According to the statistics, the output of instant noodles in Henan Province accounts for nearly 33% of the country. However, this output is distributed in the instant noodle industrial belt from Xinxiang in the north to Luohe in the south. If the scope is narrowed down to cities and counties, the most concentrated place of the instant noodle industry is actually not Henan, but a county called Longyao in Xingtai City, Hebei Province. It is the home of Jinmailang.

Longyao

As a large grain-producing county in Hebei Province, Longyao has become the world’s largest instant noodle production base driven by leading enterprises. Longyao is an agricultural county that mainly relies on wheat cultivation.

Regional location of Longyao County

However, it is in this small county the nation’s instant noodles production started. It gave birth to the richest man in China’s instant noodle industry and became the world’s largest instant noodle production base with an annual output of 14 billion packs of instant noodles. It was founded by Longyao people themselves, rooted and developed in Longyao. Now it has become a local brand of Longyao that is on an equal ar with Master Kong and Uni-President: Jinmailang.

Hurun

In the ‘2022 Hurun Top 100 Chinese Food Industry List’, Jinmailang ranked 48th (Chef Kong ranked 25th). In terms of value changes, other enterprises on the list either have negative growth or double-digit growth at most, while the year-on-year growth of Jinmailang has reached an amazing 126%, becoming the enterprise with the fastest value growth rate on the list. Jinmailang’s annual production capacity is 12 billion packs of instant noodles. It processes 5500 mt of wheat per day and 1.8 mt mt p.a., it ranks in the top six in its industry in the world and the top three in China. When we add the capacities of other related enterprises in Longyao, the regional annual production capacity of instant noodles is as high as 14 billion.

Pillar of the local economy

Jinmailang’s instant noodle production has long realised intelligent automatic production. The Longyao food industry, which is driven by instant noodles, has an annual revenue of more than RMB 17 billion and the more than 100 food manufacturing and supporting enterprises in the county contribute one-third of Longyao’s total profit, which makes it a proper pillar of the local economy. Longyao is also the world’s largest production base for paper containers and bottle caps.

Beginning

In 1992, Wei Yingzhou, a Taiwanese businessman, founded Dingyi Food in Tianjin, and Chef Kong instant noodles soon became popular in China. In this year, Fan Xianguo, a native of Longyao, took the money saved from running a small workshop and partnered with more than a dozen people to form the Tianshuai Group to produce single-crystal rock candy. Chef Kong’s popularisation made Fan Xianguo see the huge market for instant noodles, but the partners did not agree to do this. Therefore, in 1994, Fan Xianguo took a few people to establish Hualong Group. This time he got the decision-making power. An instant noodle giant who can be equal to Chef Kong in the future was born.

Rural market

At that time, Chef Kong and Uni-President were aiming at the urban market. There was no way to sell it in the countryside at all. They could only see some mixed brands, even instant noodles without packaging. From the start, Hualong targeted the blank area of the rural market. A strategy they had learned from Mao Zedong. An important contributor to the success of the Communist Party was the strategy to ‘let the countryside encircle the cities’. Its first instant noodles was called ‘Hualong Noodles’, which focussed on cheap and affordable. The advertisement of ‘Hualong noodles, you see them every day’ was painted all over the walls of rural areas. Hualong instant noodles also quickly occupied the rural market. In just three years, Hualong began to aim at the national market.

National

In 1997, Hualong established more than 600 sales networks in more than 20 provinces and began its own plan to occupy the instant noodle market north of the Yangtze River. At this time, Wang Lushan, Fan Xianguo’s hometown, was also an agent of Hualong Group in Gansu. He followed Hualong Market all the way, made a lot of money, and also had the idea of working for his own account. In 1999, Longyao’s second brand that stirred up the national instant noodle market was born. Wang Lushan, who was familiar with the old owner’s products and routines, established Zhongwang Group. With two brands of instant noodles, he quickly became a brand that was higher than Hualong in the rural market at that time. In 2000, it achieved sales of RMB 100 mln, and two years later, it became one of the top five instant noodles in China.

Jinmailang

Around 2000, the sales of Hualong instant noodles began to grow rapidly. In that year, Fan Xianguo gave up the Hualong trademark and launched a new brand ‘Jinmailang’. Jinmailang cooperated with Nissin Group (Japan), a global boss leader in instant noodles, and became the world’s largest noodle-making enterprise at that time. Subsequently, it launched the new-tech instant noodle brand Dajinye.

Wugu Daochang

On Wang Lushan’s side, he found the marketing director of Hualong before, began to cooperate with Chef Kong, and then launched a new non-fried instant noodle brand Wugu Daochang. Wugu Daochang did very well. In 2006, it also achieved annual sales of RMB 2 billion. That year, Zhongwang also topped the top 100 Chinese enterprise growth list with a growth rate of 2003%. After that, although Wang Lushan’s Zhongwang Group declined due to blind expansion, Longyao’s instant noodle industry and other related supporting industrial chains rose rapidly because of this competition between, what was locally referred to as: ’two dragons fighting’.

Decline and back

Since the 1990s, China’s instant noodle industry has been booming, and the turnover has increased for 18 consecutive years. However, since 2013, the instant noodle industry has begun to go downhill. The reason is very simple. 2012 was the first year of the rise of China’s takeaway industry. The fierce battle of Meituan, Eleme, Dianping and other platforms in this year’s ‘thousand-group war’ made instant noodles ‘out of favour’ from people’s list of instant foods. In fact, any food became instantly available. With the upgrading of the consumer market and the consideration for a healthy, nutritious and balanced diet, instant noodles were no longer a must or even an option for many people to pursue a convenient diet. It was not until the pandemic that the instant noodle industry showed signs of rebound again. According to the statistics, the market size of China’s instant noodles in 2018 was RMB 103.9 billion, and it increased to RMB 182.38 billion in 2022. It is estimated that by 2025, the market size will reach RMB 231.23 billion.

Innovation

Technological innovation is an important driver behind the continuation of the status of Longyao as China’s top instant noodles base. As early as six years ago, Jinmailang was selected as one of the top 10 innovative food companies in China in 2018 with 926 patents, together with the top international food groups of Mars, Pepsi and Starbucks. At the beginning of 2022, Jinmailang announced that it had completed a financing of RMB 600 million from investor Jiahua Capital.

China’s central and local governments have invested significantly in the development of food industry parks, designated areas that facilitate the efficient collaboration of regional food companies. These parks have received a series of supportive policies to foster their growth. In 2024, China’s food industry parks generated RMB 270.78 billion in sales revenue, representing a 13.20% increase. Notably, food industry parks actively share new technologies and equipment to enhance production, product quality, and distribution.

Overview of the Food Industry Park

Screenshot of the Laiyang Food Park from Baidu Maps

A food industrial park comprises a cluster of food industry, related supporting industries, and service institutions within a specific geographical area. It integrates the functions of food production, processing, sales, research and development, and possesses the advantages of industrial clustering efficiency, infrastructure, policy support, and other benefits. Depending on the industry type, food industrial parks can be categorised into comprehensive food industrial parks and specialised food industrial parks.

Development Stages

The beginning

The development of China’s food industry in industrial parks has progressed through four distinct stages. Initially, during the early 1980s, China’s economic system reform paved the way for agricultural industrialisation, creating the foundation for the emergence of food industrial parks. In the early stages, food industrial parks primarily focused on the processing of primary agricultural produce, including grain, oil, meat, poultry, and aquatic products. This led to the formation of regional industrial clusters based on resource advantages. At this stage, park construction was centred around the primary production area of agricultural products, characterised by low industrial concentration and small enterprise scale. While the government initiated efforts to support the development of food industrial parks through policy guidance, overall support was limited.

