Babao Porridge (Babaozhou, Babaofan), a sweet rice porridge stuffed with dates, lotus seeds and other fruits, is an extremely interesting example of a traditional product revived by industrial production. The concept of babao is used in more traditional foods, e.g. zongzi, filled steamed rice cubes wrapped in leaves, which are introduced in a separate post of this blog.

Present day Babao Porridge is derived from a southern type of porridge called Laba Porridge. La refers to the La month, the last month of the lunar calendar and ba (‘eight’) to the eighth day of that month. On the 8th day of the lunar 12th month people used to prepare a porridge using eight or more ingredients to celebrate the end of the year. Another story explains the custom as a Buddhist tradition.

Laba porridge was first cooked as a sacrifice for ancestors and gods during Laba Festival as a part of winter worship. In an agricultural society, the 12th month or layue (腊月) was a time when families consumed some of their stores from the harvest season. Cooking a porridge with rich and varied ingredients is a way to celebrate a prosperous harvest for the year, in hopes of a better one to follow.

Just like Christmas overtaking the ancient Roman holiday of Saturnalia, when Buddhism arrived in China, it stamped its own influence on this local tradition. For Buddhists, Laba Festival is also Buddha’s Enlightenment Day.

The legend says that Shakyamuni, after 6 years of seeking enlightenment by living frugally, once sat down under a tree, dead tired. A woman herding cows saw him and prepared a simple porridge for him using course cereals and wild fruits. Shakyamuni was so revived from eating a bowl of that porridge, that he immediately gained enlightenment. From that day on, Buddhist Temples prepared a similar type of porridge on the 8th of each 12th month.

With the increasing pace of life, modern Chinese are less and less willing to spend several hours a day in the kitchen. This includes less frequently prepared foods like Babao Porridge.

The basic production process is easy enough. The raw materials are mixed and cooked, cooled and then packed in cans, similar to those used to pack soft drinks. In this way, the porridge can be easily consumed as a convenient food, while travelling, as a snack during office work, etc. A plastic spoon is usually attached to the can, so the traveller does need to pack a metal spoon from the kitchen either.

Buddhist monestaries have to abide by the law as well, so more and more temples are producing laba porridge in a semi-industrialised clean way, to ensure that the faithful do not have to pay dearly for enjoying a bowl of laba porridge with food poisening. On the way, it earns the monestary a lot more income as well.

Formulation

The most essential aspect of the production of Babao Porridge is the combination of emulsifiers and thickeners. Babao Porridge consists of a viscous liquid part and solid parts. Manufacturers need to formulate the product in such a way, that the solid parts are more or less evenly distributed over the liquid part upon opening of the can.

A number of Chinese manufacturers of emulsifiers and thickeners supply products specially formulated for Babao Porridge. Some sources propagate CMC as the most appropriate thickener for this application.

A combination of CMC and a low calorie high intensity sweetener to replace the sugar will not only provide an authentic mouthfeel, but also decrease the caloric value.

Industrial recipes for so called ‘low calorie Babao Porridge,’ proposed by manufacturers of ingredients use sticky rice as the macro-ingredient, where part of the rice can be replaced with pumpkin. Various combinations of fruits (dates are most popular) and nuts (including peanuts) are added. Frequently suggested micro-ingredients and additives: pumpkin powder, xylitol, oligoxylose, CMC, konjac powder, and EDTA.

As a result of all the recent food safety problems, Chinese consumers have become more aware of ingredients and started asking if one food really needs so different ingredients. A recent article (24/9/2014) criticises the use of xanthan in one brand of Babao Porridge. Xanthan is known in the porridge industry under the nickname zhoubao, literally: ‘porridge treasure’. The reporter believes it is a means to hide the lack of skills of the manufacturer to produce a proper porridge.

Top brands

The following brands are recognised as China’s top brands for Babao porridge

Yinlu

The Yinlu Food Group was established in Xiamen (Fujian) in 1985 as producer of canned food and beverages. It is still one of China’s top producers of protein drinks. It now operates production units in Shandong, Hubei, Anhui and Sichuan. Nestlé has acquired a controlling stake in Yinlu, nut has announced that it intends to sell that stake again early 2020.

Wahaha

The Wahaha Group was established in Hangzhou (Zhejiang) in 1987 as a private company operated by a school, producing tonic for school children. The founder and CEO, Mr. Zong Qinghou, is currently one of China’s richest entrepreneurs. Wahaha has 150 subsidiaries in all regions of China, employing 30,000 people. It ranks among China’s top 500 companies in 2014 It is a relatively new player in this market, but has rapidly risen to this position. The range includes a babao porridge sweetened with xylitol. Wahaha has started a new campaign for its canned porridge range in January 2015, stressing that the company is being loyal to the Chinese tradition of porridge making. The following picture says that Wahaha’s Babao Porridge ‘tastes just like mother used to cook it’

Wahaha has launched another type of nutritious Babao Porridge mid 2018, under the Qingzhi brand.

Ingredients:

Koji, plant sterols, sugar, glutenous rice, barley kernels, red beans, maltitol, black rice, peanuts, red kidney beans, hulless barley, tremella, lecithin, sucrose ester, fatty acids, sodium tri-polyphosphate, acesulfame-k, EDTA-2Na, sucralose, water

Qinqi

Based in Guangzhou (Guangdong), Qinqi was the first in China to launch Babao porridge in cans, which created the market for ready to drink Babao porridge. Although no longer the number one brand, Qinqi still bears the honorary name ‘porridge king’.

Qinqin

This brand is owned by the Xinxin Food Group, established in Yangzhou (Jiangsu) in 1991, by a local factory and a Taiwan investor. It produces a range of convenience foods, including Babao porridge.

Tongfu

The name of the producer, Tongfu Bowl Porridge Co., Ltd., betrays that it is dedicated to producing exactly that: porridge in (plastic) bowls. Tongfu was the first to introduce this type of packaging in China. It is considerably lighter than the canned version. It is located in Wuhu (Anhui)

Corona was good for Babao porridge

Babao porridge sales went through the ceiling during the first quarter of 2020, when the entire Chinese nation went into quarantine at home. It turned out to be the ideal corona food, besides instant noodles and other packed fast foods.

More nutritious and high end

Babao porridge entered the high end sector in 2022, when Huangxiaozhu launched its series of zero sugar low fat nutritious babao porridge. Flavours included coconut-water chestnut and and black sesame – taro. The packaging was also inspired by the ongoing nationalist trend (guochao).

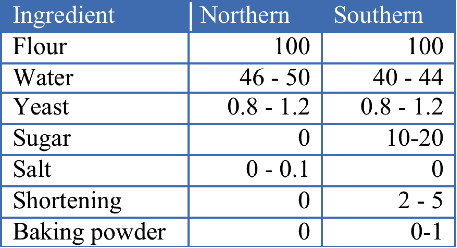

Chinese steamed bread is a fermented wheat flour product that is cooked by steaming. It is big business. Insiders claim that steamed bread is good for approximately 60% of the total flour consumption in Northern China and 20% – 30% in Southern China.

