The value of the 2025 Chinese market for energy drinks was RMB 139.8 billion; up 6.3%.

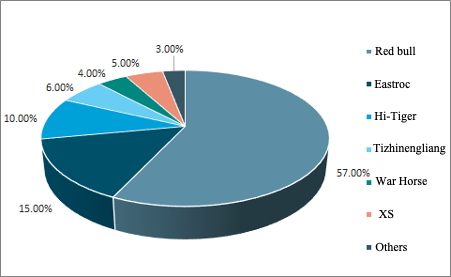

In view of the still strong influence of TCM on Chinese eating and drinking habits, China is a paradise for functional beverages. I already mentioned functional beverage in my general post on drinks, but the developments on the Chinese functional beverage scene have been so rapid lately, that it is time to dedicate a special post to this market. The interest in this type of drinks is not a surprise. TCM-based tonics have been an essential part of Chinese life almost since the beginning of Chinese culture. As has been introduced in the post on that topic, TCM has a much larger overlap with food than Western medicine. A core term in TCM is bu‘to supplement’. Most Chinese herbal medicines are in fact supplements, helping the human body to regain balance. The following pie graph shows the market shares of the main brands in 2019.

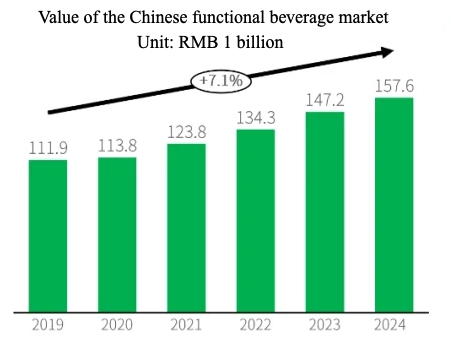

The following table shows the development of the market value in the period 2019 – 2014.

Wanglaoji

The very first functional beverage, obviously based on TCM, in China probably is Wanglaoji, also known by its Cantonese pronunciation: Wong lo kat. Wanglaoji is said to be a product that was invented by Wang Zebang (nicknamed Wang Ji ) from Heshan in Guangdong province in 1828. It withstood the turbulent modern history of China from the fall of the Qing Dynasty, the civil wars and the war with Japan and the foundation of the PRC and is currently sold as a herbal tea, with the ingredients being seven different kinds of Chinese herbal plants.

Water, sugar, mesona, dan hua (Apocynaceae species), Bu zha ye (Microcos paniculata Linn), chrysanthemum flowers, jin yin hua (Lonicera japonica Thunb.), Prunella vulgaris, and licorice.

Although these are all medicinal herbs, Wanglaoji is basically consumed as a soothing drink, not for curing a particular ailment. However, due to the high sugar content, it does provide quite a lot of energy. One sip a few years ago was enough for me. Wanglaoji has become extremely popular during the early 21stcentury, but has been plagued by a trademark dispute between the state owned Guandong-based producer and a Hong Kong-based company set up by a descendant of Wang Zebang who moved to Hong Kong after the founding of the PRC.

Red Bull

When Wanglaoji was gaining popularity, Red Bull had already been introduced in 1995. Red Bull China is marketed by the Reignwood Group, which also markets another energy drink: War Horse, together with Voss mineral water from Norway, Vita Coco, a coconut drink and Capri Sun fruit juice beverages. Reignwood got in conflict with Red Bull’s Thai-based creator TC Pharmaceutical Industries in the course of 2019 in which the latter tried to stop the cooperation with Reignwood. TCPI started a law suit in Beijing, but lost early 2020. Red Bull, this foreign, though also Asian, energy drink was welcomed by many, but also greeted with suspicion by the authorities. Red Bull was ordered to indicate on its cans that the wonder liquid was ‘not suitable for young children and pregnant women’. Reignwood opened China’s (and possibly the world’s) first functional beverage museum in its own Reignwood Centre in Beijing in August 2020.

Until that time, the only indigenous drink resembling a modern functional beverage was Jianlibao, an electrolyte drink launched in 1984, when it was made the official beverage of the Chinese participants of the LA Olympics.

It was a best-selling drink through the 1990s, but has since then suffered from mismanagement. Recently, Red Bull China has also become troubled by quarrels among its investors. You can read all about that on the Net. This strife seems to be a common ill of Wanglaoji, Jianlibao and Red Bull. Perhaps the managers involved are drinking too much of their own beverages. Still, Red Bull alone generated a turnover exceeding RMB 20 billion in 2018 in a market whose value is estimated at RMB 50 billion by insiders, making Red Bull still China’s number one functional beverage, by far.

With the growing spending power, combined with an increased interest in health and wellness, of Chinese consumers, several new functional drinks have been launched during the past 2 – 3 years: sport drinks, vitamin drinks, energy drinks, you name it. Not all of these new beverages have been able to reach a critical mass, but some of them seem to be there to stay, at least for a while. In this post, I will introduce a two more that seem to have good prospects.

Hi-Tiger

Dali Food Group has been mentioned in several earlier posts in this blog, but always for its bakery products: bread and biscuits. However, Dali is also the producer of Hi-Tiger energy drink. One look at the ad is sufficient to see that not much R&D had to spent on developing this product. The ingredients list confirms this impression.

Dali advertises heavily and is producing the drink various local plants to ensure a continuous supply. The brand sponsors the China Basketball Association.

Eastroc

Eastroc Beverages was established in Shenzhen, Guangdong, in 1987, as a state owned enterprise. It was privatised in 2003 as the Eastroc Group. It launched its energy drink in 1998 and once more the design of the bottle resembles that of Red Bull. The ingredients list is also getting a little boring.