Reform Phase

The subsequent reform phase marked a significant transformation in China’s food industry. During this phase, the government implemented comprehensive reforms aimed at enhancing the development of food industrial parks. These reforms encompassed policy guidance, targeted support, and other measures designed to foster the growth and prosperity of these parks.

Reform Phase

The subsequent reform phase marked a significant transformation in China’s food industry. During this phase, the government implemented comprehensive reforms aimed at enhancing the development of food industrial parks. These reforms encompassed policy guidance, targeted support, and other measures designed to foster the growth and prosperity of these parks.

In the transformation stage of the 1990s, with the gradual establishment and improvement of the market economy system, food industrial parks began to standardise. The government strengthened the planning and management of industrial parks and improved their standardisation. The industrial park began to develop towards the comprehensive industrial chain. From the beginning of the 21st century to the stage of rapid development from 2015, China’s economy entered a stage of rapid growth, people’s living standards greatly improved, and the requirements for food quality and safety continuously improved. As an important platform for industrial agglomeration and upgrading, food industrial parks entered a stage of rapid development. The food industry park gradually formed a complete industrial chain from raw material cultivation, through processing to sales. At the same time, the number of high-tech food processing projects, such as biological engineering, nutrition and health food, etc., increased.

Today

In the stage of innovation and development from 2015 to now, China’s economy has entered a new normal, and food industry parks are facing the need for transformation and upgrading. Food industrial parks actively introduce new technologies and processes, such as intelligent production lines, automated warehousing systems, big data analysis platforms, etc., to improve food processing efficiency, quality control and supply chain management capabilities. At the same time, the national government promotes green transformation and intelligent upgrading, and supports food industrial parks to move towards high-quality development. In 2024, the sales revenue of China’s food industry parks was RMB 270.78 billion, an increase of 13.20% year-on-year.

The industrial chain

The upstream participants of the industrial chain of the food industrial park are food enterprises, investors, real estate developers, etc. There are various types of food enterprises, including dairy, aquatic products, meat, alcoholic beverages, leisure food, etc. The participants in the middle of the industrial chain mainly include food industrial park operation and management enterprises. The downstream of the industrial chain consists of sales channels, logistics distribution, brand promotion, product marketing, etc.

Current issues

In 2024, the industrial capacity utilisation rate of China’s food manufacturing industry was 69.8%, down 0.46 percentage points year-on-year. From the background, the global economic downturn and the tight trade environment have weakened the growth momentum of food exports. Although domestic consumer demand has gradually recovered under the policy boost, the growth is still weak. Structural contradictions within the industry are prominent, and the supply of production capacity in some areas exceeds market demand, resulting in a decline in capacity utilisation. In addition, the increase in the number of enterprises but the expansion of losses also confirms the current situation of insufficient utilisation of production capacity. The decline in capacity utilisation has squeezed the profits of enterprises, and the operating pressure of some enterprises has increased. However, this change has also forced the industry to accelerate its transformation. The policy level may continue to promote the optimisation of production capacity, support technological innovation and green development, and guide enterprises to focus on high value-added areas. For enterprises, it is necessary to strengthen market research and judgement, optimise the layout of production capacity, improve competitiveness through technological upgrading, product innovation and refined management, gradually eliminate backward production capacity, and achieve a dynamic balance of supply and demand.

Relevant policies

In October 2024, the Ministry of Industry and Information Technology issued the Notice on the Key Cultivation of Traditional Advantageous Food Production Areas and Local Characteristic Food Industries, which proposed to focus on cultivating eligible traditional food production areas and local characteristic food industries, fully exploit the regional resource endowment, clarify the development direction and cultivate excellent At the first level, guide localities to accelerate the formation of local characteristic food industry advantages according to local conditions, release the vitality of traditional industrial development, build characteristic food industry clusters, promote the construction of a strong manufacturing country and a healthy China, cultivate new driving forces for economic development, and drive farmers’ employment and income growth and regional economic development. Through policy support, resource integration, industrial cluster creation and brand promotion and other measures, food industrial parks will achieve high-quality development, improve industrial competitiveness, promote farmers’ income increase and regional economic development, and help rural revitalisation and common prosperity.

Example

Shandong Laiyang Food Industrial Park was established in 2001 and is an important food industry agglomeration area in Shandong Province. The total area of the park is about 5.27 square kms, which is divided into two parts: Food Industrial Park (4.74 square kms) and Longda Industrial Park (0.53 square kms). After more than 20 years of development, it has formed a modern food industry cluster mainly focussing on beverages, juices, dairy, biscuits, canned food, and food additives. There are 68 processing enterprises in the park, including 2 leading national food enterprises (Longda Group and Chunxue Food, both meat processors) and 1 leading provincial enterprise (Longda Meat), which has cultivated 2 backbone enterprises, 8 potential enterprises and 7 growth enterprises. All these terms are officially recognised categories. The category of your organisation determines from which policies you may benefit.

The hamburger, a fast food originating in Europe and the United States, has gained global popularity. Typically composed of a halved bun, meat, vegetables, sauces, and other ingredients, it has become a cornerstone of Western fast food.

The hamburger industry in China emerged from Western fast food, initially introduced by brands like KFC and McDonald’s. In recent years, driven by the accelerated pace of life and the growing demand for fast food, Western fast food has experienced rapid development in China. Hamburgers serve as the defining component of Western fast food, attracting consumers through their status as a ‘signature product’.

Chinese hamburgers have demonstrated strong market appeal and substantial development potential, solidifying their position as one of the most dynamic categories within the Western fast food industry in China. Brands like Tastien, at the forefront of this development, promote a fusion of Western and Chinese flavours, effectively capturing the ‘Chinese stomach’ through the combination of Chinese flavour and Western standards.

Statistics indicate that in 2024, China’s Western fast food market generated approximately RMB 298.3 billion, with the hamburger market comprising approximately RMB 32 billion. It is projected that in 2025, the Western fast food market will expand to RMB 330 billion, while the hamburger market will reach RMB 44.5 billion. This growth trajectory is anticipated to persist in the subsequent years.

Classification of the Hamburger Industry

Chinese marketeers categorise hamburgers on the type of meat patty:

The hamburger industry in China comprises several stages: upstream, middle, and downstream. The upstream sector primarily involves beef, chicken, fish, vegetable meat, and other meats, along with wheat flour, yeast, sugar, oil, lettuce, tomatoes, onions, sauce, cheese, food additives, and other raw materials. Additionally, cold chain transportation and other industries are included. The middle section comprises hamburger brand operators. The downstream sector comprises offline stores and online platforms.

Typically, beef is used in hamburgers, but many Chinese consumers prefer chicken. Furthermore, with the improvement of Chinese consumers’ living standards and the acceleration of their development, they have increasingly prioritised the quality of their diet. Consequently, chicken is perceived as healthier than beef. Chicken production has maintained a steady growth trajectory. In 2024, Chinese chicken production amounted to approximately 15 million metric tons.

The Chinese hamburger industry caters to a diverse consumer base, encompassing individuals of various ages and socioeconomic backgrounds. Notably, young people, particularly teenagers, constitute a significant consumer segment. In 2024, the total population of China was 140.28 million, comprising 943.5 million urban dwellers and 464.78 million rural citizens.

The competitive landscape in the Chinese hamburger market is characterised by several major enterprises. Notably, international fast food chains such as McDonald’s, KFC, and Burger King dominate the market. These leading international fast food brands have set the objective of accelerating the expansion of their stores and cultivating the Chinese market.