Mantou can be eaten alongside dishes, or dipped in various sauces (like furu, a type of fermented bean curd). Stale mantou are often fried, as a whole or in slices.

The preparation process is similar to that of western-style bread, but the final product is steamed, not baked in an oven, so there are some differences in appearance and shape. Steamed bread is white and has a soft, shiny surface. The common types of steamed bread weight about 30 – 120 gr.

The following table shows a typical formulation of Northern and Southern steamed bread (unit: %).

This basic recipe can be varied by adding a number of ingredients: soy flour, milk powder, colorants, etc.

A major trend is the beginning of industrial production of steamed bread. Until recently, steamed bread was made exclusively at home. With increase of the pace of life in urban China, Chinese city dwellers spend less and less time in the kitchen and cumbersome processes like preparing steamed bread are the first to be ‘outsourced’ to professionals, like local cooking shops or workshop like factories that sell their products to street vendors and local shops.

There are even machines that can produce mantou in a continuous process.

Here is a video showing the industrial production of mantou.

Formulation

A tough technical and logistic problem for companies in developing steamed bread production on a national scale is that it is difficult to keep fresh during long storage and transportation. Major steamed bread producers have appeared in many Chinese cities during recent years (e.g. Sanshui Food in Beijing, Zhengrong in Zhengzhou (Henan) and Ganqishi in Hangzhou (Zhejiang)), but these mainly supply outlets in their own home region.

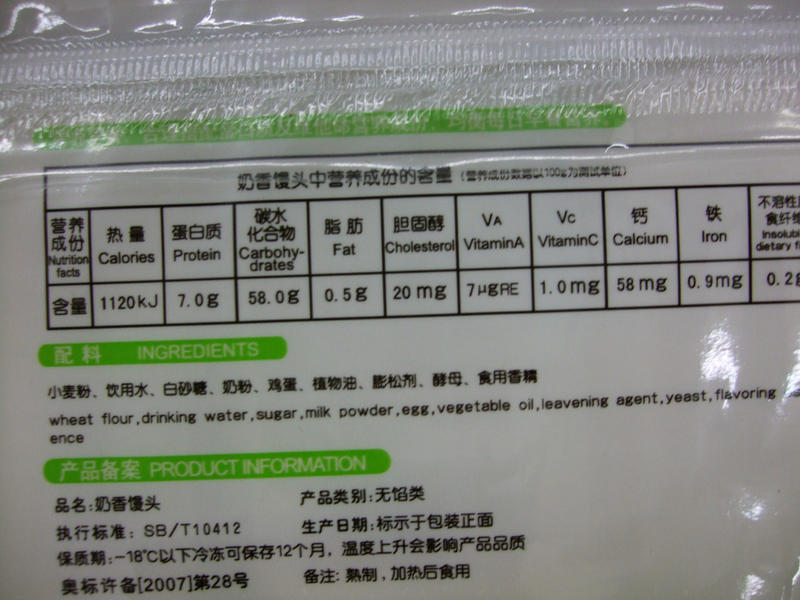

Here is a picture of the ingredients and nutrition information of Sinian’s ‘milk flavoured mantou‘

A logistic problem for companies in developing steamed bread production on a national scale is that it is difficult to keep fresh during long storage and transportation. Major steamed bread producers have appeared in many Chinese cities during recent years, but these mainly supply outlets in their own home region.

Healthy food

Some Chinese nutrition professionals are promoting mantou as a health snack food, because it is low in salt, sugar and fat. They definitely have a point, as long as you eat them fresh. Due to their high water content, mantou are an attractive medium for the aspergillus flavus mold that produces the carcinogen aflatoxin.

Special improvers

Industrial production of mantou is still in its infancy, but the R&D in this topic has already led to the appearance of specially formulated steamed bread improvers. As these improvers include enzymes, this is one of core trends to be monitored by suppliers of enzymes. Enzymes used in various commercial products (also see my blog on dumplings) are: a-amylase, hemicellulase (xylanase), lipase and glucose-oxidase for improving the dough handling properties and a larger volume yield. A Chinese food technology site provides the following recipe for a specially formulated flour improver for mantou:

Ingredient

parts

Calcium stearoyl lactate

30-50

Monoglyceride

10-20

Vitamin C

6-10

Fungal alpha-amylase

0.6-1.2

Xylanase

2-3

Alkaline buffer

12.5-18.75

Regional varieties

Huifang Food (Hebei) has recently launched an industrially produced local type of mantou called qiangmian mantou. The production process adds additional flour to the dough, which gives the end-product an extra shiny finish. This development indicates that the industrial production of steamed bread in China has entered a new stage.

In Jilin, an importer of Russian flour is promoting it as the best raw material for the production of mantou. According to that supplier, Russian wheat has a longer growing period, the soil is of higher quality and the flour is better processed. I have not yet been able to verify this myself.

Mantou are especially popular in Qingdao (Shandong). Wanggezhuang Street in that city is lined with mantou sellers. One of these even won a gold award at an international culinary competition in Paris in July 2016.

Mantou for dessert

Chinese cuisine does not really have desserts, but serving a sweet dish at the end of a meal is getting more and more popular in China.A special type of mantou is eaten as such a dessert. They are deep fried and served with a dip of sweetened condensed milk. This dish has been invented in Guangdong with obvious Western influences (compare my blog about traditional Chinese dairy products).

Potato mantou – a revolution in Chinese staple food

The China Academy for Agricultural Sciences and Haileda Food (Beijing) have jointly developed a type mantou that consists for 30% of potato. The product was launched on June 1, 2015. This is yet another step in the process of changing the potato into a major staple of Chinese cuisine (see my post on potatoes). The researchers have announced that they reached the next step in this R&D project, increasing the percentage of potato to 55% on June 8, 2016. Other potato products will also be developed, like: noodles, or bread.

Focus company: Maixiangyuan

Maixiangyuan Food Co., Ltd. In Shandong is an interesting company in the industrial production of mantou. It can produce 38 types of mantou and has a production capacity of 25 mt per day. When the company was founded in 2009, it mainly hired people who had lost their job in obsolescent industries, thus giving them an income again. Maixiangyuan is the only industrial manufacturer of mantou that does not use any chemical additives. Its mantou are produced using an in-house developed process based on the traditional recipe. It has 12 machines for producing mantou and bread and 15 food trucks to sell their products directly to consumers. Besides mantou and bread, Maixiangyuan also produces baozi (stuffed steamed buns) and zongzi. The company operates 6 shops of its own and sells through another 600 retailers in surrounding cities and Ji’an, Shandong’s capital. It is China’s only mantou manufacturer with a green certification, and the first to get listed on the stock exchange in 2015. Maixiangyuan has also invested in wheat growing and other related activities, with the aim to control the entire value chain.

