Don’t say that social media are changing the way we market products and services, until you have learned about their impact in China. The collectivist nature of Chinese culture has undoubtedly affected the speed in which social media have caught on in China. This particularly applies to beer in China.

Largest beer market in the world

China has been the world’s largest beer consuming and producing nation for a number of years. The competition is murderous and the number of individual players is decreasing almost yearly through mergers and acquisitions. The current number of breweries in China is 460, almost half the number of two decades ago. The top 5 breweries now have a combined market share of 73.7%. Chinese brewers are among the most heavy users of the new social media in China in the battle for the consumers’ attention. I have therefore chosen the Chinese brewing industry to illustrate how Chinese food and beverage companies are using the Internet.

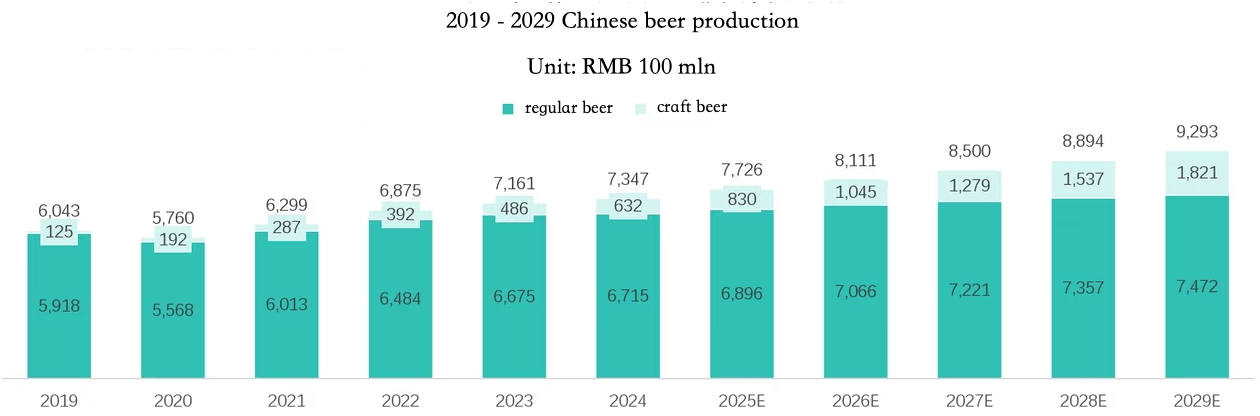

The following table shows the development of Chinese beer production up to projections for 2029. It includes a breakdown in industrial and craft beer.

Weibo – China’s Twitter

Not only individuals use Weibo, the Chinese counterpart of Twitter or WeChat, the Chinese WhatsApp, but with many more possibilities, companies have discovered the power of the social media as well. Beer seems like a great product to investigate the way Chinese companies are exploiting the new media.

China’s top domestic brands Tsingdao and Yanjing immediately reflect a very Chinese cultural trait: imitating. The banners of the Weibo accounts of both brands are related to football. in China too, beer is THE drink for couch potatoes, watching football.

The first posts on today’s (26-9-2014) Weibo site for Yanjing mainly inform visitors of the quickest way to get their hands on a can of Yanjing beer. The other posts relate to everyday life issues like ‘the 30 things that are most worth doing in a man’s life’. I am not really excited.

Tsingdao’s site on the other hand gives a much livelier impression, and tells you what you can eat best with a glass of Tsingdao, or leads you to the Weibo site of the Tsingdao Beer Museum. That is 1 – 0 for Tsingdao, at least from my personal point of view.

International players cannot afford to lag behind and are following suit. Heineken’s Weibo home page is all about . . . Heineken, while Budweiser is measuring itself a musical image, both on the site’s banner and in the content of the first posts.

Public praise

Whether or not a company is active on a social network and if so, with what type of banner is not the most exciting aspect. Much more interesting is the analysis of how and how much netizens discuss a certain brand. In China as well, statisticians have discovered that all that online communication is by no means idle talk, but a true mine of information about the way consumer perceive a certain product, company or brand.

They are referring to this a the koubei (literally: ‘oral stele’) of a brand. Koubei is hard to translate properly. Dictionaries usually give ‘public praise’ as the translation, and I am inclined to go for ‘reputation’, although Chinese usually refers to that concept with another word. However, the figures featuring in statistic reports are not only about praise, but also refer to brand awareness, or the frequency in which a brand pops up in online conversations.