In response to the accelerated expansion of Western fast food, the development pace of local Western fast food brands in China has not been hindered. These brands continue to establish themselves in first- and second-tier cities, further intensifying their market presence. Currently, the prominent brands of Chinese hamburgers include Wallace, Tastien, Happy Star Hamburger, Pale Hamburger, Midberg Halal Burger, Malezi Burger, Manlido Fried Chicken Burger, and others.

Various Chinese burgers offered by Tastien; including beancurd burgers, chilli chicken burgers, etc.

Traditional ingredients adapted for hamburgers

An interesting spin-off of the development of Chinese-style hamburgers is that some manufacturer of traditional ingredients have note this a new business opportunity. China’s leading producer of fermented beancurd (furu), Wangzhihe, has developed a version of this condiment for the use on hamburgers. Indeed, shouldn’t Chinese hamburgers be seasoned with Chinese flavours? Follow the link in this paragraph to read more about furu.

Slow Boat: beer + hamburgers

Slow Boat Brewery, a Beijing-based craft brewery, was founded in 2011 by Chandler Jurinka and Daniel Hebert. It started as a small pilot brewery in the mountains outside Beijing and has grown to become one of China’s largest craft brewers by production capacity. The brewery is known for its small-batch, creative beers and its dedication to promoting the Chinese craft beer movement. Its outlets also serve a broad range of hamburgers. Both the beer and the accompanying food tries to gear to the Chinese palate while also retaining a sufficient degree of foreignness.

Hunan cuisine, known in China as Xiang Cuisine, Xiang being the literary name of Hunan Province, is one of China’s more famous cuisines. It is characterised by its liberal use of chili peppers and garlic, but also by its use of very fresh ingredients. A typical way of preparing and serving dishes in Hunan is the ‘dry pan’ (ganguo). Those dishes are served in an iron pan on a fire to keep it hot.

Hunan’s capital Changsha is foodies’ paradise. As a patron of this blog, you know that food is the central concept of Chinese culture. Food is available in abundance everywhere. However, there are still cities in China that even Chinese refer to as places to go for food lovers, and Changsha is one of them.

Changsha is also very centrally located in the heart of China. In Europe, all roads may lead to Rome, but in China they lead to Changsha. Changsha is a major infrastructure hub. This highly facilitates the export of the local cuisine to all corners of the nation, and beyond its borders. However, in this post, I will restrict my story to the situation of Hunan cuisine within China in 2024.

Regions

In an earlier post, I introduced the major food regions of China. The following table shows the percentage of Hunan restaurants in China in each region.

These figures confirm that fire food is still more appreciated in Southern China than in the north.

Cities

At a lower level, Chinese cities are catogorise by function and size. First tier cities are the cities directly under the State Council (Beijing, Tianjin, Shanghai and Chongqing). New first tier cities are the capitals of provinces and autonomous regions. The remaining cities are categorised by size. The following table shows the percentage of Hunan restaurants per urban category.

We can see that Hunan cuisine is most popular in regional capitals and smaller regional cities. A possible explanation could be that cities in the south of China tend to be smaller, with the largest cities concentrated in the north. E.g., of the four first tier cities, only Chongqing people prefer spicy food.

Province/autonomous region

I am also adding a map indicating the number of Hunan restaurants per province and autonomous region. Dark red indicates a higher number.

The top regions, Hunan (obviously) and Guangdong are indicate with percentages, 19.6% and 17.8%, respectively. Guangdong is a special region, adjacent to Hong Kong, where many emigrés from other parts of China are living. I presume that Guangdong is the home of quite a few people from Hunan.

I could go even deeper, including, e.g., the regional distribution of the various Hunan restaurant chains. However, that information would be unsuitable for a post like this. However, I will be able to provide an in-depth study upon request.

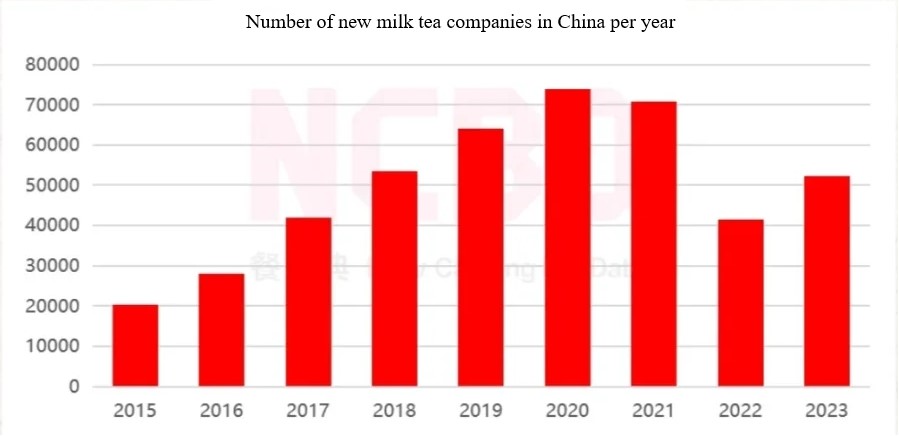

A rapidly growing beverage category in China are the milk teas. They are a combination of the bubble teas that originated in Vietnam and based and traditional milk or butter teas drunk by Mongolians and Tibetans.

In the course of 2018, China’s tea aficionados have embraced a new trend, one that is encapsulated in the growing popularity of the milk tea brand, Heytea. Originally sold in a tiny alleyway in Jiangmen, southern China’s Guangdong province, the brand went viral on social media because of its signature “cream cheese” series — a cup of hot sweet tea topped with a spoonful of savoury cream cheese. Since then, Heytea has developed into a franchise with more than 80 outlets in 13 cities across the country. There are also outlets in North America.

Milk tea now has many brands and more are still being added. Some are already established brands: for example, Naixue, Chagee, Mixue Ice Cream & Tea and Chabaidao.

This table shows the number of new outlets opened per year.

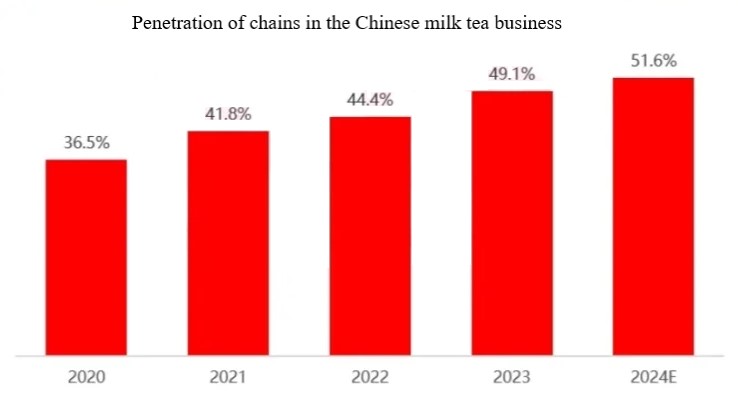

The penetration of chains has been steadily increasing in this business.

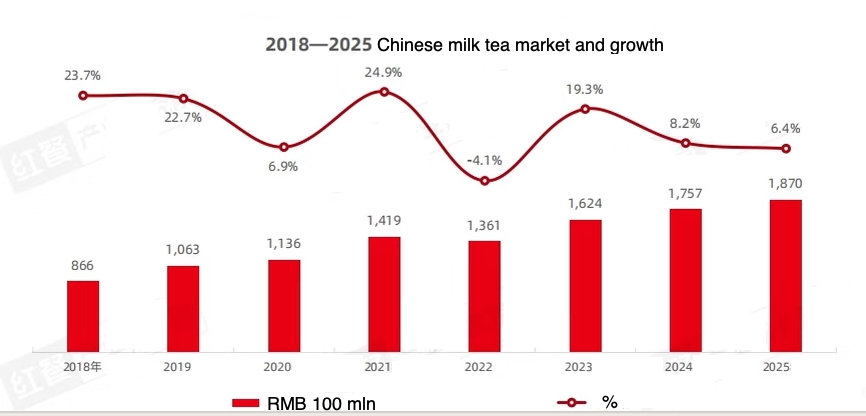

Here is an overview of the market size in RMB 100 mln and annual growth in %.