Mantou shares

Zhongyin Beverages (Henan) has been operating a mantou and baozi chain for a number of years. They are especially popular in Shanghai. Zhongyin’s turnover was RMB 990 mln in 2018 and rumour has it that a considerable part of it is derived from steam buns, with our without stuffing. The company announced that it intended to get listed in 2019.

Filled mantou

Once mantou entered the ranks of manufactured food, the door opened to designing new types of mantou, in particular those filled with all kinds of stuff. Chinese like that and most bread sold in Chinese convenience stores has some kind of filling. This picture shows a product of Yima Gongfang, filled with several types of staple food like sweet potato. In fact, the product contains more such staples, while the mantou part has been reduced to a skin holding all fillings together.

Jiang is one of the most basic types of traditional Chinese condiments; yet it is not very well known outside East Asia.

Jiang was probably the predecessor of soy sauce, which is called jiangyou (jiang oil) in Chinese. While soy sauce is liquid, jiang is a paste.

The production process of jiang also resembles that of soy sauce. The main ingredients are soybeans and a starch source: rice, wheat, etc. The starch source is hydrolyzed with a mould, resulting in a very basic type of koji (qu) that is also used for the production of traditional Chinese liquors (baijiu) or the Japanese sake.

Soybeans are soaked and boiled, after which the koji and the boiled soybeans are mixed with salt and water added. That mixture is fermented until a black salty paste is formed.

There are many types of jiang. Some are sweet, while others are fragrant because of the formation of alcohols (produced by added yeast).

Various spices can be added as well. A very famous type is the spicy doubanjiang of Pixian in Sichuan. The sweet jiang used with Peking Duck is made of wheat flour, without using soybeans.

Jiang is presently undergoing a process of modernization. Each type of jiang has its typical flavour (unique mix of the Five Flavours), smell, consistency, colour, etc. Additives are needed to guarantee a mass produced product of consistent quality. Moreover, the time and distance between production and consumption of jiang is also longer and farther than before. This calls for sufficient preservation methods.

Industrial production of jiang is an interesting new market for enzymes. The first enzymatic processes used a single enzyme: a-amylase. Some of the companies produced the enzymes in-house. Later multi-enzyme processes were adopted as well, using a mix of a- and b-amylases and neutral protease.

The following video introduces the industrial production of jiang. It is in Chinese, but food technologists will be able to get the gist.

A major trend is the development of special jiangs for specific dishes. Now you can buy ready to use Peking Duck jiang, dandan noodles jiang (a typical Sichuan type of spicy noodles), huiguo pork jiang (a spicy dish, again from Sichuan), jiang for cooking fish, etc.

You can stir fry some pickled vegetables, add a spoon of dandan noodles jiang, poor it over a bowl of cooked noodles and eat your dandan noodles.

With the proper packaging and marketing campaign introducing these modern jiangs to the Western consumer, these products could mean lucrative business for an astute entrepreneur.

If you want to understand the basics of how the Chinese government creates a level playing field in business, in particular in relation with foreign products, study this post.

Developments in this business have been literally dramatic, and it is directly related to the most precious item of the majority of adult Chinese: their, until recently, only child.

Melamine

A synopsis of what had happened from 2008 up to the present day.

In the year of the first Chinese Olympics it was discovered that several brands of domestic infant formulae contained melamine, a compound that make the protein content of milk appear higher in the standard tests as conducted by dairy companies. It caused about 300,000 babies to get seriously ill, with a small number of deaths.

As a result, the market share of the domestic brands dropped even lower that it already was at that time. However, a number of smaller brands deftly used this situation to gain market share, as is clarified in the following video

Hubris

Foreign brands believed that a Golden Age had come, in which they could virtually set the market price of formulae in China. European and American brands increased their prices almost every couple of months, without naming a valid reason.

Chinese consumers were so eager to get their hands on foreign products, that Chinese on foreign trips were asked by the relatives to buy up any formulae they could get their hands on, as products there were much cheaper than in Chinese supermarkets. In countries like the UK or The Netherlands, quotas were issued for the number of packagings single customers could buy at one time.

Then the gods punished the foreign suppliers for their hubris. Fonterra came with the news that its whey powder could have been contaminated. That shocked China.

Leveling the playing field

The Chinese authorities grabbed the momentum of the falling consumer confidence in foreign formulae to start a media campaign trying to restore the reputation of domestic product.

To support this, they launched an investigation into monopolistic activities by foreign suppliers of infant formulae. A good example is the accusation against Danone that it had bribed hospital staff to feed babies first with their Dumex formula, to get them hooked on that brand. Most foreign suppliers were found guilty, and those who have not fully cooperated with the investigation, were heavily penalised.

However, a survey among young parents conducted at that time noted that the latter were still more confident in foreign formulae.

Who the were the guilty parties in all that commotion? I believe all of them.

The domestic suppliers have forfeited their favourite position with relatively low cost to produce good generic infant formulae. Instead, many of them, including the then market leader Sanlu, were attracted by the short-term opportunity of increasing their income by adding ‘protein power’ (read: melamine) to their milk. The larger Chinese producers usually control the entire value chain, from cow to formula. This means that the melamine was added right under their noses and it is hard to believe that they were not aware.

The foreigners have been too greedy. The constant price hikes increased the financial burden for young parents. Without those unreasonable price increases, the authorities would probably have left their high market shares untouched.

The international media have been biased towards the domestic companies. Chinese companies like Sanlu were heavily criticized in the Western press for trying to hide the first reports about health problems, not to spoil the national Olympic party. The same media were a lot milder towards a company like Fonterra, the then partner of Sanlu.

New system of accreditation

The Dairy Association of China (DAC) has begun to promulgate ‘state endorsed milk powder manufacturers’. Here, ‘milk powder’ mainly refers to infant formulae. Severa; have so far been stamped this way. Others are allowed to produce as well, but the state only guarantees the quality of the suppliers on its shortlist. It will surprise no one that China’s top dairy company Yili (see the item on China’s top brands of 2014) heads the list.

Foreign brands need to be registered and are not allowed to be active in China with more than 3 brands or 9 different products.

The best that can come out of this mess is that there now is finally an opportunity that the Chinese market for infant formulae becomes a level playing field in which domestic and foreign brands can compete fairly.

Inbound foreign investment- new style

Statistics seem to confirm that it works. Four of the five most popular infant forumula brands in China were foreign brands. This is happening in spite of recurrent media reports about batches of imported infant formulae being rejected by the Customs inspections.

A number of international players try circumvent those problems at the customs through setting up local production.

FrieslandCampina of the Netherlands entered into a joint venture with Huishan Dairy (Liaoning) to jointly produced infant formulae in October 2014. The joint venture will own Huishan’s facility in Xiushui (Liaoning). During the obligatory ceremony, the Dutch partner’s CEO said that he was ‘proud that FrieslandCampina will be part of the first joint venture between a Chinese and a foreign dairy company that will locally source, manufacture, market and distribute infant milk formula’. That statement called for correction, as a number of international investors have preceded FrieslandCampina, with varying results. A few years later, mid 2017 to be precise, the joint venture got into serious problems, when the Chinese partner Huishan was accused of fraud. FrieslandCampina opted to buy out their local partner early 2018 and now operate a wholly foreign owned company alongside their partner. This situation is far from ideal, as it renders FrieslandCampina’s local production in China extremely vulnerable.