Let’s have a look at the statistics published this week about the way beer brands are discussed in the Chinese online media. The statistics have been compiled by the China Statistical Information Service Centre (CSISC). For each item, I will list the top 3 and Heineken, to see how this top international brand is faring in China.

The first dimension is ‘brand awareness index’.

Rank

brand

figure

1

Tsingdao

6.49

2

Yanjing

2.61

3

Pearl River

1.68

10

Heineken

0.03

Pearl River here ranks higher than Snow Flake, which is China’s current top brand according to turnover. Heineken ends up rather low, with two international brands, Budweiser and Carlsberg, before it.

The second dimension is ‘consumer interaction index’; how much netizens mention a brand in online conversations.

Rank

brand

figure

1

Tsingdao

5.79

2

Yanjing

1.96

3

Snow Flake

1.30

8

Heineken

0.41

This ranking coincides with the ranking using financial indicators. Heineken is quite close, but still lags behind two international brands: Asahi and again Budweiser.

Then we move on to the ‘quality recognition index’.

Rank

brand

figure

1

Tsingdao

4.51

2

Snow Flake

2.62

3

Pearl River

1.56

9

Heineken

0.38

Not much needs to be added here and Heineken only has, once more, Budweiser before it.

The ‘company praise index’ sounds intriguing. This is not about merely mentioning a brand, but doing so in a positive way.

Rank

brand

figure

1

Tsingdao

5.11

2

Snow Flake

3.72

3

Yanjing

2.08

8

Heineken

0.33

Can you guess what international brand outranks Heineken in this table?

The following index, ‘brand praise index’, resembles the previous one but concentrates on the brand rather than the producer.

Rank

brand

figure

1

Snow Flake

13.08

2

Tsingdao

6.43

3

Harbin

5.38

7

Heineken

0.65

Snow Flake is the big winner here, but Heineken is still behind Budweiser.

The final figure is the ‘brand health index’; how healthy do netizens believe a brand is. This seems odd for beer, and indeed the figures literally turn around the brands.

Rank

brand

figure

1

Qingke Beer

0.00

2

Dafuhao

0.00

3

Yellow River

-0.01

12

Heineken

-0.03

Qingke Beer is made in Tibet using the local Qingke barley. This has a relatively healthy image, but because this is about an alcoholic beverage, consumers do not really regard it as healthy. The other beers that come out in high position are all smaller local breweries, that apparently gives them more credit in the health department.

Our Heineken now ranks higher that all top domestic brands and its American competitor Budweiser. However, a number of international brands, like Suntory and Carlsberg, still rank slightly higher.

It is not immediately obvious to draw conclusions about these figures. I will leave that to my readers, but am also interesting in learning your reactions. I am sure more figures like this will be published for other product groups. I will make new items for them, or add them to existing items in this blog.

Output

So how much beer does China actually produce? Here is the regional breakdown of the volume during the first 9 months of 2014, with the in- or decrease compared to the same period in 2013.

Region

Volume (1000 L)

Growth (%)

China

40,924,478.98

1.74

Beijing

1,365,905.07

-4.05

Tianjin

249,319.97

9.17

Hebei

1,437,217.75

15

Shanxi

399,626.20

-2.92

Inner Mongolia

900,010.08

1.28

Liaoning

2,117,929.95

3.10

Jilin

1,135,387.64

1.15

Heilongjiang

1,585,479.68

-3.13

Shanghai

538,281.23

24.56

Jiangsu

1,801,601.02

-1.85

Zhejiang

2,267,633.18

-7.01

Anhui

1,237,393.38

-14.42

Fujian

1,530,728.09

-7.27

Jiangxi

1,020,149.91

4.94

Shandong

6,324,000.21

10.23

Henan

3,372,637.06

8.08

Hubei

1,851,839.85

-1.68

Hunan

651,440.76

-2.37

Guangdong

3,420,602.46

-1.54

Guangxi

1,547,119.61

1.64

Hainan

54,055.00

-6.11

Chongqing

608,640.74

-12.97

Sichuan

1,888,282.58

0.11

Guizhou

620,163.14

54.11

Yunnan

736,064.25

2.45

Tibet

122,985.56

-5.28

Shaanxi

855,607.11

3.59

Gansu

548,007.18

-4.29

Qinghai

86,810.00

2.61

Ningxia

234,304.97

8.96

Xinjiang

415,255.35

-5.40

More interest in traditiional culture (?)