Eastroc sponsored the Portuguese football team during the World Cup in Russia in 2018. It is also the Official Supplier of the 2018/2019 Chinese Super League (CSL). In the first three quarters of 2024, Eastroc’s operating revenue surged to RMB 12.56 billion, up 45.34%. By the end of the third quarter of 2024, Eastroc had built a nationwide sales network with 2,982 dealer partners and 3.6 million active retail outlets, reaching over 210 million consumers. The company’s direct sales channels (online and offline) grew 69.87 percent year-on-year.

These are the top energy drinks in China at the moment. The most salient feature of this market is that it is on one hand huge and on the other hand extremely boring, with the numbers two and three doing the utmost to imitate the leader. This leaves lucrative opportunities for the a genuinely innovative product; I would say: one based on TCM, or perhaps herbal traditions from other parts of the globe?

The other side: drinks that help you sleep

Amidst this fierce battle between older and newer suppliers of energy drinks, candy maker Want Want launched its Dream Dream Water (Mengmengshui) in 2019. It is a herbal tea that claims to make you sleep better. Its main ingredients in GABA, that is sometimes taken for relieving anxiety and improving mood. The market, professionals and consumers have received the drink with mixed feelings. As soon as I have an opportunity to try it, I will add my personal comments here.

New Hope Dairy has launched a milk drink fortified with casein peptides that induces sleep even better than your regular bed time glass of milk. It is marketed as Shuo Wan’an ‘Say Good night’.

From extremely popular to off the shelves – fruit jelly flirting with consumers to recoup their market

People with experience in Asia probably know the stuff: brightly coloured fruit flavoured jelly in small plastic cups. Chinese women, as well as their sisters from many other East Asian nations, cannot get enough of fruit jellies. You rip off the sealing foil and suck the entire jelly into your mouth. There, it will start melting instantly and you can enjoy (if fruit jelly is your thing) the feeling as if you have just taken a huge sip of fruit juice. The effect is partly caused by a mixture of texturisers, flavours and colourants, but who cares. Well, parents did, when a few children almost choked to death on the things.

You need to be careful when giving them to younger children. Even though they melt quickly in the oral cavity, if you suck with so much enthusiasm that the thing ends up in your windpipe, you are in trouble. A number of such incidents happened and Chinese retailers reacted in a very Chinese way: they took all fruit jellies from the shelves. That radical measure will certainly protect the children, but is a big blow to the producers. And the market is huge. It has grown into an RMB 25 billion industry, with about 300 serious manufacturers in China alone. They want their market back and who would dare to blame them.

The original thing

Before I look at how some manufacturers are trying to win back the market, let’s have a look at the original standard fruit jelly. The main ingredients of fruit jelly are:

fruit juice, carrageenan, konjac sodium alginate, water and sugar.

Production is relatively easy. Just mix the ingredients, fill it into the cups, close the cups, refrigerate to set and you can package and dispatch them.

Fruit jelly is obviously not a very nutritious food. However, it is still better than the average candy. It does not contain much fat and some of the texturisers used are dietary fibre that helps the bowel function.

Insiders distinguish four types of fruit jelly producers.

The big players for whom fruit jelly is their core product; like market leader Xizhilang (22.1% market share in 2019);

Candy makers that also produce fruit jelly; like Hsufuchi (introduced in another post in this blog about biscuits; 2.8% market share) or Want Want (introduced in various posts about beverages; 5.5% market share);

Specialist food companies for which fruit jelly fits in the product line; like pudding maker Qiaomama (Clever Mummy) that specialises in pudding for children (see the Trends page of this blog).

Local companies supplying their own regional market.

Innovation

Taiwan-based manufacturer of leisure food Want Want seems to be leading these efforts by launching a number of varieties that call for a slightly different way of consuming fruit jellies, thus reducing the risk of choking.

Soft pudding

Soft puddings do not contain trans-fat and have a protein content of more than 1.1 g/100g. They are chewier than the traditional fruit jellies and therefore invite to bite and chew on, rather than sucking them in at once.

Weiduoli

Li means ‘pellet’ and refers to the small chunks of fruit in the jelly. Want Want claims that Weiduoli contains at least 5% of fruit. However, the most innovative aspect of Weiduoli is that it comes in a soft bottle, so you can suck it in small sips, rather than swallowing an entire piece of fruit jelly.

Fruit flesh jelly

This is fruit jelly with a 20% – 25% fruit content. It is more like pieces of fruit held together by jelly. This as well invites to consume it by biting off small pieces and properly chew it. It also has more dietary fibre than the classic jellies, obviously. And if you are lucky, you may even hit some remaining traces of vitamins and minerals.

Yaogundong (Rock ‘n Roll Jelly)

Low calorie

Qinqin Food (Fujian) launched a new type of low calorie konjac fruit jelly in cooperation with Orihiro from Japan in July 2020. An interesting feature of the ad is that it does not use children, but a young adult male to promote these products. This could be a subtle attempt to reposition fruit jelly.

I’m sure that most readers love this variety even before trying it. This product is sold in a cup resembling that used to sell ice cream. The cup contains a few jellies in the traditional packing and a layer of fruit flavoured powder. According to an advertising video that is entertaining even for readers who cannot understand the Chinese, you can consume these jellies in three ways:

eat the jellies in the traditional way;

take them out, roll them through the powder and eat them;

Wet your finger, dip it in the powder and eat the powder;

This is a clever move. Children will be tempted to go for the second way, which will slow down their moves and diminish the risk of choking to a minimum. However, I wonder if this variety will survive. I will keep you posted.

With so much innovative energy from the competition, market leader Xizhilang is also introducing a floral type of fruit jelly to re-interest its patrons in their products. Perhaps this more elegant fancy look will make consumers less eager to suck the jelly up at once.