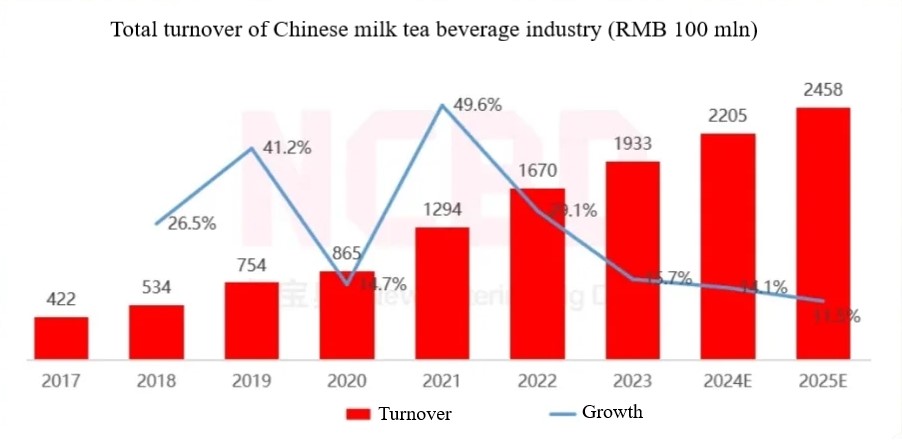

The following table lists the turnover and profit for a number of major players in this market for 2024.

This positive trend can be expected to continue, as the total turnover of this business is expected to grow, at least during the coming few years.

The 2023 New Tea Drink Research Report, released by the China Chain Store and Franchise Association and Meituan New Catering Research Institute, predicts that by the end of 2025, the market size of Chinese-style tea drinks will reach RMB 242.5 billion.

The Chinese bakery business is booming, but the market is also extremely volatile. There is no better moment to enter the Chinese market for suppliers of any bakery ingredient than now.

I have collated a few statistics that are recent enough to give a rough impression of the size of the market.

The first table indicates the development of the value of the market and the projection of the near future.

Some interesting details about consumer behaviour:

Whether online or offline, women are still the main consumers of baked goods in China.

In terms of age, 70% of consumers are between the ages of 21 and 40.

In terms of price, consumers spending RMB 20 – 40 in a single consumption constitute the largest segment (35. 8%).

The next table shows the number of bakery shops in a selected group of major cities. This tells something about the geographic distribution. However, the smaller provincial cities currently show the highest growth.

We should not forget the focus issue of this blog: food ingredients. This graph shows the major cream suppliers to the Chinese baking industry. As you can see, the market still consists of a few major brands and a large number of small suppliers.

This healthy food brand was founded 8 years ago, but in 2023 it already had an annual income of more than RMB 1 billion. This story, from entrepreneurship clubs for students to food companies with an annual turnover of more than RMB 1 billion, started with the wrong choice of study by the founder.

Zheng Guo, founder of Unicorn

Wrong study

At the time, Zheng Guoyu chose to study computer science. ICT was then a popular field and Zheng Guoyu made his choice without in-depth knowledge of the technology. Soon after enrolling, he discovered that he wasn’t interested in it, so he joined a club that played entrepreneurship games. Unicorn (Dujiaoshou 独角兽) was one of his entrepreneurial projects in that club.

Candy

In 2015, Zheng Guoyu’s first venture was based on the touristic popularity of his hometown, Xiamen, the major port city of Fujian. He created a special e-commerce platform to sell handmade sweets and souvenirs. According to Zheng Guoyu, a turnover of almost RMB 10 million was already achieved at that time. But he didn’t have a positive cash flow and wasn’t making a profit. However, he did gain a lot of experience at that time.

Light food

From the beginning, the Unicorn brand has been positioned in the market for what is known in China as Light Food (qingshi), which is a low-calorie, low-salt, sugar-and-fat food. The first product has achieved a turnover of more than RMB 60 million in 3 years. In 2022, the revenue was more than RMB 700 million, and the revenue for 2023 is estimated at RMB 1 billion. This growth will continue. According to Zheng, what is the driving force behind this rapid success?

Beauty parlour

Zheng sees the university as a ‘beauty salon’. Young people on the university campus are starting to pay attention to their bodies and clothes, and when Zheng Guoyu himself started at the university, he and his classmates also had a need for fitness and weight control. When they got their university gym card and tried to follow the coach’s instructions to start eating healthier, they discovered that there were few products to choose from on campus.

Internet

Preparing low-fat meals yourself was not realistic, as the use of electrical appliances such as refrigerators and hotplates was prohibited in university dormitories. Zheng Guoyu and his classmates therefore chose to buy light meals over the internet. They found that the unit price of chicken breast there was between RMB 150 – 200; A very student-unfriendly price. This unmet need presented a commercial opportunity.

Small portions

Starting from their own needs, Zheng Guoyu and his classmates began to think about what light meals they would like to buy: small portions that are individually wrapped, not too expensive in price, lean but still tasty. Zheng Guoyu, who was already in the entrepreneurs’ club, started this entrepreneurial project with his team.

Outsourcing

The team has gained entrepreneurial experience by negotiating production outsourcing with factories. When they discovered that there were very few ready-to-eat chicken breast products in small packages on the market, Unicorn decided to find a factory to produce chicken breasts in small packages based on their specifications.

Unicorn’s lean chicken breast with crayfish flavour (you can compare it with the chicken breast of Dacheng on the Trends page of this blog)

Resounding success

The first product was an instant hit. In 2017, the ready-to-eat chicken breast was launched, and already in 2018 achieved a turnover of more than RMB 20 million in 2018 and RMB 60 million in 2019. It became the best-selling brand in its category on the Taobao internet store.

In-house production

When, three years after its founding, the scale of RMB 100 million was reached, Zheng and his partners thought it better to build their own factory than to continue to rely on outsourcing to multiple third-party factories. They thought it would be better not to look for external financing right away, but to finance the factory from their own income. Nor did they immediately aspire to become the market leader. Staying profitable was more important. This also applied to the promotion costs. Unicorn is active on several internet platforms, but does not invest in excessive promotional campaigns and steadily tries to build brand awareness through consistent quality.

Traditional brand

Unicorn, which was born on the internet, has been around for 8 years now, but hopes to transform itself into a ‘traditional brand’ that makes good use of the internet. According to Zheng Guoyu, China’s e-commerce platforms are about 20 years old. However, there are popular consumer brands that are 30 or 40 years old and still viable. If Unicorn would like to live to be 50 or 100 years old, the brand must also learn from the traditional brands. That means you should also be found in physical stores.

New channels

Zheng sees great opportunities for offline sales. That does require changes in the supply chain. Online sales are made in small quantities. Large batches are needed to supply stores. Also, the pricing of products has to change in order for retailers and the like to earn money from sales. According to Zheng, it may be necessary to develop new products for offline sales. “We found that in order to solve this problem, we may need to develop other products, and the net content, specifications, and taste of the products need to be adjusted,” Zheng said.

Export

The next step could be export. At the end of 2020, Unicorn set up an export company. However, it is more difficult to export food because the regulations are different in each market. The strategy chosen by Zheng is to first gain experience with the export of textile products (bedding), for which the rules are less strict, and then to move on to foodstuffs.