The revival of interest in traditional culture seems to have returned to the Chinese brewing industry as well. China Resources has launched beer with painted faces from traditional Chinese operas on the labels early 2020.

Many Western governments believe that citizens should be encouraged to take care of their own health and see to it that they get sufficient vitamins and minerals by eating a varied diet, with plenty of fresh fruits, vegetables, whole cereals and different protein sources. Adding vitamins and minerals to processed foods is allowed, as long as producers abide by the relevant regulations, but the government does not make public funds available to finance R&D and propagation of fortified foods.

Nutrition as government policy

China is one of the nations that actively support public nutrition. It is even regarded as a basic human right. This means that the government finances R&D into the field of food fortification and the promotion of fortified foods, as a means to enhance the general state of nutrition of the population.

This is not surprising, because the concepts of food, nutrition and medicine are much more intertwined in Chinese culture (Traditional Chinese Medicine TCM) than in the West.

The leading policy making organization here is the Public Nutrition Development Centre (PNDC), an organization under the State Development and Reform Committee of the State Council. R&D is coordinated by the Nutrition and Food Safety Institute of the Centre of Disease Control under the Ministry of Public Health.

This policy, combined with a population of approximately 1.4 billion people, has created a highly attractive market for suppliers of single nutrients, nutrient pre-mixes, and ready-to-eat fortified foods. The Food Ingredients China (FIC) 2018 trade fair (March 22 – 24) included 26 suppliers of various vitamins, and many more of minerals other nutritious food additives.

In October 2016, President Xi Jinping announced the Healthy China (HC 2030) blueprint, a declaration that made public health a precondition for all future economic and social development. The HC 2030 blueprint, released in Beijing by the Chinese government, includes 29 chapters covering public health services, environment management, the Chinese medical industry, and food and drug safety.

Nutrition pagoda

The Chinese love to localise foreign things and ideas. The Western nutrition pyramid has been made Chinese by changing it into the nutrition pagoda.

The Chinese Nutrition Society has issued a special food pyramid for pregnant women late 2019.

Generous budget

The Chinese government has a made a generous budget available to develop pre-mixed micronutrients.

Most micronutrients cannot be simply added to and mixed with other ingredients. Manufacturers of fortified foods need to be sure that the nutritional value of their product when consumed meets the promise they make in the nutrition information on the packaging. Some nutrients lose activity during heating, while others may dislike a low or high pH value. Some nutrients dislike one another’s presence.

This means that many nutrients need to be buffered or treated otherwise. This is specialist knowledge held by a small number of specialist scholars.

These researchers develop processes to protect single nutrients and formulate nutrient pre-mixes in state sponsored research facilities. However, those organizations are less suited for industrial production. A number of more entrepreneurial researchers have set up companies for the production of ready-to-use nutrients during recent years.

Several of them have been very successful and have proved to be fierce competitors to the multinational players like FMC or DSM, who are competing for a share in this lucrative market. The basis of their success is exactly their forming a close and effective chain with government regulators, research institutes, nutrition professionals and food and beverage manufacturers.

Ongoing projects

A number of projects has already been launched:

Infant formulae and ‘nutrition packages’ for primary school children; infant formulae are by far the largest application, as well as the best known one. The nutrition packages are ready to use packages of micronutrients for children of primary school age. Experiments have been conducted with the latter, handing out nutripacks to children (see picture below), but providing such packages has not been institutionalised so far. The packages use soy or soy protein as a basis and add Vitamins A, D, B1, B2, B12, folic acid, iron, zinc and calcium.

Vitamin A fortified cooking oil; as a rice eating nation, many Chinese lack vitamin A and the PNDC has been searching for the best carrier for this vitamin. Cooking oil is one vector that has been tried, in cooperation with COFCO. Products have been launched, but sales seems to be disappointing so far.

Wheat flour fortified with 8 nutrients; Vitamin A is also allowed in flour, another ingredient available in every Chinese household. Guchuan Flower has partnered with the government in developing fortified flour This experiment seemed to have failed as well, because consumers are not willing to pay a premium price.

Fortified rice; in cooperation with Bühler, DSM has develop a process to fortify rice with several vitamins and minerals by making fake rice granules that are mixed with regular rice. This Nutririce is produced in Wuxi (Jiangsu). Bühler acquired DSM’s share in the plant late 2013, but DSM remains committed to developing this product. As rice is regarded as a strategic staple, this entire development process has been conducted in close contact with the relevant authorities.