Healthier

Chinese manufacturers of fruit jelly are also trying to revive the product by designing healthier types. They experiment with adding more fresh fruit and vegetable juice, adding tradtional Chinese medicinal (TCM) herbs, tea extracts, etc. Using healthier types of thickeners, like konjac or xanthan, is also part of this research.

The oldest Chinese carbonated beverages dates from 1874

Soft drinks is undoubtedly a Western concept. However, the history of domestic carbonated beverage in China is longer than many people may believe. The most famous soda beverages launched before 1949 are:

Most of the HQ locations were cities with considerable numbers of foreign expats.

The Chinese typology of foods and beverages is one of the recurrent themes in this blog. The typical way in which such products are divided in categories in a certain region provides an interesting look on the influence of the local culture on eating and drinking.

This post will continue with this topic with the typology of beverages. This typology has even been officially laid down in a State Standard (GB), GB10789 to be precise. It discerns the following types.

Carbonated drinks

These are relatively new in China and still strongly connected to the Western lifestyle. China’s oldest carbonated drink: Beibingyang (Northern Ice Sea) has been revived recently, which I have introduced in a separate post on the reappearance of old brands.

Protein beverages

Although not a Chinese invention, this category is much more popular in China than elsewhere in the world. They have also been introduced separately in a previous post. Protein beverages are relatively viscous liquids made from various nuts or beans, or milk, or a combination. A number of them include probiotic cultures.

Bottled water

Paying a lot of money for something that you can get from your tap for a much lower price has also taken on in China. China’s bottled water market is expected to reach 490 mln hls of total annual consumption by 2020. The retail value of bottled water in China for 2019 is estimated at RMB 346.2 billion. Apart from the large number of branded water, new mineral water brands keep appearing in China. Many are profiling themselves with the location of their source. The trend of 2015, e.g., in this category was mineral water from Tibet.

Some statistics of the past 5 years

Year

Volume(hls)

Increase(%)

2015

841,016,000

7.60

2014

781,614,000

9.37

2013

665,114,000

13.01

2012

556,278,000

19.20

2011

178,900,000

23.67

Top brands

The following table shows the market shares of major brands in 2017

Brand

Share (%)

Nongfu Spring

8.5

C’est Bon

8.0

Evian

5.0

Chef Kong

4.8

Ganten

4.6

Wahaha

4.5

Coca Cola

4.0

Others

60.7

A new variety was added to the category of bottled water by Nongfu Spring in February 2022: bottled boild water (baikaishui). This type is inspired by traditional Chinese medicine. TCM attributes many healing and nutritional functions to water that has been brought to the boil and then cooled to drinking temperature.

China’s once largest mineral water brand, Laoshan, came back in 2025 with a mineral water enriched with snake grass. Snake Grass, also known as Clinacanthus nutans, is a plant ascribed various medicinal benefits, like anti-inflammatory, anti-diabetic, anti-cancer, and antioxidant properties.

Tea beverages

Tea is China’s national drink, but still, tea beverages have been introduced from overseas. When foreign ice teas were launched in China, many beverage makers tried to concoct their own versions. Tea beverages with various fruit flavours appeared one after another.

Milk tea

A rapidly growing subcategory are the milk teas, based on traditional milk or butter teas drunk by Mongolians and Tibetans.

The pictures shows the Sizhou brand milk tea, with the following ingredients:

In the course of 2018, China’s tea aficionados have embraced a new trend, one that is encapsulated in the growing popularity of the milk tea brand, Hey Tea. Originally sold in a tiny alleyway in Jiangmen, southern China’s Guangdong province, the brand went viral on social media because of its signature “cheese” series — a cup of hot tea topped with light cheesecake mix. Since then, Hey Tea has developed into a franchise with more than 80 outlets in 13 cities across the country. In large urban centres such as Shanghai and Beijing, customers routinely wait for hours to get their hands on a cup of cheese tea. Hey Tea’s cheese-inspired beverages are just variations of the same milk-topped teas available at many urban teashops in China. Fresh milk, skimmed milk, and cream cheese are blended and poured on top of iced tea to create a layer of creamy froth about 3cm thick.

Milk tea is becoming such a huge market that ingredients suppliers have started to prioritise it in their R&D. FrieslandCampina Kievit, e.g., is conducting research to develop the optimum dairy ingredients for Chinese milk tea. Aspects considered include: tea type, milkiness, sweetness and mouthfeel.

A new development in the Chinese tea beverage market is mixed tea drinks. Representative brands are: Teaka (tea + coffee), Chef Kong’s tea + milk, Cha pi (tea + fruit juice) and Hongchajun (tea + probiotics).

Multinationals like Coca Cola cannot afford to miss out on the popularity of tea beverages in China. The company has launched a range of tea drinks branded Chunchashe ‘Genuine Tea House’. It is marketed as not containing sugar, but still leaving a sweet aftertaste. It comes in green, black and Wulong flavours.

Herbal tea

Traditional Chinese Medicine (TCM) is making an effort to cash in on the increasing interest in health foods among Chinese consumers, as has been introduced in earlier posts. The market value was estimated at more than RMB 40 billion late 2015 and is expected to grow to close to RMB 20 billion in 2020.. A very prominent application of medicinal herbs as food ingredients are the herbal teas that have become popular during the past few years. The first and most popular, Wanglaoji, is still based on a traditional recipe. Later herbal teas are marketed as modern health or functional beverages, comparing and competing with Western drinks like Red Bull. A very recently launched product in this category is Good Night (Wan An), produced by Wan’an Technology Co., Ltd. (Beijing). Ingredients are said to include:

natural GABA, theanine, chamomile and spina date seed

Wanglaoji launched its own cola drink, Wanglaoji Cola, in January 2018. The company promoted it during the Davos Summit.