Comments

This entrepreneurial story also offers insight into the typical way of thinking of Chinese entrepreneurs. Whereas Western biographies of entrepreneurs usually portray the protagonist as the ‘born entrepreneur’ who knows how to realize an idea with unique strategic insight, Zheng is someone who is proud of the fact that his idea is due to a wrong choice of study and has come to fruition in a social context (the entrepreneurs’ club on campus). Where the typical Western start-up entrepreneur is willing to sacrifice everything to make a company grow quickly (quick success or failure), Zheng thinks in terms of continuous learning by keeping the company up and running for as long as possible and converting what he has learned into long-term strategy. Reverence for one’s ancestors is an old Confucian value.

Stating that China is a huge nation with a very diverse population is kicking in an open door. However, a major shift is taking place in the demography of China that is exercising significant influence on a number of markets, including food and beverage. I like to refer to it as the shift from ‘big collectivism’ to ‘specialised collectivism’. In fact, Chinese collectivism has always been smaller than in, e.g., Japan. Where Japanese copy each other’s behaviour on a massive scale, not rarely on the national level, Chinese focus on smaller groups, like: family members, people from the same neighbourhood, colleagues in the same department of their work unit, etc. Still, due to the huge Chinese population, even a small group is still enormous and therefore interesting to anyone who is (re)designing foods for the Chinese market. This post is taking a closer look at some of the more important demographic segments.

Would it be worth your effort to develop food for golfers?(read the post and find out more at the end)

Elderly

I have reported about food for the elderly in an earlier post. Here, I will provide more background information. Population is the foundation and main body of economic growth and social development, and age structure is a core determinant of population quality and population structure. It is of great significance to study the age structure of the population, especially the aging problem. China’s population aged 60 and over is about 260 million, accounting for 18.7% of the total population. Due of the importance of this consumer group, not only because of its size but also because the elderly are still held in high regard in China, the Chinese government has issued a large body of legislation for ensuring that the elderly are taken care of.

Aging society

China has entered an aging society in 2000. The average age of the population has caught up with the United States and Japan. Due to the decline in fertility rate and the increase in life expectancy, aging is an important problem faced by all countries in the world, but due to the long-term implementation of family planning policy, this problem is more urgent in China. According to the internationally accepted classification standards, when the proportion of the elderly population aged 65 and over in a country (region) exceeds 7% of the total population, or the proportion of the elderly population aged 60 and over exceeds 10% of the total population, that country (region) is regarded as having an aging society. According to the statistics of the United Nations Population Program, in 2000, the proportion of China’s population aged 60 and over exceeded 10% for the first time to reach 10.03%, and in 2002, the proportion of China’s population aged 65 and over exceeded 7% for the first time to reach 7.08%, marking that China has officially entered an aging society in 2000. In 2019, China’s population aged 65 and over reached 176 million, nearly double the 88 million in 2000, accounting for 12.6% of the total population. In 2019, the average age of China’s population reached 37.6 years old, compared with 38.9 years old, 46.7 years old, 41.7 years old and 30.0 years old in the United States, Japan, Europe and India in the same period. It is estimated that in 2030/2050, China’s population aged 60 and above will account for 24.8% – 34.6%, 65 years and above will account for 16.9% – 26.1%, and the average age of the population will reach 41.2 – 45.6 years.

Life expectancy is rising, birth rates are low, and the Chinese population is aging at an unprecedented rate. With the improvement of living standards and medical conditions, the life expectancy of the Chinese population has increased significantly, from 44 years in 1960 to 77 years in 2019, and the life expectancy of the population in some developed coastal areas is higher. The life expectancy of Shanghai’s population in 2019 was as high as 83.66 years. The Chinese birth rate in 2019 was only 10.48 per thousand, and the number of newborns was only 14.65 million, down 580,000 from 2018 and a new low in 70 years.

The policy of encouraging childbirth after the founding of the People’s Republic of China in 1949, generated the first baby boom in New China. The birth rate remained above 37% for five consecutive years. The improvement of the economy after the end of the natural disasters in 1959 – 1961 led to compensatory births, triggering the second baby boom, with more than 250 million births within 10 years, accounting for 17.6% of the total number of Chinese population at present. These two waves of baby boomers will gradually enter old age between 2010 and 2030. The rate of aging in China from 2010 to 2030 is expected to be similar to that of the most rapidly aging period in Japanese society (1990-2010). The insufficient number of newborns will accelerate the aging rate of the Chinese population.

If this rate develops, the average age of the Chinese population will reach 45.6 years old in 2050, the proportion of the population aged 14 and under will only be 14.15%, and the proportion of the population aged 65 and over will reach 26.07%, when there will be one elderly person aged 65 and above in every four Chinese.

China’s “silver economy” has broad prospects

The elderly care industry is a comprehensive industrial cluster to meet the health and happiness requirements of the elderly population. On the whole, the elderly care industry covers food, housing, care, medical treatment, finance, culture, entertainment, science and technology and other aspects, and is an industrial system that meets the multi-level needs of the elderly, from the basic living needs (housing, food, medicine, clothing) to the psychological and spiritual needs provided by (fun in life). The three pillars of China’s pension system are basic pension insurance, annuity and personal pension, of which the first pillar accounts for 85%, much higher than the 11% in the United States. According to international experience, the pension replacement rate is greater than 70% to maintain the standard of living before retirement, if it is less than 50%, the living standard will drop significantly compared with before retirement.

Chinese traditional culture is deeply influenced by Confucianism. Home care is more in line with secular concepts than welfare facilities for the elderly, so home care and community care will continue to be the mainstream of China’s pension model. Facility care will be there as well, but as an auxiliary model. From 2010 to 2018, the number of people aged 65 and over in China increased by 47.64 million, while the number of elderly care institutions increased by only 128,000 and the number of elderly care beds increased by only 4.122 million, with an average of 1,393 elderly people having an elderly care institution, the supply is far less than the market demand, and home care is more in line with China’s traditional culture.

Government support

The central authorities heavily support keeping this large segment of the population healthy. Through its Office of the National Working Committee on Aging, the government has issued a plan to organize the elderly nutrition improvement action in the country from 2022 to 2025.

The notice proposes four actions, including publicizing the nutrition and health knowledge of the elderly, strengthening nutrition intervention for the elderly, improving the ability of elderly nutrition and health services, and carrying out public welfare activities for elderly nutrition and health. Apart from the general Dietary Guidelines for Chinese Citizens, that saw an updated version this year (from the previous 2016 version), the government also issued a separate Dietary Guidelines for the Elderly and one for the very old (<80 years).

The government also organizes several campaigns for promoting healthy living and eating, like: the National Elderly Health Promotion Week, or Respect for the Elderly Month. The phrasing of the latter refers to an important trait of the Chinese policy towards promoting the health of the elderly: the duty of the young, in particular children, to see to it that their parents lead a healthy and happy life. The government rolls out the playing field, but the policies are executed by the children, where necessary assisted by government officials of various administrative levels.

The lowest administrative levels have a special role in the implementation of the national policies. Senior citizens move less easily than younger generations, so it is imperative that their care is in the hands of grass root level administrations, like communities (shequ 社区) or neighborhood commissions (jiedao 街道). These administrations include Elderly Affairs Offices (laonianban 老年办) to see that the elderly under their jurisdiction are take care of well, including their nutritional needs.

Children and local government officials go about carefully, when trying to improve the eating and drinking habits of the elderly in their care. A report published by the site Herbridge gives some interesting examples from interviews with various consumers.

The elderly may have fixed habits that are not easy to change. E.g., many stick to old habits and buy what they have bought for decades, without giving a thought to whether their bodies are still capable of digesting high sugar high fat foods.