Iron fortified soy sauce; iron deficiency is huge in China and soy sauce has been found a proper carrier for iron (EDTA iron). It is current the most propagated fortification project in China. A number of soy sauce manufacturers have launched iron fortified products, but again so far the results seem to be somewhat disappointing.

Iron fortified wet noodles and steamed bread (mantou); this multi-nation research project has been initiated by the Food Fortification Initiative (FFI) Secretariat in 2009 and executed by the Nutrition and Food Safety Institute of the Centre of Disease Control. The results were promising, but this has so far not resulted in the regular production of such fortified products.

Probiotics; the fortification of suitable foods and beverages with probiotics like oligosaccharides was officially launched in January 2007. A sufficient intake of probiotics promotes a healthy gut flora.

Iodine salt: until recently, iodine salt was required in all manufactured foods. This law changed in May 2018. Since then iodine salt is only required in specific cases like regions with iodine deficiency. Another aspect of the new rules was that iodine also has to be listed on the packaging of manufactued foods.

The lack of progress of several of the the above mentioned projects seems to indicate that public nutrition in China still has a long way to go. Possibly, the many food safety incidents are negatively affecting these campaigns. Chinese consumers are still waiting for regular food to be safe for consumption, so there is little attention left for fortified food.

Moreover, as a result of the public food safety concern, the Chinese media regularly report about ‘excessive number of additives’ in certain foods like soft drinks or ice cream. Fortified foods need to comply with the regulation to indicate all ingredients on the label, so they may end up with an even longer list of ingredients than the non-fortified competitive products.

National Nutrition and Health Committee

China has created a special committee to implement the country’s national nutrition plan, according to the National Health Commission (NHC). Jointly established by NHC and 17 other government departments to coordinate and advance nutrition and health related work, the national nutrition and health committee held its inaugural meeting on Feb. 28, 2019, in Beijing. Among the key jobs are improving food nutrition and health standards that build upon food safety, and establishing subcommittees at local levels to organise nutrition education and training, to conduct pilot programs and spread scientific knowledge in this regard. The national nutrition plan (2017-2030) was released by the General Office of the State Council in July 2017, with the goal of raising awareness of nutrition among the Chinese people, reducing obesity and anemia among students.

From more to less meat

More recently, the Chinese authorities have included the global campaign for lowering meat consumption in the national dietary policies. Like all nations with a growing rate affluence, Chinese started to eat more meat, when they had more money to spend on food. Eating meat has always been a distinctive trait of the wealthy throughout Chinese history. The China National Dietary Guidelines already encourage Chinese consumers shifting toward a plant-based diet. The national government is planning to cut back meat consumption in half by 2030, not just for health and the environment, but also due to concerns for animal welfare, risks to workers, and antibiotic resistance.

A China Plant Based Foods Alliance (CPBFA) was established in December 2018. One of the first professional trade groups to represent plant-based food sector in China. It is a joint effort of the State Food and Nutrition Consultant Committee (SFNCC), Advisory Committee on Nutrition Guidance (ACNG) of China National Food Industry Association. The CPBFA advocates for plant-based ingredients, food and beverages, closely monitoring and thoughtfully influencing the legislative and regulatory environment. A list of members is not yet available, but a seminar organised late 2019 was attended by a mix of producers, consultants, policy makers and equipment suppliers. I will monitor the Alliance’s developments and report about them here.

Low fat, low salt, low sugar

This is another diet-related movement that has started in the Western world, but is now also gradually growing support in China. It has a common trait with the movement to lower meat consumption: fat, salt and sugar (in sufficient amounts) are also regarded as symbolic for a healthy diet in China. Poor people used to eat little meat, which automatically meant that they were happy with any fat they could get. Salt used to be as valuable as in other parts of the world (don’t forget the etymology of the word ‘salary’!) and sugar not much less. Nowadays, cooking oil, salt and sugar are available in abundance, but during the early decades of the Economic Reforms, Chinese were happy to indulge in these food ingredients that had to be rationed not that long before. Unfortunately, this has resulted in a dramatic increase of obesity, hypertension and diabetes among the Chinese.

The national and local governments have started drawing up dietary guidelines controlling fat, salt and sugar. Guidelines for snack food for primary and high school age students were proposed by the Beijing Public Health Commission and the China Food Distribution Association in May 2020.