The value of the Chinese tea beverage market in 2020 exceeded RMB 100 billion.

Coffee beverages

Coffee being such a recent arrival in China, so closely linked to a Western lifestyle, it seems odd to find it as an officially sanctioned subcategory of beverages. However, they have become quite popular. Perhaps they are easier on the Chinese palate than the basic black brew. The have been introduced in this blog before, in a separate post.

Plant beverages

This category includes drinks made from the juice of vegetables and fruits, in various degrees of concentration. Cereal based drinks are also included. A subtype that is especially popular in China is called ‘fruit tea’ (guocha) in Chinese. The best English translation would be ‘nectar’. The are relatively viscous drinks with carrot or hawthorn pulp as the main ingredient.

In 2016, China’s fruit juice retail volume was 134.47 mln hls and retail sales reached RMB 100.914 billion, up 1.88%. Main brands in the Chinese fruit juice market include Uni-President, Chef Kong, Nongfu Spring, and Huiyuan. China’s top producer in this category is Huiyuan Fruit Juice (Beijing). The company was once an acquisition target of Coca Cola, but the deal was vetoed by the Chinese cartel watchdog. Huiyuan recently launched a range of juices in Malaysia under the Yami brand.

The latest addition to the fruit nectars is Zaoshanzha, a drink made from dates and hawthorn by Haoxiangni.

In terms of taste, orange juice is still the largest category of the fruit juice market in China, There are some differences in taste between the north and the south in China. Apple, peach and pear consumption is relatively high in the north market. Pure juice (‘not from concentrate’) is the growth point in this industry. Chinese women have greater demand for juice, which is related to the pursuit of a healthy figure.

Another popular new subtype is formed by the fruit vinegars. These beverages have become in vogue in the years 2015 – 2016 as health products that help burn fat. In the early stage, it looked as if they would become a success, cashing in on the general trend towards more healthy food in China. However, the tide seemed to turn mid 2018, when a prominent brand, Tiandi Nr. 1 (Tiandi Yihao)’s semi-annual report showed a turnover almost half that of the same period of the previous year.

Flavoured beverages

The literal translation of the Chinese definition of this category is: drinks made by combining food flavours, sugar or sweeteners, or acidifiers. We probably could also refer to these as: designer beverages. It is not always easy to distinguish these from other categories. If you boil tea leaves and the add other flavouring ingredients to the filtered liquid, you would have a tea beverage. However, a drink whose ingredients list includes tea extract, would count as a flavoured beverage.

Nutritious beverages

These include sports drinks and other functional beverages. This category started to boom in the course of 2016. As a result, Red Bull is confronted with an ever growing number of domestic competitors in China. One of the frist challengers (August 2016) was a vitamin drink by Want Want, presented in a gold-coloured can.

This product category is getting so popular, that a dairy company like Yili launched an energy drink of its own in April 2018: Huanxingyuan.

Solid beverages

These are sold in powdered from and infused before consumption. There is at least one traditional Chinese drink typically sold as such: suanmeitang or sour plum drink (literally: soup). A more recent, but still traditional, product is instant soy milk. Many members of the other categories are now also available in powdered form.

The picture shows Yiben brand suanmeitang, which contains the following ingredients:

Senke Beverages has launched an innovative type of suanmeitang adding traditional Chinese medicinal herbs, marketed as ‘Lotus Leaf Suanmeitang‘, in the summer of 2018. Apart from quenching thirst, it is said to lower cholesterol and have a certain slimming effect.

Daring launches – low survival

Chinese beverage makers are quite daring in launching newly developed products on the market, where Western multinationals would organise more pilots to test the products’ reception by consumers. However, a recent survey by the China Food Industry Association reveals that only 5% of newly launched Chinese beverages survive. I guess that is test marketing the Chinese way.

How do Westerners appreciate this?

Are you getting bored with my academic stories? No problem, you can now relax watching this home brew video in which a Western lady living in China introduces here own favourite Chinese beverages.

Here is another Top 5, but then of the most bizarre Chinese drinks.

Latest trend: odd flavours

The structure of the Chinese soft drinks market is undergoing rapid changes. Consumers are developing an awareness of personality, paying more attention to individual needs and preferences. This has created a market for what Chinese have started to call ‘odd flavour water (guaiweishui)’. Laoshan, China’s first and for a long time only producer of mineral water, has launched Baishecaoshui (literally: white snake grass water). It is based on Baishecao (oldenlandia). Hey Song Sarsaparilla from Taiwan is also gaining popularity. The current top producer of mineral water, Nongfu Spring (see above), has also launched odd flavour drinks: Oriental Leaves (Dongfang Shuye), which does not contain herbal extracts, but a mix of flavourings and nutrients, and Red Pointed Leaves (Hongse Jianye), which contains extracts from American Ginseng, green tea and bamboo. This market is extremely volatile. The survival rate of new drinks is generally about 10%, and is now dropping to 5%, according to recent market studies. These products are catering to the young and young Chinese consumers have a low brand loyalty where food and drinks are concerned.

Coffee has been reported on before in my post on Pu’er. People have been talking about the Chinese market for ready to drink coffee a lot since then. Apparently it is a topic that is on people’s minds, so I have bundled their remarks in this dedicated post.

Coffee vs tea beverages

The following table shows the turnover of tea beverages and coffee beverages in China in the period 2019 – 2024, also indicating the ratio between the two. It is clear that coffee is slowly but definitely winning this battle. However, these data also show that the total market of ready-to-drink tea and coffee is growing steadily.

An emerging coffee nation

China is gradually emerging as a coffee producing nation. The country’s current annual production is approximately 100,000 mt, 98% of which takes place in Yunnan, the home province of Pu’er, and the remaining the island province of Hainan.