That situation is turned around by another group of elderly. A woman who buys the groceries for her mother complains that her mother now prefers fruits and vegetables, but that she worries that this will lead to malnutrition, while her mother is already very thin. Meat and fish are still regarded as the most nutritious foods by many Chinese. While the young now like to have slim bodies (see further on in this report), most middled aged Chinese still regard a slightly protruding tummy as a sign of good health.

Then there are also people with some basic knowledge about food ingredients who try apply that insight to adjust their parents’ diet. One interviewee has bought a jar of xylitol powder to substitute the sugar jar in the family kitchen. She now sweetens foods and drinks for her mother with xylitol wherever possible.

A final example of inventive adjustment of a parent’s nutrition is a man whose father stopped liking oatmeal porridge made with milk, although he bought an expensive type of ‘smooth milk’ for his father. He then replaced the milk with unsweetened yoghurt which his father liked very much. The report does not mention if this was a case of lactose intolerance. It is still a great example of how deep present day Chinese are involved with nutrition.

The Young (?)

The ‘young’ is insufficient for denoting an age group in present day China. China has developed so rapidly during the past decades, that Chinese marketers like to divide the country’s population in cohorts named after a decade – such as the post-80, the post-90 and the post-00. Each group is characterized by a number of distinctive habits and world outlook. The post-80s were born after the end of the Cultural Revolution and have been shaped by the early years of the economic reforms that changed the lives of Chinese so profoundly. They are approaching 40 now and most of them are married and have children. They are much more affluent than their parents but are not big spenders on food, as there are so many other expenditures to worry about. A considerable part of those expenditures are for their children, the post-00s, including candy and snacks.

Single dogs

This is another category that has been introduced in an earlier post. The post-90s are young, well-educated, concentrating on their careers in corporations or their own start-up enterprises. With a few exceptions, they are all only children and have been spoiled by their parents and grandparents, as a result of which they have developed a taste for good food. Moreover, a considerable part of them are single and living by themselves. They may marry once, but they give priority to their careers. Many pursue that career outside their hometown, so also away from their school and neighbourhood friends. A modern term for these people is Single Dogs (danshengou 单身狗). Experts estimate the current number of people in the post-90 cohort at 188 million, approximately 14.1% of the Chinese population. 92 million of them were living a single life in 2021. In spite of their young age, many of the post-90s are complaining about ailments resulting from their demanding lifestyle. A 28-year old female Internet programmer is quoted as saying: “I used to buy supplements for my parents, now half of the supplements I buy are for my own consumption.”

So, what and how do the post-90s eat, besides taking supplements? Based on my own observations, they easily spend RMB 100 per person per day on food. They typically live in two-bedroom rental apartments. They have the equipment to cook but many lack the skills. They are the generation of ‘little emperors’, spoiled by their parents, who provided three meals a day, so their child could concentrate on their education. As long as they came home with top grades, the sky was the limit in regards to what their parents would do for them.

The post-90s also lack time. They are enjoying the freedom of their own apartment but are still leaving home early and returning late. They do eat fast food occasionally but they have learned to appreciate good food and they are also still Chinese, so their palates are longing for the right textures and flavours. They are conscious about good nutrition as introduced in the previous report.

The Chinese food industry is allocating considerable R&D funding to serve this cohort, which has resulted in an impressive range of ready-to-eat or semi-finished products. This is a brand-new food category in China, so there is no ready-to-use categorization of products. To cash in on this trend, food producers and retailers have started making and selling single-portion packed versions of a large spectrum of foods and drinks.

Punk diet

One of the ‘bad’ habits many of them share is staying up late, or even regularly skipping sleep altogether. A survey has shown that 44% of the 19 – 25 years cohort stay up until after midnight. In order to stay awake, they need aoyeshui (熬夜水) night owl beverages (literary: staying up all night water)’. Most of these are based on the milk tea drinks that have become so popular among young Chinese. Some also contain traditional Chinese medicinal herbs, which links these drinks to the nationalist trend (guochao 国潮).

This does not mean that the post-90s neglect their health. On the contrary, a healthy body is as important to them as I indicated in the first report. They smoke considerably less than their parents, for example. However, they want to combine healthy living with happy go living lifestyle. A term that has become fashionable among the same post-90 consumer segment is pengke yangsheng (朋克养生), or the ‘punk diet’: nutritious food presented as junk food. The choice of this term indicates that these consumers give themselves a kind of subcultural status. A concrete product type will help clarify this term and a good example food in this context is the energy bar. Energy bars are the ideal ‘punk diet’ food. They can be consumed with one hand, while the other remains functional (e.g., for moving a computer mouse). They provide energy, but are also a source of fibre and nutrients, so comforting to both your stomach and your consciousness. The Chinese name for this product, yingyangbang (营养棒), literally means: ‘nutrition stick’. You can find some examples on the Trends page of this blog. Nuts, a natural source of nutrients, form a common ingredient, but you can add whatever you want, or, better, is allowed by the local regulations. Another occasion for consuming energy bars in China is what I would like to translate as ‘après fitness’ (jianshenhou 健身后) as a parallel to après ski. The Chinese are only just starting to ski, but fitness centres are extremely popular in this age group. One recent study states that there are more than 43 million patrons of fitness centres in Chinese cities. After a tough spell on a treadmill, you need something that gives you energy without making you regain the weight that you just lost. The same study mentions energy bars as the favourite après fitness snack.

Bread as breakfast or snack

As introduced above, a long breakfast does not suit the lifestyle of the Chinese post-90s. Western style baked bread, that is easier to keep that the traditional steamed bread is more and more accepted as the ideal breakfast item. Moreover, it also makes an easy to consume between meals snack. You can take it to office and eat it again with one hand. To cater to post-90s demand for convenience, several Chinese bread suppliers have designed products consisting of two slices of bread with a filling in between. You just buy it, tear open the pack and eat it.

Liquid meals

When the pace of life is seen as becoming so hectic that you even lack time to chew, but you still want a nourishing meal, post-90s Chinese may look for something liquid. You can gulp it down, while still believing that you have ingested a little more than just calories. A traditional product ticking these boxes is congee. Instant congee has been on the market in China for several years. However, more nutritious products have appeared recently.

Children

This section concentrates on foods designed for the post-00 group, though not including babies or infants. One Chinese supplier defines the age group for its ‘children snacks’ (ertong lingshi 儿童零食) as 3 to 12 years. However delimited, this is still a huge consumer segment. The number was estimated at 159 million in 2020.

A salient feature of this segment is that these consumers usually do not buy the products themselves, but their parents, grandparents or other family members. However, they do regularly influence the selection of snack food purchased for them. Advertising therefore needs to appeal to both children and adult relatives. E.g., children like brightly colored packaging and advertisements related to their favourite cartoon figures. The adults will first look at the ingredients to see how ‘healthy’ the product is. Moreover, parents frequently exchange ideas about this on social media like Xiaohongshu or Weibo.

More light eating

Talking about health, Chinese parents are basically applying the same criteria to snack food for their children as they use for the foods they buy for themselves. In that respect, the contents of the first report apply to this category as well. Low fat, low sugar and low salt are mentioned frequently by people who discuss candy and other snacks for children.

A number of ingredients are perceived as especially important for the physical and mental health of children. We can take the popular category of soft candies (yingyang ruantang 营养软糖) as an example. Soft candies are used most often in professional literature on fortified children snack food.

White gold

Dairy, often referred to in China as the white gold, continues to have a high healthy profile among Chinese consumers and this is even stronger in the context of children. Foods made from milk, containing milk or adding an ingredient derived from milk are automatically regarded as more healthy. However, making a child drink a glass of milk is not easy and dairy based snacks offer a welcome alternative. One that became popular in 2023 is the cheese popsicle.

