Coffee has been reported on before in my post on Pu’er. People have been talking about the Chinese market for ready to drink coffee a lot since then. Apparently it is a topic that is on people’s minds, so I have bundled their remarks in this dedicated post.

Coffee vs tea beverages

The following table shows the turnover of tea beverages and coffee beverages in China in the period 2019 – 2024, also indicating the ratio between the two. It is clear that coffee is slowly but definitely winning this battle. However, these data also show that the total market of ready-to-drink tea and coffee is growing steadily.

An emerging coffee nation

China is gradually emerging as a coffee producing nation. The country’s current annual production is approximately 100,000 mt, 98% of which takes place in Yunnan, the home province of Pu’er, and the remaining the island province of Hainan.

By the end of 2010, China had 135 coffee processing companies, the geographic distribution of which is can be found in the following table.

| Region | companies |

| Shanghai | 37 |

| Guangdong | 26 |

| Yunnan | 18 |

| Beijing | 17 |

| Hainan | 11 |

| Other | 26 |

This shows that the processing still mainly takes place in the most developed regions and not in the locations where the coffee is grown. However, the Pu’er post shows that the main multinational players have set up shop in Yunnan.

The Chinese have never acquired a habit of brewing coffee at home, which creates a fertile ground for two types of products: coffee shops where you can enjoy your favourite brew (see my post on that market), and Ready To Drink (RTD) coffee products, introduced in this post.

Applying the Chinese instant tea model to instant coffee

Between 2008 and 2013, instant tea has been the driving force in the Chinese tea market, increasing sales by USD 1.7 billion. To date, the popularity of instant tea is almost entirely a Chinese phenomenon, as China accounted for 92% of Asia-Pacific’s instant tea sales in 2013. Instant coffee on the other hand, is immensely popular throughout the region, with China accounting for just 15% of the overall market in 2013. As instant coffee shares many of the attributes that have driven the success of instant tea in China, namely the replication of foodservice options, flavour malleability, convenience, and a young consumer base, applying the innovative packaging of instant tea to coffee may spell further success for Asia’s already booming instant coffee market.

Instant tea in China is composed almost entirely of instant ‘milk teas’ that aim to replicate the sweet flavours of popular street stall/kiosk and café operators like Happy Lemon, Jack Hut, and ChaTime. Popular flavours include red bean and jasmine green, while some also include bobas (tapioca pearls found in bubble tea) for added texture. To make the beverage accessible through retail channels, manufacturers use single-serve packaging of on-the-go paper cups filled with a sealed pouch of instant tea and a straw.

The sweet flavour profile of these milk teas, and economical price tag compared to their on-trade equivalents, makes them particularly popular with younger Chinese consumers. The accessible format and price of instant tea enables young consumers to partake, albeit indirectly, in fashionable foodservice.

Aware of the influence of younger demographics, Chinese manufacturers including the Guangdong Strong and Zhejiang Xiangpiaopiao (2023 turnover: RMB 362.5 billion) are deliberate in their marketing, positioning the products specifically to Chinese youth, through fun packaging, and celebrity endorsements. Xiangpiaopiao is awaiting approval for its IPO before the end of 2015.

Is China the future for instant coffee?

In the past decade, the instant coffee market has actually expanded at rates of 7 to 10% a year, according to the Global Coffee Report; the International Coffee Organization projects a 4% global volume growth between 2012 and 2017.

The country that historically drank about two cups of coffee per year per person is now the fourth-largest global market for ready to drink coffee in terms of volume. The reason? Convenience. A 2012 poll found that 70% of Chinese workers said they were overworked and more than 40% stated they had less leisure time than previous years. Plus, most new buyers are used to boiling water to make tea, often owning just a teapot and not the appliances needed to make a fresh pot of coffee. By 2017, the Chinese RTD coffee market is projected to increase by 129% in volume. A recent study estimates that the value of the Chinese RTD coffee market will be RMB 18.6 bln by 2020.

Like many food innovations, the origin of instant coffee has several claimants.

Instant coffee is tapping into a new market: tea drinkers. As of 2013 in Great Britain, tea bag sales dropped 17.3% while sales of Nescafé instant coffee went up in supermarkets by more than 6.3%. The country known for it’s tea and crumpets may be making a similar transition to China’s tea-drinking population.