By the end of 2010, China had 135 coffee processing companies, the geographic distribution of which is can be found in the following table.

Region

companies

Shanghai

37

Guangdong

26

Yunnan

18

Beijing

17

Hainan

11

Other

26

This shows that the processing still mainly takes place in the most developed regions and not in the locations where the coffee is grown. However, the Pu’er post shows that the main multinational players have set up shop in Yunnan.

The Chinese have never acquired a habit of brewing coffee at home, which creates a fertile ground for two types of products: coffee shops where you can enjoy your favourite brew (see my post on that market), and Ready To Drink (RTD) coffee products, introduced in this post.

Applying the Chinese instant tea model to instant coffee

Between 2008 and 2013, instant tea has been the driving force in the Chinese tea market, increasing sales by USD 1.7 billion. To date, the popularity of instant tea is almost entirely a Chinese phenomenon, as China accounted for 92% of Asia-Pacific’s instant tea sales in 2013. Instant coffee on the other hand, is immensely popular throughout the region, with China accounting for just 15% of the overall market in 2013. As instant coffee shares many of the attributes that have driven the success of instant tea in China, namely the replication of foodservice options, flavour malleability, convenience, and a young consumer base, applying the innovative packaging of instant tea to coffee may spell further success for Asia’s already booming instant coffee market.

Instant tea in China is composed almost entirely of instant ‘milk teas’ that aim to replicate the sweet flavours of popular street stall/kiosk and café operators like Happy Lemon, Jack Hut, and ChaTime. Popular flavours include red bean and jasmine green, while some also include bobas (tapioca pearls found in bubble tea) for added texture. To make the beverage accessible through retail channels, manufacturers use single-serve packaging of on-the-go paper cups filled with a sealed pouch of instant tea and a straw.

The sweet flavour profile of these milk teas, and economical price tag compared to their on-trade equivalents, makes them particularly popular with younger Chinese consumers. The accessible format and price of instant tea enables young consumers to partake, albeit indirectly, in fashionable foodservice.

Aware of the influence of younger demographics, Chinese manufacturers including the Guangdong Strong and Zhejiang Xiangpiaopiao (2023 turnover: RMB 362.5 billion) are deliberate in their marketing, positioning the products specifically to Chinese youth, through fun packaging, and celebrity endorsements. Xiangpiaopiao is awaiting approval for its IPO before the end of 2015.

Is China the future for instant coffee?

In the past decade, the instant coffee market has actually expanded at rates of 7 to 10% a year, according to the Global Coffee Report; the International Coffee Organization projects a 4% global volume growth between 2012 and 2017.

The country that historically drank about two cups of coffee per year per person is now the fourth-largest global market for ready to drink coffee in terms of volume. The reason? Convenience. A 2012 poll found that 70% of Chinese workers said they were overworked and more than 40% stated they had less leisure time than previous years. Plus, most new buyers are used to boiling water to make tea, often owning just a teapot and not the appliances needed to make a fresh pot of coffee. By 2017, the Chinese RTD coffee market is projected to increase by 129% in volume. A recent study estimates that the value of the Chinese RTD coffee market will be RMB 18.6 bln by 2020.

Like many food innovations, the origin of instant coffee has several claimants.

Instant coffee is tapping into a new market: tea drinkers. As of 2013 in Great Britain, tea bag sales dropped 17.3% while sales of Nescafé instant coffee went up in supermarkets by more than 6.3%. The country known for it’s tea and crumpets may be making a similar transition to China’s tea-drinking population.

Nestlé SA led the Chinese market with 70.8% share in 2017, followed by Suntory at 4.9%, Uni-President at 3.3%, and Starbucks at 3.1%. Coca-Cola re-entered the category with its Georgia brand. Its marketing has improved the brand image and the product’s visibility. Nestlé’s Nescafé, a strong category leader, hired Chinese actress Angela baby for TV advertisements, which boosted sales. Starbucks and Ting Hsin (PepsiCo’s local distributor and bottler) agreed to jointly produce and distribute RTD coffee. Suntory and Huiyuan also set up a joint venture to market RTD coffee and RTD tea. In 2015, Hui Yuan was the largest local player in off-trade volume sales terms.

In terms of flavor, the most popular one is latte, accounting for over 54% of off-trade volume sales in 2015.

Coffee as ingredient

Europeans still mainly think of coffee as a beverage made by infusing ground coffee beans with boiling water. The real coffee lovers drink it black, hot and bitter. Those who find that a little too intimidating can dilute it with milk. As most Chinese still have a problem with pure coffee, even with the heavily diluted americanos served by Starbucks or Costa Coffee, a number of coffee flavoured beverages have appeared on the Chinese market. The most recent one Maoyuan Coffee by Wahaha (Hangzhou, Zhejiang).

Multinationals follow suit

A recent development in this market is a strategic alliance between Starbucks and Tingyi. Tingyi, a leading food and beverage producer, has signed an agreement with Starbucks to manufacture and distribute the latter’s RTD products on the Chinese mainland. Tingyi is a well-known supplier of instant noodles and biscuits. According to the agreement, Starbucks will help Tingyi, which makes the well-known Master Kong brand of instant noodles, with coffee expertise, brand development and future product innovation. Tingyi will manufacture and sell the Starbucks RTD portfolio in China, said a statement from Starbucks.

But it will take a lot more than a fancy Starbucks product to convince Americans to drink products like this one sold in China: Nestlé’s instant coffee with jelly.

A multinational like Coca Cola cannot afford to miss out on the popularity of tea beverages in China. The company is marketing its RTD coffee brand Georgia in China.

Taiwan-based manufacturer of snack food, Want Want, had already started looking for divesting opportunities in the beverage industry, when it launched its own RTD coffee brand ‘Mr. Bond’ in 2018. When I am writing this (June 2018), it is still too early to judge the success of this product.