Item

denomination

specification

Fat

fat free

<= 0.5g/100 g/ml

low fat

<= 3g/100 g/ml

Sugar

sugar free

<= 0.5g/100 g/ml

low sugar

<= 5g/100 g/ml

Salt

salt free

<= 5mg/100 g/ml

low salt

120mg/100 g/ml

The Beijing proposals not only deal with lowering fat, salt and sugar, but also include adding more dietary fibre to the meals

Chinese dairy industry: from colonialism to imperialism

Through most of the imperial dynasties until the 20th century, milk was generally shunned as the rather disgusting food with horrible odour of the barbarian invaders. Foreigners brought cows to the port cities that had been ceded to them by the Chinese in the opium wars of the 19th century, and a few groups such as Mongolian nomads used milk that was fermented and made cheese-like products, but it was not part of the typical Chinese diet.

When the People’s Republic of China was born in 1949, its national dairy herd was said to consist of a mere 120,000 cows. However, the Chinese government has always supported the dairy industry since the founding of the PRC. However, evaporating raw milk into milk powder has been the major production process for a few decades. This made sense, as milk was produced in only a limited part of China and the milk powder could be easily distributed to other regions and then rehydrated into liquid milk. Milk powder was also the main imported dairy product. Another typical feature of the early decades of the modern Chinese dairy industry was that milk was regarded as an essential drink for two segments of the population: children and the elderly.

As China opened up to the market in the 1980s, milk powder began appearing in small shops where you could buy it with state-issued coupons. Parents bought it for their children, because they thought it would make them stronger. There also was a nationalist aspect to this. China felt humiliated ever since the opium wars, and developing a domestic dairy industry would make the national less dependent on foreign powers.

Today, China is the third-largest milk producer in the world, estimated to have around 13 million dairy cows, and the average person has gone from barely drinking milk at all to consuming about 30 kg of dairy produce a year. In a little over 30 years, milk has become the emblem of a modern, affluent society and a country able to feed its people. The transition has been driven by the Chinese Communist Party, for which milk is not just food, but a key strategic tool. The fact that people can afford animal produce is a visible symbol of the government’s success. Making animal produce, particularly milk, available to everyone across the country is a way of tackling potentially destabilising inequalities that have arisen between the big cities and some of the poorest rural areas while China has developed. In the poorest regions, nearly one in five children are still short for their age, from lack of adequate nutrition.

The Party’s current, 13th five-year plan identifies one of its top priorities as shifting from small-scale herds to larger industrial factory farms to keep its population of 1.4 billion in milk. Official guidelines on diet recommend people eat triple the amount of dairy foods that they typically consume currently. President Xi Jinping has talked in speeches about making a “new Chinese”. In 2014, he visited a factory owned by China’s largest dairy processor, Yili, and exhorted its workers to produce good, safe, dairy products. That new Chinese is expected to be a milk-drinker. His predecessors already launched the ideal that ‘each Chinese would drink one glass of milk per day’. This belief in the power of dairy stuck with the average Chinese as well. Some claim that it took hold with the 1984 Olympic Games in Los Angeles. New mass ownership of television sets had allowed Chinese people to see real foreigners, as opposed to actors, live on TV for the first time. “They were amazed to see how strong and tall foreigners were. They could jump twice as far, run twice as fast. They concluded that Americans ate a lot of beef and drank a lot of milk and Chinese people needed to catch up.” Chinese state planners were also impressed by the way the Japanese had developed. When the US defeated and occupied Japan after the Second World War, they had introduced feeding programs in Japanese schools to give children milk and eggs. Average heights increased within one generation.

As populations urbanise, they have always moved up the food chain, making the transition from diets largely based on grains and vegetable staples to ones in which meat, dairy, fats and sugars feature more prominently. China has followed the same trajectory. Dairy consumption grew rapidly through the 1980s and early 90s. The western model of retailing based on supermarkets with longer supply chains arrived in cities, too, making it possible for producers to distribute milk further and easy for shoppers to buy it. As incomes increased, people could afford refrigerators in their homes and wanted milk to put in them. For factory employees working long hours, dairy foods represented a convenient way to get nutrients without having to cook. Technology to produce UHT milk with longer sell-by dates, imported in the late 90s, gave consumption a further boost. Since fermenting milk helps break down lactose, yoghurt and other formulated dairy products were also marketed to overcome lactose-intolerance.