Nestlé SA led the Chinese market with 70.8% share in 2017, followed by Suntory at 4.9%, Uni-President at 3.3%, and Starbucks at 3.1%. Coca-Cola re-entered the category with its Georgia brand. Its marketing has improved the brand image and the product’s visibility. Nestlé’s Nescafé, a strong category leader, hired Chinese actress Angela baby for TV advertisements, which boosted sales. Starbucks and Ting Hsin (PepsiCo’s local distributor and bottler) agreed to jointly produce and distribute RTD coffee. Suntory and Huiyuan also set up a joint venture to market RTD coffee and RTD tea. In 2015, Hui Yuan was the largest local player in off-trade volume sales terms.

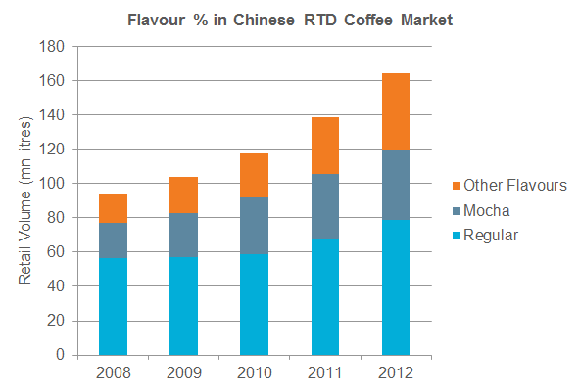

In terms of flavor, the most popular one is latte, accounting for over 54% of off-trade volume sales in 2015.

Coffee as ingredient

Europeans still mainly think of coffee as a beverage made by infusing ground coffee beans with boiling water. The real coffee lovers drink it black, hot and bitter. Those who find that a little too intimidating can dilute it with milk. As most Chinese still have a problem with pure coffee, even with the heavily diluted americanos served by Starbucks or Costa Coffee, a number of coffee flavoured beverages have appeared on the Chinese market. The most recent one Maoyuan Coffee by Wahaha (Hangzhou, Zhejiang).

Multinationals follow suit

A recent development in this market is a strategic alliance between Starbucks and Tingyi. Tingyi, a leading food and beverage producer, has signed an agreement with Starbucks to manufacture and distribute the latter’s RTD products on the Chinese mainland. Tingyi is a well-known supplier of instant noodles and biscuits. According to the agreement, Starbucks will help Tingyi, which makes the well-known Master Kong brand of instant noodles, with coffee expertise, brand development and future product innovation. Tingyi will manufacture and sell the Starbucks RTD portfolio in China, said a statement from Starbucks.

But it will take a lot more than a fancy Starbucks product to convince Americans to drink products like this one sold in China: Nestlé’s instant coffee with jelly.

A multinational like Coca Cola cannot afford to miss out on the popularity of tea beverages in China. The company is marketing its RTD coffee brand Georgia in China.

Taiwan-based manufacturer of snack food, Want Want, had already started looking for divesting opportunities in the beverage industry, when it launched its own RTD coffee brand ‘Mr. Bond’ in 2018. When I am writing this (June 2018), it is still too early to judge the success of this product.

Costa has to follow suit

Costa Coffee could not afford to neglect this market and launched a range of ready-to-drink coffee beverages in China late March 2020.

Jingdong Top 5

China’s leading online store Jingdong keeps track of the top selling brands of any product type the platform has on offer. The following list are the 5 best selling ready to drink coffee brands in 2020

| Rank | Brand |

| 1 | Nestlé |

| 2 | Starbucks |

| 3 | Nongfu Spring |

| 4 | Coca Cola (Costa) |

| 5 | Chef Kong |

Three of the top 5 are international brands, which indicates that it still is a relatively foreign product group. Nongfu Spring is China’s top bottled water brand, but has been expanding to other types of beverage in recent years. Nongfu launched a new type of RTD coffee, branded Yirgacheffee (Tanbing) in 2022 (see the next photo). Chef Kong is the leading instant noodle brand, but has also diversified into beverages a few years ago.

Peter Peverelli is active in and with China since 1975 and regularly travels to the remotest corners of that vast nation.