Costa has to follow suit

Costa Coffee could not afford to neglect this market and launched a range of ready-to-drink coffee beverages in China late March 2020.

Jingdong Top 5

China’s leading online store Jingdong keeps track of the top selling brands of any product type the platform has on offer. The following list are the 5 best selling ready to drink coffee brands in 2020

Three of the top 5 are international brands, which indicates that it still is a relatively foreign product group. Nongfu Spring is China’s top bottled water brand, but has been expanding to other types of beverage in recent years. Nongfu launched a new type of RTD coffee, branded Yirgacheffee (Tanbing) in 2022 (see the next photo). Chef Kong is the leading instant noodle brand, but has also diversified into beverages a few years ago.

The value of the 2025 Chinese instant noodle market was RMB 123.68 billion; up from RMB 103.9 billion in 2018.

Instant noodles: winners in corona time

In the present times, when governments, companies and people around the globe are bearish about the economy, employment and even the timely supply of food, there are also winners. One big winner in China is the instant noodle. After this special corona vignette, you can read the regular post, which starts with the information that the Chinese instant noodle consumption has started rising again with a few percent annually, after a period of decline. That decline followed a much longer period of spectacular growth. Chinese consumers seem literally fed up with instant noodles and were eagerly looking for a larger variety of instant foods. The manufacturers fought back bravely, launching new types of instant noodles with a broader spectrum of flavours and more and fresher ingredients. Read the details below.

Then came the corona virus, changing the ways Chinese bought and consumed food. This gave an enormous boost to instant noodles. Check out the increase of the sales figures of the first 2 months of 2020 of the top producers, compared to the sales in the same period of 2019.

Company

Increase (%)

Uni-President

297.14

Jinmailang

180.00

Chef Kong

150.54

China has produced 2,246,998.4 mt of instant noodles in the first 5 months of 2020; Henan was the largest region good for 19.54%.

The industry is eagerly taking this opportunity up and is now advertising its modernized types of noodles. I am selecting a few of the most representative aspects.

Great taste

Imperial quality

Broad range of flavours

The regular blog text

One of the most intriguing headlines I read in the Chinese food industry media when I started this blog is in the shape of a question: ‘have instant noodles past their peak?‘ The national output of instant noodles in 2014 was 10,256,640 mt, down 1.55% compared to 2013. Total sales of instant noodles in 2015 decreased with 6.3% and the turnover with 2.6%. The market saw an increase of 0.9% in 2016, positive for the first time since several years. The volume of 2017 increased with an additional 2.8%, but plummeted again in 2018. The value of the market was worth RMB 143.546 billion in the first half of 2019; up 7.75% again. The leading companies filed increasing turnovers for again for 2018 (see below). The market is extremely volatile, but there is a trend towards sanitation, in which the top players grow, while smaller companies disappear.

According to a survey conducted mid 2017, the largest market segment are consumer of the age group 23 – 28, followed by the section 29 – 35. In both groups, women consume significantly more than men.

The following table shows the development of the Chinese instant noodle output from 2010 thru 2018.

Year

volume (mt)

2010

6,881,100

2011

8,275,900

2012

9,467,400

2013

10,307,600

2014

10,256,640

2015

10,178,000

2016

11,039,000

2017

11,032,000

2018

6,695,000

China has produced 5.13 mln mt of instant noodles in 2021; down 6.8%.

The market has been dominated by 4 main players for many years. The following tables shows their market shares from 2005 to 2017. An interesting detail is that the first 2 are Taiwan-based.

Whether instant noodles are on retreat is indeed a bold question. If there is one Chinese food product that has seemingly conquered the world in the sense that it is known and available in supermarkets on all continents it is instant noodles.

Yes, soy sauce was know in most Western countries long before the first pack of instant noodles appeared on the shelves of our supermarkets and yes, instant noodles are probably a Japanese invention. However, it was that huge neighbour of Japan that posed the single largest market for this convenience food and it was through the Chinese diaspora that it ended up in supermarkets in regions like Europe, North America, or Australia. The products on offer in Western shops are not only imported from Asia, but also partly produced by Western companies like Unilever’s Unox brand.

One theory says that the rise of instant noodles was partly caused by the mass movement of surplus rural labour to the Chinese cities. Instant noodles became the favourite food of the migrant workers. It was cheap, tasty and easy to prepare. Migrants have now accumulated enough wealth to move on to more healthy foods, causing a drop in instant noodle sales.

Another surprising factor influencing the decrease of instant noodle consumption in China is booming development of the high speed rail network. In a special post on train food in China, I have reported that railroad stations are important points of sales for instant noodles. However, with the shortening of the time between any two cities, the demand for instant noodles decreases proportionally. This comes on top of the rise in living standard, which makes Chinese rail travellers buy more fancy lunch boxes, on the expense of cheaper instant foods.

Market not endless

The market for instant noodles in China seemed to be growing endlessly. From a convenience snack it has become a regular meal for many white-collar workers. The growing spending power in the Chinese created an ever-larger number of new adaptors for this food. The following video gives an impression about the an instant noodles production line.

What we could notice during the past few years was that the manufacturers of instant noodles had to go into ever-larger lengths to create new flavours and textures, new additions like dried pieces of meat that could be rehydrated like the dried vegetables that were a more traditional ingredient of instant noodles. With hindsight, this can be regarded as a sign that the consumers were getting a little bored and needed to be stimulated again.

Against the background of the many food scandals of recent years, Chinese consumers have grown more conscious of food safety and healthy food in general. While instant noodles are not unhealthy, it is surely not healthy food. Major players are noticing that the need to rid their product of the ‘junk food’ image.