Later that same month October 2014, Danone announced that it was to subscribe to a private placement by Yashili, one of China’s leading infant milk companies. Upon completion of the subscription, Mengniu, currently Yashili’s majority shareholder, will hold a 51.0% equity interest and Danone will hold 25.0%. Danone and Mengniu want to use this expanded alliance to grow Yashili and develop a wide range of products that meet the very highest standards in this category. Through their alliance, Danone, Mengniu and Yashili intend to expand and strengthen their cooperation in the infant milk formula business in China. The parties will study the possibility of a minority equity investment by Yashili in Danone’s subsidiary Dumex China.

Reaping success

Domestic brands have started recouping market share in 2018, fastening the pace in 2019. A leading player in this developed is newcomer Junlebao (Hebei). Founded in 1995, Junlebao used to make only yogurt. It added infant formula to its product line in 2014 to help revitalise the product’s domestic presence. In the following five years, the company established a whole industrial chain, including a planting pasture, a base for breeding cows and quality-control centre. By 2019, the company had 17 production plants and 10 breeding bases with more than 60,000 cows across China. To improve the quality of its milk sourcing, Junlebao has developed a high-standard cow breeding system, which consists of raising the animals in comfortable barns, feeding them with high-quality fodder and using high-tech machines to milk them. The market share of domestic formulae in China increased to more than 60% in 2018, thanks to Junlebao.

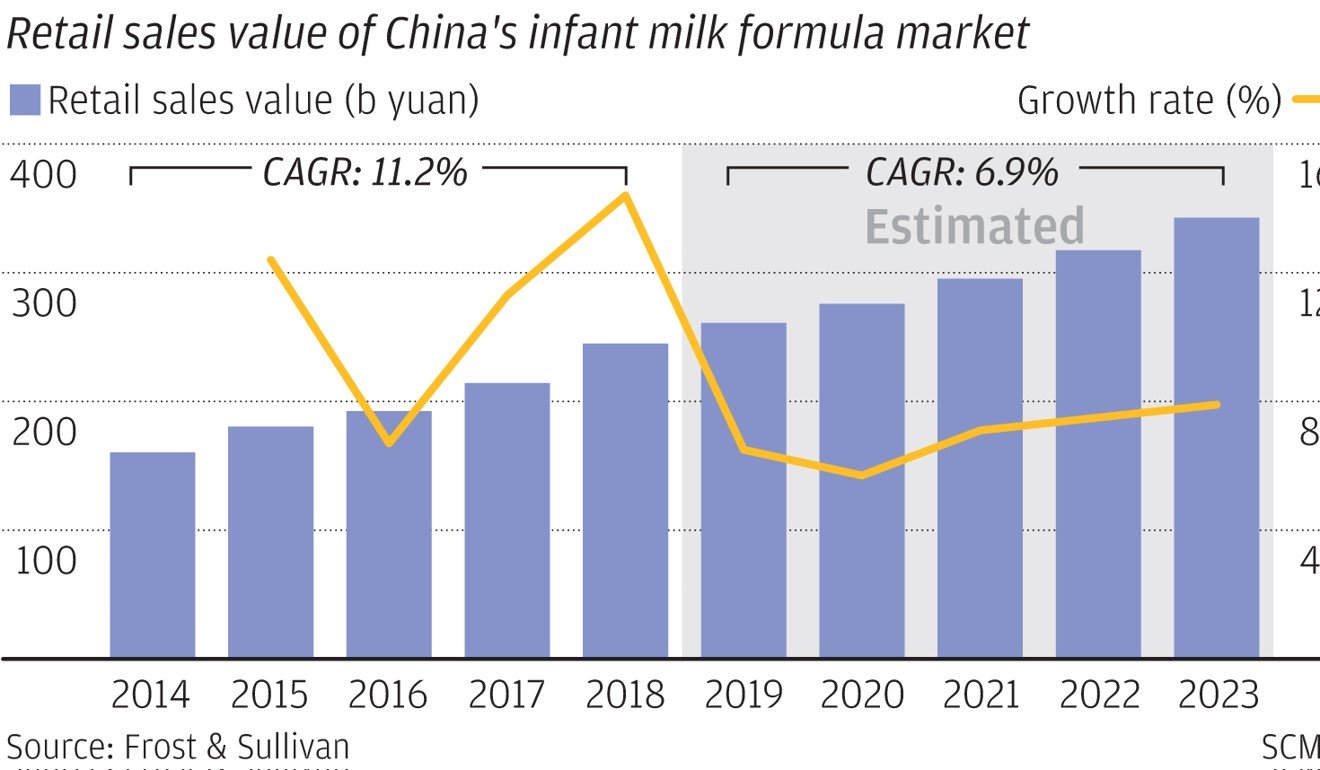

The following tables show the development of the value of the market and estimates for the years up to 2023 by various researchers.

Year

ValueRMB billion

2016

157.10

2017

187.30

2018

222.10

2019

257.86

2020

295.51

Outbound foreign investment – recent but rapid

A number of Chinese companies try to overcome the problems in the industry by acquiring foreign infant formula producers. Formulae imported from those plants then have a hybrid Chinese and foreign identity.

Bright Dairy & Food (Shanghai), China’s third-biggest dairy company by volume, has bought a majority stake in Canterbury milk processor Synlait Milk for $82 million in 2010. Synlait, which abandoned a planned $150 million share sale in 2009 due to a tepid response, is a joint owner of its processing company with Bright Dairy, while keeping and operating its farms through a separate company.

In 2014, Bright bought a majority stake in the Israeli manufacturer of infant formulae Tnuva.

September 2014, Guangdong real estate group Evergrande (which also owns the province’s main football team) acquired the New Zealand company Cowala Dairy.

Internet interaction analysis

An interesting development is that the China Statistical Information Service Centre (CSISC) has started analysing online consumer interaction about brands. CSISC published the following table showing consumer interaction about infant formulae in the 2nd quarter of 2014 today (19/9/2014).

The brand most discussed is Junlebao (also featuring in my blog on old yoghurt), followed by Dumex and Mead Johnson. The brands that the central government has been heavily supporting in the above described campaign, like Yili, ranks 7. Obviously, brands can also turn up high in this graph, because consumers may share negative experience with it. Still, CSISC analysts believe that this outcome shows that newcomer Junlebao’s low price strategy is reaping results. Junlebao received class A certification of EU’s BRC Food Safety Global Standards in September 2014. Junlebao’s milk powder would be qualified to enter CIES’ 200 supermarket groups in the world. I would like to add that it also proves the central authorities right: the Chinese market for infant formulae is a level playing field now. The international brands are still favourites, but local entrepreneurs have ample space to move, as long as the get their strategy right.