Women

As any society, the different likings of food between men and women have been a topic of discussion for ages. Also, some foods have been prepared specially for women for centuries. Bird’s nests are a good example. They are believed to be good for one’s complexion.

However, more recently foods have been launched in China that are positioned as typically for female consumers. Female consumers have become so valuable, that Chinese marketers are starting to talk about ‘her economy’ (ta jingji 她经济) as a separate market segment. The value of the Chinese health food market for women for 2025 is estimated to RMB 300 billion; from 237.9 billion in 2019.

In the realm of snacks, fruit jellies are a product almost entirely consumed by women in China. Recently, some manufacturers have developed more exciting and healthy versions. There are now jellies with fruit chunks to increase the fruit contents up to 25%, or jellies flavoured with flowers or traditional Chinese medicinal (TCM) herbs. Just to mention a few the most frequently used: Red dates or goji berries nourish qi and blood, moisturize and the complexion. Mung beans and white fungus detoxify the intestines and have an anti-aging effect. Black sesame seeds keep your hair black. This fits in with the general health trends introduced in the first report.

Female ingredients

Some ingredients are typically used in foods for women. An example of such an ingredient is peach gum. Peach gum is regarded as a beauty tonic in traditional Chinese medicine (TCM). It comes in the form of amber-hued crystals and is the resin of the Chinese peach tree (prunus persica). It is known for its beneficial properties on improving various skin conditions. Commonly prepared into soup-like desserts, often adding goji or dates. It is generally tasteless with a gelatine bouncy texture similar to bird’s nest. Peach gum is popular among Chinese women as it is rich in collagen.

Cosmetic food

The latest development in this trend is ‘cosmetic food’. So far, most of these are beverages fortified with collagen, like collagen yoghurt by Sanyuan.

More segments

When you put yourself to it, it will be possible to discern a few more special consumer segments. An obvious one is the ethnic segmentation. I intend to add a section about that to this post in the near future. However, Chinese marketers seem to develop a liking to this. The segments highlighted in this post are those worth considering when designing new or adapting existing foods for the Chinese market.

However, it is possible to pick out a more specific demographic group that you deem large and/or affluent enough an develop a product specially for that group. Eurasia Consult can assist you with this. We understand Chinese culture and how it affects food and drinks and we have a large database of foods available on the Chinese market.

*As for the question about Chinese golfers: unofficial reports mention more than 4 mln Chinese who play golf occasionally and about 1 mln regulars. The 2022 Chinese golf market (including everything, from golf club membership to equipment) was worth RMB 493 mln; up 4.8%.

Chinese New Year is on February 10 this year and regular readers of this blog know that Chinese are now preoccupied with buying stuff for the Spring Festival, the official name for Chinese New Year, and most of it will be food and drinks.

I happen to be in China at the moment to celebrate with family and friends, but obviously also to observe the latest trends. I visited Beijing’s annual New Year Fair in the Agricultural Exhibition Centre. In this post, I want to focus on the foreign influences in this year’s fair.

Russia

Russian products are by far the most important foreign foods offered on the fair. Some of them are imported, while others are produced in China, in particular in Harbin. Harbin is the home of the famous lieba, a word derived from the Russian word for bread ‘hljeb’. A big stand from Harbin also offers various Russian style sausages.

In the middle of the fair is a large space set up as a supermarket, with an entrance and an exit with the cashier. It offers a broad range of goods, including some non-food products. I am simply providing a few pictures of milk powder, chocolate, cookies, and pasta.

Australia

Australia is the second nation in terms of volume. I saw three or four stands with Australian food, in particular oatmeal.

New Zealand

There was one stand with products from New Zealand, with wine as the most visible. That was especially interesting considering that no stand offering Australian products was selling wine. A few wines were offered for exceptional low prices (for Chinese standards).

Spain

A stand promoting Spanish ham is positioned near the entrance. Interestingly the same stand is advertising with ‘pizzas with Spanish ham’.

Romania

The Romanian stand was exclusively selling wines from Romania and Moldova. The Romanian importer and his Chinese aide were selling actively, offering free tasting of several wines. On the other hand, the importer was not prepared to give special prices for the New Year, except for a 6-bottle box of the cheaper red wine.

Indonesia

Indonesia was present exclusively with coffee, including the prestigious kopi luwak.

Contact me for tailor made market research on the spot

The oldest Chinese carbonated beverages dates from 1874

Soft drinks is undoubtedly a Western concept. However, the history of domestic carbonated beverage in China is longer than many people may believe. The most famous soda beverages launched before 1949 are:

Most of the HQ locations were cities with considerable numbers of foreign expats.

The Chinese typology of foods and beverages is one of the recurrent themes in this blog. The typical way in which such products are divided in categories in a certain region provides an interesting look on the influence of the local culture on eating and drinking.

This post will continue with this topic with the typology of beverages. This typology has even been officially laid down in a State Standard (GB), GB10789 to be precise. It discerns the following types.

Carbonated drinks

These are relatively new in China and still strongly connected to the Western lifestyle. China’s oldest carbonated drink: Beibingyang (Northern Ice Sea) has been revived recently, which I have introduced in a separate post on the reappearance of old brands.

Protein beverages

Although not a Chinese invention, this category is much more popular in China than elsewhere in the world. They have also been introduced separately in a previous post. Protein beverages are relatively viscous liquids made from various nuts or beans, or milk, or a combination. A number of them include probiotic cultures.

Bottled water

Paying a lot of money for something that you can get from your tap for a much lower price has also taken on in China. China’s bottled water market is expected to reach 490 mln hls of total annual consumption by 2020. The retail value of bottled water in China for 2019 is estimated at RMB 346.2 billion. Apart from the large number of branded water, new mineral water brands keep appearing in China. Many are profiling themselves with the location of their source. The trend of 2015, e.g., in this category was mineral water from Tibet.

Some statistics of the past 5 years

Year

Volume(hls)

Increase(%)

2015

841,016,000

7.60

2014

781,614,000

9.37

2013

665,114,000

13.01

2012

556,278,000

19.20

2011

178,900,000

23.67

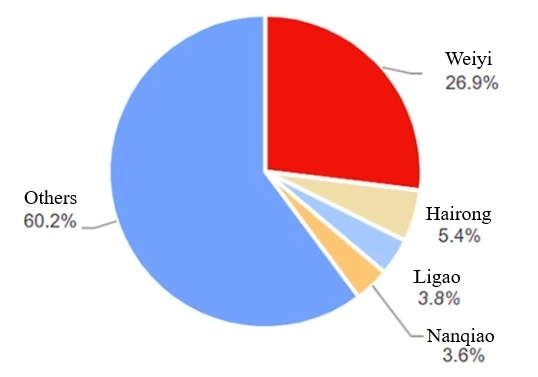

Top brands

The following table shows the market shares of major brands in 2017

Brand

Share (%)

Nongfu Spring

8.5

C’est Bon

8.0

Evian

5.0

Chef Kong

4.8

Ganten

4.6

Wahaha

4.5

Coca Cola

4.0

Others

60.7

A new variety was added to the category of bottled water by Nongfu Spring in February 2022: bottled boild water (baikaishui). This type is inspired by traditional Chinese medicine. TCM attributes many healing and nutritional functions to water that has been brought to the boil and then cooled to drinking temperature.

China’s once largest mineral water brand, Laoshan, came back in 2025 with a mineral water enriched with snake grass. Snake Grass, also known as Clinacanthus nutans, is a plant ascribed various medicinal benefits, like anti-inflammatory, anti-diabetic, anti-cancer, and antioxidant properties.

Tea beverages

Tea is China’s national drink, but still, tea beverages have been introduced from overseas. When foreign ice teas were launched in China, many beverage makers tried to concoct their own versions. Tea beverages with various fruit flavours appeared one after another.