All top manufacturers have already switched from fried to boiled instant noodles, reducing the fat content, which also decreases the need for antioxidants.

Another recent trend is that several producers of instant noodles, even market leader Master Kong, have started diversifying, adding soft drinks or other foods (like biscuits) and beverages to their product range. Their strategists may have read the signs on the wall.

Master Kong, a brand of Taiwan-based Tingyi, is the absolute leader in this market. In 2013, the company operated 23% of all instant noodle production lines in China, was good for 46.6% of the national turnover of the industry and produced 34.5% of the national volume. Moreover, Master Kong was the fastest selling Chinese brand in 2013, for the second time in row. 91.4% of the respondents in the survey had been in contact with the brand. That even this company has stopped placing all its eggs in the instant noodle basket is telling. Tingyi is reporting a serious drop in net profit in 2014. The net profit of the 3rd quarter of 2014 was 13.85% lower than in the same period of 2013.

Tingyi, the owner of the Master Kong brand makes half the instant noodles eaten annually in China, yet revenue is stagnating as middle-class consumers abandon the salty, fatty cups for healthier options. Tingyi is on a mission to reinvent the humble noodle, pouring millions of dollars into customer education, food science, Olympic Games sponsorships and “Kung Fu Panda” movie shorts to convince diners the cheap meal can be part of their gastronomic aspirations. “We want to continue to grow up, and ‘premium up,’ with our Chinese consumers,” Richard Chen, Tingyi’s chief technology officer, said at the company’s Shanghai research centre. “In a couple of years, we will be able to reach the gold standard, which is when you can’t tell our noodles apart from what you would get in a noodle shop.”

The latest innovative move of Master Kong to keep its leading position is launching two sister varieties based on Western flavours: black and white pepper steak.

Innovators at Tingyi once focused on practical advancements such as foldable forks and double-layer packaging so working-class Chinese could wolf down noodles on their commutes. Now, they work out of an RMB 500 mln research complex in Shanghai, with Tingyi tapping the nation’s top food-science university programs and partnering with Japanese companies such as Itochu Corp. to develop chemical-free flavorings and palm oil-free noodles. Master Kong’s turnover of 2018 was RMB 60.686 billion; up 2.94%. Its turnover for instant noodles was RMB 23.917 billion; up 5.73%.

Master Kong launched a range of power bars, marketed as breakfast replacers early 2020.

The company also divested into various beverages. Master Kong’s turnover in the first half of 2020 was RMB 32.934 billion; but only RMB 14.910 was derived from instant noodles.

Master Kong’s main competitor is another Taiwanese company: Uni-President. While Master Kong is still the leader, it is struggling with decreasing sales (-1.51% in the first half of 2014), while Uni-President is still showing, low, increasing sales (1.3%).

There could be some truth in the predictions of the author of the above-mentioned article. We need to wait and see how this market develops. For the time being it remains huge. UniPresidents’s turnover in China of 2018 was RMB 21.772 billion; up 4.6%. Its turnover for instant noodles was RMB 8.425 billion; up 5.7%.

Master Kong launched yet another new range of instant noodles in the summer of 2016; this time with a broader spectrum of dried vegetables and meats. These ‘healthier’ noodles are advertised using a famous actor.

We can also see an increase in regional variation in these production and sales statistics. The biggest decrease in output during the first half of 2014 was in Sichuan (-46.75%), and the largest increase in Guangxi (27.38). These figures are much higher than the slight decrease in the national output, so perhaps we are witnessing a regional shift in production, that is temporarily creating a downturn on the national level.

Chinese food scientists have also taken up the idea to enhance the nutritional image of instant noodles. One group is picking up the Chinese government’s idea to make potatoes the nation’s fourth staple foods and is developing a recipe and production process for instant noodles in which part of the wheat is replaced by potato. See my blog on potato processing for more details.

Baixiang Food Group (Zhengzhou, Henan) is developing more tasty products with better raw materials and production techniques. The company uses a special technique to freeze-dry noodles at -30 C to lock the nutrients in fresh noodles. When cooking, the noodles will be able to restore the original taste and texture after boiling. The company is increasing its investment in research and development by building more advanced labs, upgrading facilities, and attracting more talents. Baixiang has also established research institutes in South Korea and Japan.

Success by concentrating on a single segment

In 2024/25, Jinmailang reaped an enormous success, becoming the top selling branch in February 2025. This success was accomplished by the company’s new range of instant products specially designed for students. This included even the brand name:Xiaohui Banmian, ‘School Badge Noodles’.

A brand with a story: Nanjiecun

Wang Hongbin from Nanjie, a village in Henan province, was among the first in his village to travel overseas. In 1988, Wang, then in his 30s, had a chance to visit Japan, where he had his very first taste of instant noodles. A year after his return, a company in the nearby city of Pingdingshan bought two production lines for instant noodles, but their efforts to popularize the convenience food failed. Wang and some friends from Nanjie took over the factory and founded Nanjiecun Co. Targeting people in rural areas and students, the noodles were priced at RMB 0.5 per packet: cheap, but not very cheap in a country where many rural people still earned less than RMB 3 a day. Nevertheless, soon everyone was talking about Nanjie noodles. Nanjiecun’s star rose and the village was soon one of the wealthiest in the country. A full industrial cluster grew up around instant noodles, including print shops and seasoning and packaging factories. Production lines increased from two to 36. Annual capacity now can reach 120,000 packets per line. In 2017, the company sold noodles worth RMB 600 mln. About RMB 80 mln of that came from online sales. Nanjiecun has set up an R&D centre to develop new flavours. As the following picture shows, Nanjiecun is hooking on to the current craze for spicy food. Moreover, for those who can read Chinese: note that this flavour is linked to Beijing. The history of Yanjing Beer elsewhere in this blog shows that linking your product to the nation’s capital can be a winning strategy.