Top formulae of 2019

The following table shows the top 5 infant formula suppliers in China of 2019

Company

Market share(%)

Nestlé

14

Feihe

13

Danone

10

Abbott

7

Mead Johnson

6

More babies, bigger market . . or not?

The market for infant formulae has changed in China, when the government decided that couples who both were only children were aloud to have 2 children. Even though fewer eligible couples responded positively than expected during the first few years after the decision, this is now gradually leading to a small baby boom. That and the continuing growth of an affluent middle class, has boosted the sales of most players in this market. However, this does not mean that China will once more become the paradise of multinationals in this field. It is a genuine level playing field now, and a growing one, with opportunities for all companies that are willing to play by the rules.

However, in spite of the new policy, 15.23 mln babies were born in China in 2018, 2 mln fewer than in 2017. Therefore, insiders estimate that the consumption of infant formulae in 2019 will be approximately the same as in 2018, and will decrease with 2% in 2020.

Innovative products – a step up the ladder for the Chinese industry

Beingmate (Hangzhou, Zhejiang) has received official approval for the production of infant formulae for prematurely born babies and over-birthweight babies in August 2019. While these are not new types of formulae, Beingmate was the first in China to launch these specialist products. Fonterra is a major shareholder of Beingmate. After the repositioning of the regular Chinese infant formulae, this development could mark the beginning of the rise of the Chinese industry on the technological ladder.

The organic way

The sales of organic infant formulae increased significantly in the course of 2019. Buoyed by the rising demand, several multinational companies like Germany’s Hibb, Switzerland’s Nestlé and its unit Wyeth are not only witnessing resurgent sales. Hipp is looking to further expand its presence in the e-commerce market. The company witnessed annual growth of about 20% in China in 2019, making the country its second-largest market after Germany. Besides, Wyeth, the baby and infant formula unit of Nestlé, has introduced Illuma 3 organic products for Chinese parents since 2017. Its research released in October shows that the sales of organic infant and maternity products grew by 33% year-on-year in China, creating a generation of “organic mothers”. US infant formula maker Mead-Johnson introduced its grass-fed Enfagrow to Chinese consumers in September 2019.

If this article is of interest to you, you may also like:

What do Chinese eat, when they have something to celebrate: dumplings! Frozen dumplings are a major food product in China. More than 10,000 companies related to that industry were registered on 8/11/2023.

Dumplings are small round sheets of dough (flour + water) filled with minced meat + condiments + vegetables. After a piece of filling has been placed in the centre of the dough, the latter is folded into a shape that vaguely resembles a horn, in particular that of a cow. This shape is the origin of the Chinese name: jiaozi. Jiao is ‘horn’ in Chinese and jiaozi means something like ‘small horn.’ Later, the link between dumplings and horns eroded and as dumplings became an important part of Chinese cuisine (in particular in the Northern part of China), a special character was coined for this food.

Dumplings are an old food, as is shown by various archeological finds. According to an archaeologist from the Museum of Xinjiang Uygur autonomous region, the three dumplings unearthed in the region’s Turpan area were determined to have been made during the Wei, Jin, Southern and Northern Dynasties (220-589). Archaeologists also found two complete dumplings made during the Tang Dynasty (618-907) in Turpan. The dumplings were 5 cm long, 1.5 cm wide and resembled the new moon in shape. Further research revealed the dumpling wrappers were made from wheat flour and the stuffing was meat.

According to legend, during the Eastern Han Dynasty (AD 22 – 220), there lived a famous physician of Traditional Chinese Medicine, named Zhang Zhongjing, who introduced dumplings. Once, the “medical saint” was returning to his ancestral village after a long period of absence. During that winter, a febrile disease was turning into an epidemic. Many poor people were submitted to the cold weather because of the lack of warm clothes and sufficient food and suffered frostbite, mainly around their ears. Seeing their condition, Zhang was determined to help them rid of the frostbite. He cooked lamb, black peppers and a few medicinal herbs, shredded them and wrapped it in the scrape of dough skin. He shaped them like ears and boiled them. Everyone sick person was given two ‘ears’ along with a bowl of warm soup. After a few days, the frostbite was gone and the epidemic was under control. Since then, most people begin imitating Zhang’s recipe with additional ingredients like vegetables and other kinds of meat to celebrate Chinese New Year.

Already in traditional Chinese cuisine, some variation was applied in the preparation of dumplings. While pork was the main type of meat for the filling, beef and mutton were also used, combined with different vegetables. In Southern China seafood, especially shrimps, were used as filling as well. Vegetarian types of dumplings with, e.g., eggs, cucumber slices and glass noodles, etc. were known as Three Delicacies Dumplings.

Dumplings have developed into a Chinese type of fast food and special small restaurants only serving a wide variety of dumplings can be found on street corners of Beijing and other Northern cities.

Dumplings are THE Chinese festival food par excellence. Look at this video to learn more about the role of dumplings in the Chinese New Year celebration.

Industrial production

The dramatic change in life style of the past two decades has had a great impact on dumplings. While making dumplings (preparing the filling and the dough, folding the dumplings and, of course, eating them) used to be the number one family occupation during the weekends in the North, the quickening of the pace of life has decreased the interest in this time consuming preparation. It has not, however, tempered the love for dumplings of the Chinese. Towards the end of the 20th Century, a number of food manufacturers started experimenting with the industrial production of quick frozen dumplings (one of these, Sanquan, already ranks among China’s top food brands), to cash in on the increasing pace of life of Chinese consumers. the current production is approximately 15 mln mt p.a., with 100 – 150 kt exported.

The latest news (October 2014) is that China’s top fruit juice producer, Huiyuan, is considering to invest in the production of quick frozen dumplings. This is a clear sign that dumplings are perceived as a lucrative business.

Apart from the quick frozen mass production, there are also machines that produce dumplings for use in restaurants and other types catering business.

This video shows part of the production of quick frozen dumplings at Sanquan.

Volatile market

The dumplings market consists of a several types of companies: manufacturers of dumplings, manufacturers of machines, manufacturers of ingredients, dumpling shops, catering businesses, etc. This market is very volatile. While new companies are registered each year, a number of companies disappears as well, due to bankruptcy, closing down by the owners and other causes. The following table shows the number of new companies and disappearances in the period 2019 – 2023; unit: number of companies.

Formulation

This development has created exciting new challenges for ingredients suppliers (see my blog on the Quick Frozen Tradition). First of all, do the manufacturers of frozen dumplings buy their own raw meat, vegetables, etc., or do they purchase minced meat and chopped vegetables. Especially for the meat, it seems more appropriate to have meat processing companies supply ready-to-use minced meat. Other ingredients used in the fillings include: flavours, taste enhancers, and dehydrated spices. The dough poses challenging opportunities for suppliers of enzymes. To mention one example: fungal α-amylase can lower the viscosity of the of the gelatinized starch, generating dextrin and a small quantity of glucose and maltose, which will make the dumplings softer and not stick to the teeth.