Milk tea

A rapidly growing subcategory are the milk teas, based on traditional milk or butter teas drunk by Mongolians and Tibetans.

The pictures shows the Sizhou brand milk tea, with the following ingredients:

In the course of 2018, China’s tea aficionados have embraced a new trend, one that is encapsulated in the growing popularity of the milk tea brand, Hey Tea. Originally sold in a tiny alleyway in Jiangmen, southern China’s Guangdong province, the brand went viral on social media because of its signature “cheese” series — a cup of hot tea topped with light cheesecake mix. Since then, Hey Tea has developed into a franchise with more than 80 outlets in 13 cities across the country. In large urban centres such as Shanghai and Beijing, customers routinely wait for hours to get their hands on a cup of cheese tea. Hey Tea’s cheese-inspired beverages are just variations of the same milk-topped teas available at many urban teashops in China. Fresh milk, skimmed milk, and cream cheese are blended and poured on top of iced tea to create a layer of creamy froth about 3cm thick.

Milk tea is becoming such a huge market that ingredients suppliers have started to prioritise it in their R&D. FrieslandCampina Kievit, e.g., is conducting research to develop the optimum dairy ingredients for Chinese milk tea. Aspects considered include: tea type, milkiness, sweetness and mouthfeel.

A new development in the Chinese tea beverage market is mixed tea drinks. Representative brands are: Teaka (tea + coffee), Chef Kong’s tea + milk, Cha pi (tea + fruit juice) and Hongchajun (tea + probiotics).

Multinationals like Coca Cola cannot afford to miss out on the popularity of tea beverages in China. The company has launched a range of tea drinks branded Chunchashe ‘Genuine Tea House’. It is marketed as not containing sugar, but still leaving a sweet aftertaste. It comes in green, black and Wulong flavours.

Herbal tea

Traditional Chinese Medicine (TCM) is making an effort to cash in on the increasing interest in health foods among Chinese consumers, as has been introduced in earlier posts. The market value was estimated at more than RMB 40 billion late 2015 and is expected to grow to close to RMB 20 billion in 2020.. A very prominent application of medicinal herbs as food ingredients are the herbal teas that have become popular during the past few years. The first and most popular, Wanglaoji, is still based on a traditional recipe. Later herbal teas are marketed as modern health or functional beverages, comparing and competing with Western drinks like Red Bull. A very recently launched product in this category is Good Night (Wan An), produced by Wan’an Technology Co., Ltd. (Beijing). Ingredients are said to include:

natural GABA, theanine, chamomile and spina date seed

Wanglaoji launched its own cola drink, Wanglaoji Cola, in January 2018. The company promoted it during the Davos Summit.

The value of the Chinese tea beverage market in 2020 exceeded RMB 100 billion.

Coffee beverages

Coffee being such a recent arrival in China, so closely linked to a Western lifestyle, it seems odd to find it as an officially sanctioned subcategory of beverages. However, they have become quite popular. Perhaps they are easier on the Chinese palate than the basic black brew. The have been introduced in this blog before, in a separate post.

Plant beverages

This category includes drinks made from the juice of vegetables and fruits, in various degrees of concentration. Cereal based drinks are also included. A subtype that is especially popular in China is called ‘fruit tea’ (guocha) in Chinese. The best English translation would be ‘nectar’. The are relatively viscous drinks with carrot or hawthorn pulp as the main ingredient.

In 2016, China’s fruit juice retail volume was 134.47 mln hls and retail sales reached RMB 100.914 billion, up 1.88%. Main brands in the Chinese fruit juice market include Uni-President, Chef Kong, Nongfu Spring, and Huiyuan. China’s top producer in this category is Huiyuan Fruit Juice (Beijing). The company was once an acquisition target of Coca Cola, but the deal was vetoed by the Chinese cartel watchdog. Huiyuan recently launched a range of juices in Malaysia under the Yami brand.

The latest addition to the fruit nectars is Zaoshanzha, a drink made from dates and hawthorn by Haoxiangni.

In terms of taste, orange juice is still the largest category of the fruit juice market in China, There are some differences in taste between the north and the south in China. Apple, peach and pear consumption is relatively high in the north market. Pure juice (‘not from concentrate’) is the growth point in this industry. Chinese women have greater demand for juice, which is related to the pursuit of a healthy figure.

Another popular new subtype is formed by the fruit vinegars. These beverages have become in vogue in the years 2015 – 2016 as health products that help burn fat. In the early stage, it looked as if they would become a success, cashing in on the general trend towards more healthy food in China. However, the tide seemed to turn mid 2018, when a prominent brand, Tiandi Nr. 1 (Tiandi Yihao)’s semi-annual report showed a turnover almost half that of the same period of the previous year.

Flavoured beverages

The literal translation of the Chinese definition of this category is: drinks made by combining food flavours, sugar or sweeteners, or acidifiers. We probably could also refer to these as: designer beverages. It is not always easy to distinguish these from other categories. If you boil tea leaves and the add other flavouring ingredients to the filtered liquid, you would have a tea beverage. However, a drink whose ingredients list includes tea extract, would count as a flavoured beverage.

Nutritious beverages

These include sports drinks and other functional beverages. This category started to boom in the course of 2016. As a result, Red Bull is confronted with an ever growing number of domestic competitors in China. One of the frist challengers (August 2016) was a vitamin drink by Want Want, presented in a gold-coloured can.

This product category is getting so popular, that a dairy company like Yili launched an energy drink of its own in April 2018: Huanxingyuan.

Solid beverages

These are sold in powdered from and infused before consumption. There is at least one traditional Chinese drink typically sold as such: suanmeitang or sour plum drink (literally: soup). A more recent, but still traditional, product is instant soy milk. Many members of the other categories are now also available in powdered form.

The picture shows Yiben brand suanmeitang, which contains the following ingredients:

Senke Beverages has launched an innovative type of suanmeitang adding traditional Chinese medicinal herbs, marketed as ‘Lotus Leaf Suanmeitang‘, in the summer of 2018. Apart from quenching thirst, it is said to lower cholesterol and have a certain slimming effect.

Daring launches – low survival

Chinese beverage makers are quite daring in launching newly developed products on the market, where Western multinationals would organise more pilots to test the products’ reception by consumers. However, a recent survey by the China Food Industry Association reveals that only 5% of newly launched Chinese beverages survive. I guess that is test marketing the Chinese way.

How do Westerners appreciate this?

Are you getting bored with my academic stories? No problem, you can now relax watching this home brew video in which a Western lady living in China introduces here own favourite Chinese beverages.

Here is another Top 5, but then of the most bizarre Chinese drinks.

Latest trend: odd flavours

The structure of the Chinese soft drinks market is undergoing rapid changes. Consumers are developing an awareness of personality, paying more attention to individual needs and preferences. This has created a market for what Chinese have started to call ‘odd flavour water (guaiweishui)’. Laoshan, China’s first and for a long time only producer of mineral water, has launched Baishecaoshui (literally: white snake grass water). It is based on Baishecao (oldenlandia). Hey Song Sarsaparilla from Taiwan is also gaining popularity. The current top producer of mineral water, Nongfu Spring (see above), has also launched odd flavour drinks: Oriental Leaves (Dongfang Shuye), which does not contain herbal extracts, but a mix of flavourings and nutrients, and Red Pointed Leaves (Hongse Jianye), which contains extracts from American Ginseng, green tea and bamboo. This market is extremely volatile. The survival rate of new drinks is generally about 10%, and is now dropping to 5%, according to recent market studies. These products are catering to the young and young Chinese consumers have a low brand loyalty where food and drinks are concerned.