Food delivery offers more variety

The rise of food delivery has also played a role in the declining fortunes of the instant noodle industry. Food delivery gives consumers access to quick meals of more diversified tastes. Users of food delivery services reached 295 mln by the end of June 2017, a 41.6% increase from the end of 2016, according to the China Internet Network Information Center. Food delivery services have even reached high-speed trains (see the previous paragraphs). In mid-July 2017, 27 major railway stations across China launched a pilot on-demand food delivery service for high-speed trains passing through the stations.

Nissin severs ties with Jinmailang

Nissin has sold its interest in three joint-venture operations for RMB 450 mln to partner Jinmailang late 2015. Nissin said that in the future, the company would focus on expanding its business in China through local subsidiaries, without elaborating on exactly why the agreement had been ended. Insiders note that there is a growing preference for foreign brands of instant noodles, particularly in the larger cities such as Beijing and Shanghai, which bodes well for Nissin.

Africa the new frontier?

However, wouldn’t it be an interesting thought that some time in the near future, the consumption of instant noodles in the Western countries could be higher than in China?

Or will the Asian manufacturers succeed in reviving this product with more, and in particular healthier, formulations?

Anyway, I just (Aug. 27, 2014) read an interesting news item on a Chinese food industry site, with an even more intriguing title than the one this blog starts with: ‘Chinese instant noodles are attacking Coca Cola in Africa‘. It starts by reporting that a cup of instant noodles (see the above illustration) is already replacing the traditional corn porridge Kenkey as the typical breakfast in urban Ghana. The reporter then conjectures that Chinese instant noodles are pushing Coca Cola from its position as the leading foreign food and beverage product in that country. Food for thought indeed.

Export to . . . Chinese tourists

A report released jointly on Sept 28 by Alibaba’s Alitrip and Internet finance platform Wacai showed once and for all that Chinese tourists have a true, unswerving love for instant noodles. The report noted that up to 31.29% of Chinese tourists have packed instant noodles in their luggage when going abroad, and 58.24% have bought instant noodles after reaching their outbound destinations. The report shows that 66.14% of tourists born in 1970s pack instant noodles in their luggage, whereas the number is reduced to 53.82% for those born in the 1980s, and 50.96% for babies of the 1990s.

Still a newcomer

Early September 2014, Taiwan-based Wantwant Group suddenly announced that it intends to enter the instant noodle market. Wantwant is a major producer of candy, flavoured dairy beverages, snacks and other leisure food, but so far completely unfamiliar with instant noodles. The only link I can see so far is that the above mentioned top players also originate from Taiwan. Master Kong and Uni-president have not yet reacted to Wantwant’s announcement.

High end experiments

Uni-president attempted to open up a new market segment for its instant noodles by launching a line priced at RMB 30 per cup early 2016. The experiment failed utterly, and the products were recalled within a month after launch.

Flavour maker Haoji (Sichuan) has relaunched its non-fried instant noodles in November 2016. This instant noodle product — branded 99 Love, or phonetically “long-lasting love” in Chinese — is marketed as a healthy product that is made primarily from wheat, corn, buckwheat and potato sourced from high-altitude unpolluted areas; it is steamed, as opposed to fried, during the manufacturing process. An earlier launch failed, because Chinese consumers were apparently not ready for such an innovative product.

Instant relief

However, instant noodles have will remain to be the absolute favourite for one application: quick relief in times of disasters. When parts of China are shut off from the rest of the country due to floods or earthquakes, it is always possible to get a supply of light-weight instant noodles to the disaster area to prevent people from starving.

Instant noodles will remain an important pillar in the Chinese food industry, but it is a mature market and the main players will be fighting fiercely for a few percent for some time to come.

Instant noodle restaurants – are you serious?

Chinese are masters in turning anything around and market it as something completely new. One entrepreneur has played this trick on instant noodles and opened a restaurant annex convenience store chain named Nonoodle (bufangbianmian in Chinese). You can purchase a wide range of instant noodles there and a few other snacks and drinks, but you can also eat your instant noodles in the dining space. The English name Nonoodle is not a literal translation. In Chinese, instant noodles are called fangbianmian, ‘convenient noodles’. So, bufangbianmian literally means ‘inconvenient noodles’. The entrepreneur is suggesting that cooking water, soaking the noodles with the condiments in water, and wait until the noodles are more or less ready to eat is actually not that convenient. Why not let a ‘cook’ prepare the noodles of your choice for you. After the meal, you just go away, home or to another destination. The trick works, as long lines of young consumers can be seen at Nonoodles any time of the day. Amazing.

Corona virus facilitating the revival of instant noodles

When almost all urban Chinese were locked up inside their homes for a few weeks early 2020, it actually was a major boost for instant noodles. It is light, so easy to take home in large quantities. It is tasty and, in combination with some vegetables, chunks of meat, an egg, etc., can be a quite nutritious easy to prepare meal. However, the inventive Chinese invented a broad variety of dishes with instant noodles as the main ingredient. The following picture shows one example of such a novel dishe.

During and after COVID, noodle chains (not only instant) became a serious target for big investors. Once focused on high tech companies, venture-capital funds are pouring money into new noodle chain brands. Even tech giants like Tencent, the mother company of WeChat as well as an active investor, are doubling their bets on the sector. Chinese-style noodle chain restaurants first became tech investor darlings in 2021 when the industry faced tightened regulation while the country’s consumers became increasingly willing to spend more on quality products and experiences. There were twelve noodle chain investment deals in the first half of that year, with a combined total of RMB 1 billion injected into the emerging area.

Eurasia Consult’s database includes 342 producers of instant noodles.