Here is a recipe for quick frozen dumpling skin that I picked up from a food technology site.

Ingredient

Volume (gr.)

High gluten flour

100

Modified potato starch

20

Wheat Gluten

6

Sodium hexametaphosphate

0.26

Sodium tripolyphosphate

0.14

sodium pyrophosphate

0.05

Sodium bicarbonate

0.2

CSL-SSL

0.3

Salt

1.5

Water

35

Guar gum

0.3

Shortening

4

Clean dumplings

Concepts like Clean Label have also reached China and started to get serious around 2022. However, the Chinese interpretation of ‘clean’ seems to be broader or lest strict than the Western. Here is an example of a quick frozen dumpling brand from Eurasia Consult’s database that is advertised as ‘zero additives’ site in China.

The product name is: black pig meat maize fried dumplings

Ingredients

black pig meat (>- 30%), wheat flour, maize kernels, water, carrots, starch, Chinese broccoli, brewed soy sauce (includes caramel colour), vegetable oil, crystal sugar, salt, MSG, white pepper

Special seasoning

The booming industrial production of dumplings and the resulting increased consumption has also triggered developments in related industries. A typical example is the appearance of ‘dumpling vinegar’. Dumplings are traditionally dipped in rice vinegar before consumption. China’s top vinegar brand Hengshun is now also available in a convenient table top packing. The label clearly indicates the motivation for this variety.

Innovation

Haibawang in Shantou (Guangdong) has launched innovative dumplings in September 2014 are ‘fish skin dumplings’. The wrapping of these dumplings contains 40% fish meat (probably in the form of fish paste). This makes them highly transparent. Highbawang has clearly stated that it intends to challenge the top producers of frozen dumplings like Sanquan with this novel product.

A month later, in October 2014, Sinian (Zhengzhou, Henan) has launched a new range of dumplings with well known Chinese dishes like Sichuan Pepper Beef or Lime Beef fillings. Until this launch, the fillings of dumplings, whether home made or produced commercially, consisted of minced meat and a type of vegetable as the main ingredients, with spices and seasoning as added to finish the flavor. Stuffing a complete dish in a dumpling is revolutionary.

The mackerel dumplings of Hongye Food (Shandong) received the status of ‘traditional Chinese delicacy’ in February, 2020.

CP (Zhengda) has launched a range of ready to eat dumplings early 2022, marketed as breakfast dumplings. The are packed in small one-person helpings, also gearing to the growing market for single households.

Dumplings for children

Children are a major market segment for the Chinese food and beverage industry. Although a second child is a possibility now, for parents who are themselves single children, most children in China are still the ‘little emperors’ of the household who are doted on by parents and grandparents. Producers of quick frozen dumplings have also developed dumplings for children. They are marketed as more nutritious than the regular product and the skins are often coloured (typically red or green) to appeal more to the young. Sanquan‘s ‘King Shrimp Dumplings’ ended first in a taste panel test organized before Children’s Day (June 1), 2017.

Vegetarian

Although minced meat is the typical main ingredient of the fillings of dumplings, vegetarian dumplings exist as well. For home cooking, they do not pose a particular problem. However, the transformation to industrial production of vegetarian dumplings has its particular problems, the most prominent being the dehydration of the filling. Jiajiamei Seasoning (Zhoukou, Henan) has developed a seasoning mix specially formulated for vegetarian dumplings to deal with that problem.

(Towards) organic

Another way of distinguishing yourself in the growing mass of industrial dumpling makers is going for high quality, getting rid of unnecessary additives, perhaps going for organic in the near future. Such a company is Chuange (Qingdao, Shandong). Founded in 2009, it produces a range of hand-made seafood dumplings. It markets its products as an industrial reproduction of traditional seafood dumplings eaten by the local fishermen. Its product range even includes sepia dumplings, marked by its distinct colour, not unlike the sepia noodles from Italy, or sepia paella from Spain.

Spin-off products

Dumplings are such a popular food, that it has lead to the development of various products related to the making or eating dumplings. E.g., many producers of vinegar or soy sauce have developed special products for dipping dumplings. Some chefs have started making dumplings using other cereals, like the oat dumplings of the restaurant chain Xibei Youmian.

Eurasia Consult’s database of the Chinese food industry includes 10 producers of dumplings., industrial recipes, and more.

The value of the 2025 Chinese instant noodle market was RMB 123.68 billion; up from RMB 103.9 billion in 2018.

Instant noodles: winners in corona time

In the present times, when governments, companies and people around the globe are bearish about the economy, employment and even the timely supply of food, there are also winners. One big winner in China is the instant noodle. After this special corona vignette, you can read the regular post, which starts with the information that the Chinese instant noodle consumption has started rising again with a few percent annually, after a period of decline. That decline followed a much longer period of spectacular growth. Chinese consumers seem literally fed up with instant noodles and were eagerly looking for a larger variety of instant foods. The manufacturers fought back bravely, launching new types of instant noodles with a broader spectrum of flavours and more and fresher ingredients. Read the details below.

Then came the corona virus, changing the ways Chinese bought and consumed food. This gave an enormous boost to instant noodles. Check out the increase of the sales figures of the first 2 months of 2020 of the top producers, compared to the sales in the same period of 2019.

Company

Increase (%)

Uni-President

297.14

Jinmailang

180.00

Chef Kong

150.54

China has produced 2,246,998.4 mt of instant noodles in the first 5 months of 2020; Henan was the largest region good for 19.54%.

The industry is eagerly taking this opportunity up and is now advertising its modernized types of noodles. I am selecting a few of the most representative aspects.

Great taste

Imperial quality

Broad range of flavours

The regular blog text

One of the most intriguing headlines I read in the Chinese food industry media when I started this blog is in the shape of a question: ‘have instant noodles past their peak?‘ The national output of instant noodles in 2014 was 10,256,640 mt, down 1.55% compared to 2013. Total sales of instant noodles in 2015 decreased with 6.3% and the turnover with 2.6%. The market saw an increase of 0.9% in 2016, positive for the first time since several years. The volume of 2017 increased with an additional 2.8%, but plummeted again in 2018. The value of the market was worth RMB 143.546 billion in the first half of 2019; up 7.75% again. The leading companies filed increasing turnovers for again for 2018 (see below). The market is extremely volatile, but there is a trend towards sanitation, in which the top players grow, while smaller companies disappear.

According to a survey conducted mid 2017, the largest market segment are consumer of the age group 23 – 28, followed by the section 29 – 35. In both groups, women consume significantly more than men.

The following table shows the development of the Chinese instant noodle output from 2010 thru 2018.