The reinvention of milk as a staple of modern China has required a series of remarkable feats. It has involved privatising farming, allowing processing companies to become corporations, and even converting desert areas into giant factory farms. As populations urbanise, they have always moved up the food chain, making the transition from diets largely based on grains and vegetable staples to ones in which meat, dairy, fats and sugars feature more prominently. China has followed the same trajectory. Dairy consumption grew rapidly through the 1980s and early 90s. The western model of retailing based on supermarkets with longer supply chains arrived in cities, too, making it possible for producers to distribute milk further and easy for shoppers to buy it.

While incomes increased, people could afford refrigerators in their homes and wanted milk to put in them. For factory employees working long hours, dairy foods represented a convenient way to get nutrients without having to cook. Technology to produce UHT milk with longer sell-by dates, imported in the late 90s, gave consumption a further boost. Since fermenting milk helps break down lactose, new yoghurt products were also marketed to overcome lactose-intolerance.

Now the global impact of China’s ever-expanding dairy sector is causing concern in other countries. Dairy farming requires access to vast quantities of fresh water: it takes an estimated 1,020 litres of water to make one litre of milk. But China suffers from water scarcity, and has been buying land and water rights abroad, as well as establishing large-scale processing factories in other countries. A recent move in this respect was the announcement that Yili Dairy (Inner Mongolia) intended to acquire New Zealand’s Westland Milk Products. The news immediately triggered a host of positive and negative reactions, with headlines like: ‘Can the world quench China’s bottomless thirst for milk?’. So, while Western imperialism laid the foundation of the modern Chinese dairy industry, China is now ‘colonising’ the former imperialists.

National School Milk Programme

The Chinese government has introduced the National School Milk Programme in 2000 to support the improvement of students’ nutrition and the development of the Chinese dairy industry. After a decade of operation, the programme reached more than 8 mln students by the end of 2011. And thanks to the Nutrition Improvement Programme for Rural Compulsory Education Students (NIPRCES) launched in 2012, the School Milk Programme more than doubled its coverage in the following years. At present, nearly 20 mln Chinese students receive milk in their schools every day on average. The School Milk Programme creates demand for higher quality and locally produced and UHT processed milk, sourced from licensed dairies. After the School Milk Programme was introduced in 2000, China’s raw milk production increased by 10% per annum over a period of 13 years, dairy cattle stock increased from 4.6 mln to 14.4 mln and annual dairy products consumption volume per person grew from 6.7kg to 27.86kg. A study made in 2009 shows that children gained an extra of 1.2cm in terms of height and 0.6 kg in terms of weight on average after receiving school milk regularly for three years. Though the School Milk Programme has expanded quickly over the past years, it covers only 15% of the total students at the stage of mandatory education. In light of increasing public attention on student nutrition status and the expansion of programmes like NIPRCES, the School Milk Programme is expected to benefit more students in the future.

Entrepreneurial initiatives

However, there is already a large number of fortified foods available in China. Many of them add single nutrients, in particular calcium. Calcium deficiency is rampant in China as well, and calcium compounds are easy to add to foods and beverages. Iron, zinc, magnesium and vitamins in various combinations are added too.

An interesting example is Mondelez (formerly Kraft) that is producing biscuits in China with 10 nutrients added. The following table shows the content of each nutrient per 100 gr of finished product as indicated on the consumer packaging.

Nutrient

dosage

Vitamin A

833 IU

Vitamin B1

0.4 mg

Vitamin B2

0.4 mg

Niacin

4.0 mg

Vitamin B4

0.4 mg

Vitamin D

3.2 mg

Folic acid

58 mg

Zinc

4.5 mg

Iron

4.0 mg

Calcium

290 mg

Another example worth mentioning here is Bread Pan, produced by Oishi, a Chinese venture of Philippines based Liwayway Holdings. The bread is sold as packed slices and marketed as a breakfast food. It is flavoured with shredded beef. Added nutrients per serving are listed as follows.