Year

volume (mt)

2010

6,881,100

2011

8,275,900

2012

9,467,400

2013

10,307,600

2014

10,256,640

2015

10,178,000

2016

11,039,000

2017

11,032,000

2018

6,695,000

China has produced 5.13 mln mt of instant noodles in 2021; down 6.8%.

The market has been dominated by 4 main players for many years. The following tables shows their market shares from 2005 to 2017. An interesting detail is that the first 2 are Taiwan-based.

Whether instant noodles are on retreat is indeed a bold question. If there is one Chinese food product that has seemingly conquered the world in the sense that it is known and available in supermarkets on all continents it is instant noodles.

Yes, soy sauce was know in most Western countries long before the first pack of instant noodles appeared on the shelves of our supermarkets and yes, instant noodles are probably a Japanese invention. However, it was that huge neighbour of Japan that posed the single largest market for this convenience food and it was through the Chinese diaspora that it ended up in supermarkets in regions like Europe, North America, or Australia. The products on offer in Western shops are not only imported from Asia, but also partly produced by Western companies like Unilever’s Unox brand.

One theory says that the rise of instant noodles was partly caused by the mass movement of surplus rural labour to the Chinese cities. Instant noodles became the favourite food of the migrant workers. It was cheap, tasty and easy to prepare. Migrants have now accumulated enough wealth to move on to more healthy foods, causing a drop in instant noodle sales.

Another surprising factor influencing the decrease of instant noodle consumption in China is booming development of the high speed rail network. In a special post on train food in China, I have reported that railroad stations are important points of sales for instant noodles. However, with the shortening of the time between any two cities, the demand for instant noodles decreases proportionally. This comes on top of the rise in living standard, which makes Chinese rail travellers buy more fancy lunch boxes, on the expense of cheaper instant foods.

Market not endless

The market for instant noodles in China seemed to be growing endlessly. From a convenience snack it has become a regular meal for many white-collar workers. The growing spending power in the Chinese created an ever-larger number of new adaptors for this food. The following video gives an impression about the an instant noodles production line.

What we could notice during the past few years was that the manufacturers of instant noodles had to go into ever-larger lengths to create new flavours and textures, new additions like dried pieces of meat that could be rehydrated like the dried vegetables that were a more traditional ingredient of instant noodles. With hindsight, this can be regarded as a sign that the consumers were getting a little bored and needed to be stimulated again.

Against the background of the many food scandals of recent years, Chinese consumers have grown more conscious of food safety and healthy food in general. While instant noodles are not unhealthy, it is surely not healthy food. Major players are noticing that the need to rid their product of the ‘junk food’ image.

All top manufacturers have already switched from fried to boiled instant noodles, reducing the fat content, which also decreases the need for antioxidants.

Another recent trend is that several producers of instant noodles, even market leader Master Kong, have started diversifying, adding soft drinks or other foods (like biscuits) and beverages to their product range. Their strategists may have read the signs on the wall.

Master Kong, a brand of Taiwan-based Tingyi, is the absolute leader in this market. In 2013, the company operated 23% of all instant noodle production lines in China, was good for 46.6% of the national turnover of the industry and produced 34.5% of the national volume. Moreover, Master Kong was the fastest selling Chinese brand in 2013, for the second time in row. 91.4% of the respondents in the survey had been in contact with the brand. That even this company has stopped placing all its eggs in the instant noodle basket is telling. Tingyi is reporting a serious drop in net profit in 2014. The net profit of the 3rd quarter of 2014 was 13.85% lower than in the same period of 2013.

Tingyi, the owner of the Master Kong brand makes half the instant noodles eaten annually in China, yet revenue is stagnating as middle-class consumers abandon the salty, fatty cups for healthier options. Tingyi is on a mission to reinvent the humble noodle, pouring millions of dollars into customer education, food science, Olympic Games sponsorships and “Kung Fu Panda” movie shorts to convince diners the cheap meal can be part of their gastronomic aspirations. “We want to continue to grow up, and ‘premium up,’ with our Chinese consumers,” Richard Chen, Tingyi’s chief technology officer, said at the company’s Shanghai research centre. “In a couple of years, we will be able to reach the gold standard, which is when you can’t tell our noodles apart from what you would get in a noodle shop.”

The latest innovative move of Master Kong to keep its leading position is launching two sister varieties based on Western flavours: black and white pepper steak.

Innovators at Tingyi once focused on practical advancements such as foldable forks and double-layer packaging so working-class Chinese could wolf down noodles on their commutes. Now, they work out of an RMB 500 mln research complex in Shanghai, with Tingyi tapping the nation’s top food-science university programs and partnering with Japanese companies such as Itochu Corp. to develop chemical-free flavorings and palm oil-free noodles. Master Kong’s turnover of 2018 was RMB 60.686 billion; up 2.94%. Its turnover for instant noodles was RMB 23.917 billion; up 5.73%.

Master Kong launched a range of power bars, marketed as breakfast replacers early 2020.

The company also divested into various beverages. Master Kong’s turnover in the first half of 2020 was RMB 32.934 billion; but only RMB 14.910 was derived from instant noodles.

Master Kong’s main competitor is another Taiwanese company: Uni-President. While Master Kong is still the leader, it is struggling with decreasing sales (-1.51% in the first half of 2014), while Uni-President is still showing, low, increasing sales (1.3%).

There could be some truth in the predictions of the author of the above-mentioned article. We need to wait and see how this market develops. For the time being it remains huge. UniPresidents’s turnover in China of 2018 was RMB 21.772 billion; up 4.6%. Its turnover for instant noodles was RMB 8.425 billion; up 5.7%.

Master Kong launched yet another new range of instant noodles in the summer of 2016; this time with a broader spectrum of dried vegetables and meats. These ‘healthier’ noodles are advertised using a famous actor.

We can also see an increase in regional variation in these production and sales statistics. The biggest decrease in output during the first half of 2014 was in Sichuan (-46.75%), and the largest increase in Guangxi (27.38). These figures are much higher than the slight decrease in the national output, so perhaps we are witnessing a regional shift in production, that is temporarily creating a downturn on the national level.

Chinese food scientists have also taken up the idea to enhance the nutritional image of instant noodles. One group is picking up the Chinese government’s idea to make potatoes the nation’s fourth staple foods and is developing a recipe and production process for instant noodles in which part of the wheat is replaced by potato. See my blog on potato processing for more details.

Baixiang Food Group (Zhengzhou, Henan) is developing more tasty products with better raw materials and production techniques. The company uses a special technique to freeze-dry noodles at -30 C to lock the nutrients in fresh noodles. When cooking, the noodles will be able to restore the original taste and texture after boiling. The company is increasing its investment in research and development by building more advanced labs, upgrading facilities, and attracting more talents. Baixiang has also established research institutes in South Korea and Japan.

Success by concentrating on a single segment

In 2024/25, Jinmailang reaped an enormous success, becoming the top selling branch in February 2025. This success was accomplished by the company’s new range of instant products specially designed for students. This included even the brand name:Xiaohui Banmian, ‘School Badge Noodles’.

A brand with a story: Nanjiecun

Wang Hongbin from Nanjie, a village in Henan province, was among the first in his village to travel overseas. In 1988, Wang, then in his 30s, had a chance to visit Japan, where he had his very first taste of instant noodles. A year after his return, a company in the nearby city of Pingdingshan bought two production lines for instant noodles, but their efforts to popularize the convenience food failed. Wang and some friends from Nanjie took over the factory and founded Nanjiecun Co. Targeting people in rural areas and students, the noodles were priced at RMB 0.5 per packet: cheap, but not very cheap in a country where many rural people still earned less than RMB 3 a day. Nevertheless, soon everyone was talking about Nanjie noodles. Nanjiecun’s star rose and the village was soon one of the wealthiest in the country. A full industrial cluster grew up around instant noodles, including print shops and seasoning and packaging factories. Production lines increased from two to 36. Annual capacity now can reach 120,000 packets per line. In 2017, the company sold noodles worth RMB 600 mln. About RMB 80 mln of that came from online sales. Nanjiecun has set up an R&D centre to develop new flavours. As the following picture shows, Nanjiecun is hooking on to the current craze for spicy food. Moreover, for those who can read Chinese: note that this flavour is linked to Beijing. The history of Yanjing Beer elsewhere in this blog shows that linking your product to the nation’s capital can be a winning strategy.

Food delivery offers more variety

The rise of food delivery has also played a role in the declining fortunes of the instant noodle industry. Food delivery gives consumers access to quick meals of more diversified tastes. Users of food delivery services reached 295 mln by the end of June 2017, a 41.6% increase from the end of 2016, according to the China Internet Network Information Center. Food delivery services have even reached high-speed trains (see the previous paragraphs). In mid-July 2017, 27 major railway stations across China launched a pilot on-demand food delivery service for high-speed trains passing through the stations.

Nissin severs ties with Jinmailang

Nissin has sold its interest in three joint-venture operations for RMB 450 mln to partner Jinmailang late 2015. Nissin said that in the future, the company would focus on expanding its business in China through local subsidiaries, without elaborating on exactly why the agreement had been ended. Insiders note that there is a growing preference for foreign brands of instant noodles, particularly in the larger cities such as Beijing and Shanghai, which bodes well for Nissin.

Africa the new frontier?

However, wouldn’t it be an interesting thought that some time in the near future, the consumption of instant noodles in the Western countries could be higher than in China?

Or will the Asian manufacturers succeed in reviving this product with more, and in particular healthier, formulations?

Anyway, I just (Aug. 27, 2014) read an interesting news item on a Chinese food industry site, with an even more intriguing title than the one this blog starts with: ‘Chinese instant noodles are attacking Coca Cola in Africa‘. It starts by reporting that a cup of instant noodles (see the above illustration) is already replacing the traditional corn porridge Kenkey as the typical breakfast in urban Ghana. The reporter then conjectures that Chinese instant noodles are pushing Coca Cola from its position as the leading foreign food and beverage product in that country. Food for thought indeed.

Export to . . . Chinese tourists

A report released jointly on Sept 28 by Alibaba’s Alitrip and Internet finance platform Wacai showed once and for all that Chinese tourists have a true, unswerving love for instant noodles. The report noted that up to 31.29% of Chinese tourists have packed instant noodles in their luggage when going abroad, and 58.24% have bought instant noodles after reaching their outbound destinations. The report shows that 66.14% of tourists born in 1970s pack instant noodles in their luggage, whereas the number is reduced to 53.82% for those born in the 1980s, and 50.96% for babies of the 1990s.

Still a newcomer

Early September 2014, Taiwan-based Wantwant Group suddenly announced that it intends to enter the instant noodle market. Wantwant is a major producer of candy, flavoured dairy beverages, snacks and other leisure food, but so far completely unfamiliar with instant noodles. The only link I can see so far is that the above mentioned top players also originate from Taiwan. Master Kong and Uni-president have not yet reacted to Wantwant’s announcement.

High end experiments

Uni-president attempted to open up a new market segment for its instant noodles by launching a line priced at RMB 30 per cup early 2016. The experiment failed utterly, and the products were recalled within a month after launch.

Flavour maker Haoji (Sichuan) has relaunched its non-fried instant noodles in November 2016. This instant noodle product — branded 99 Love, or phonetically “long-lasting love” in Chinese — is marketed as a healthy product that is made primarily from wheat, corn, buckwheat and potato sourced from high-altitude unpolluted areas; it is steamed, as opposed to fried, during the manufacturing process. An earlier launch failed, because Chinese consumers were apparently not ready for such an innovative product.

Instant relief

However, instant noodles have will remain to be the absolute favourite for one application: quick relief in times of disasters. When parts of China are shut off from the rest of the country due to floods or earthquakes, it is always possible to get a supply of light-weight instant noodles to the disaster area to prevent people from starving.

Instant noodles will remain an important pillar in the Chinese food industry, but it is a mature market and the main players will be fighting fiercely for a few percent for some time to come.

Instant noodle restaurants – are you serious?

Chinese are masters in turning anything around and market it as something completely new. One entrepreneur has played this trick on instant noodles and opened a restaurant annex convenience store chain named Nonoodle (bufangbianmian in Chinese). You can purchase a wide range of instant noodles there and a few other snacks and drinks, but you can also eat your instant noodles in the dining space. The English name Nonoodle is not a literal translation. In Chinese, instant noodles are called fangbianmian, ‘convenient noodles’. So, bufangbianmian literally means ‘inconvenient noodles’. The entrepreneur is suggesting that cooking water, soaking the noodles with the condiments in water, and wait until the noodles are more or less ready to eat is actually not that convenient. Why not let a ‘cook’ prepare the noodles of your choice for you. After the meal, you just go away, home or to another destination. The trick works, as long lines of young consumers can be seen at Nonoodles any time of the day. Amazing.

Corona virus facilitating the revival of instant noodles

When almost all urban Chinese were locked up inside their homes for a few weeks early 2020, it actually was a major boost for instant noodles. It is light, so easy to take home in large quantities. It is tasty and, in combination with some vegetables, chunks of meat, an egg, etc., can be a quite nutritious easy to prepare meal. However, the inventive Chinese invented a broad variety of dishes with instant noodles as the main ingredient. The following picture shows one example of such a novel dishe.

During and after COVID, noodle chains (not only instant) became a serious target for big investors. Once focused on high tech companies, venture-capital funds are pouring money into new noodle chain brands. Even tech giants like Tencent, the mother company of WeChat as well as an active investor, are doubling their bets on the sector. Chinese-style noodle chain restaurants first became tech investor darlings in 2021 when the industry faced tightened regulation while the country’s consumers became increasingly willing to spend more on quality products and experiences. There were twelve noodle chain investment deals in the first half of that year, with a combined total of RMB 1 billion injected into the emerging area.

Eurasia Consult’s database includes 342 producers of instant noodles.