Nutrient

dosage

Vitamin A

43 iu

Vitamin C

9.80 mg

Vitamin D3

17.55 iu

Vitamin B1

0.50 mg

Vitamin B2

0.15 mg

Vitamin B3

1.30 mg

Vitamin B6

0.15 mg

Vitamin B9

11.70 mg

Vitamin B12

0.13 mg

Vitamin B5

0.40 mg

Calcium

63 mg

Iron

0.70 mg

Zinc

0.40 mg

Some manufacturers seem to struggle between the will to make their product more nutritious additives and the need to maintaining the texture and flavour of the original product. In other posts, I have pointed out that most industrial bread sold in China comes with an impressive ingredients list. Mankattan Food is offering a ‘fortified bread’ with the following ingredients.

This bread indeed supplies the consumer with some additional nutrients, but also contains a number of non-natural ingredients that are not strictly needed to make artisanal bread.

Most of these manufacturers of fortified foods and drinks do not cooperate with PNDC. This indicates that lack of strategic and marketing knowledge is part of the problem in propagating public nutrition by the authorities.

Yake Food (Fujian) produces a fruit-flavoured candy, Yake V9 Candy, enriched with 9 vitamins.

Each candy is said to contain the following vitamins:

Vitamin

Dosage

C

23.04 mg

B3

3.13 mg

E

2.82 mg

B5

1.37 mg

B2

0.32 mg

B1

0.32 mg

B6

0.27 mg

Folic acid

79.8 mg

B12

0.47 mg

Ice cream maker Zhongjuegao has launched ‘ice cream for non-adults’ in 2019. It is fortified with vitamins A and D and calcium, as many drinking milk products in China.

Does it work?

So is a public nutrition policy like that of the Chinese government more effective that the propaganda to eat well policy of most Western governments? So far, no comparative research has been conducted. My personal impression (I have been involved in a global market survey concerning public nutrition) is that big city dwellers in China or West Europe usually have few nutrition problems. They have the knowledge about nutrition and have access to nutritious food ingredients. The difference could be in the poorer regions on those countries and the entire globe. It does make sense to add nutrients to staple foods or food ingredients that are used in most households.

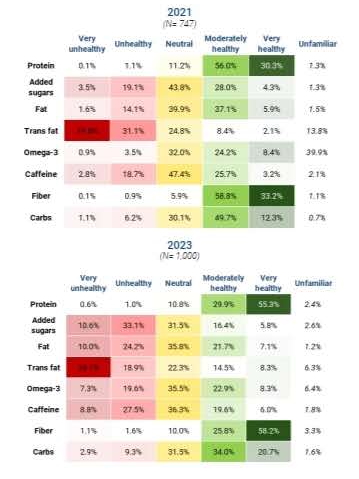

Here are some of the results of market surveys about the perception of the nutritional value of several foods and food ingredients in 2021 and 2023.

And here is a table showing the nutritional perceptions of food (groups) in 2024.

The influence of nutritional education is most clearly visible in the consumption of supplements among Chinese consumers (2024).

According to a Chinese saying, no visit to Beijing is complete if you miss climbing the Great Wall or dining on Peking Duck.

Long history

Eating roast duck in China dates back as far as the Northern and Southern Dynasties (420 – 589). Up until the Southern Song Dynasty (1127 – 1279), ducks were roasted in the area around Jinling, today’s Nanjing. According to the book of The Eastern Capital: A Dream of Splendors Past, written by Meng Yuanlao (1090-1150). The book gives a lively and detailed description of life in the Northern Song capital of Bianliang, based on the author’s reminiscences of his youthful years there.

Ducks eggs are consumed more in China than in European cuisine. They are particularly popular are raw material for preserved eggs.

The following Yuan Dynasty (1271 – 1368; yes, there is an overlap with the Song, as the Mongol rulers of the Yuan Dynasty conquered China gradually) rulers moved their capital city to Beijing. According to the Standard History of the Yuan, Roasted Duck only spread to Beijing after Bayan of the Baarin the general of the Yuan Dynasty conquered Lin’an, the then capital city of the Southern Song Dynasty. When a Dynasty overthrows another dynasty the capital also changes, the general relocated all the skilled workers from Lin’an, to the new northern capital, Beijing and the skilled duck chef was among them.

The ducks were originally roasted in a conventional convection oven until Qing Dynasty (1644 – 1911), when a new type of cooking method and special oven were invented. According to the new method, the ducks were suspended over the flame in an open oven. In that way, the interior and the skin of the ducks were cooked simultaneously, producing that well known end-product with its tender meat and crispy (brushed with a layer of sugar) skin. Preparing a Peking roast duck takes at least four steps: preparing the duck, pumping air beneath the skin, drying and roasting.

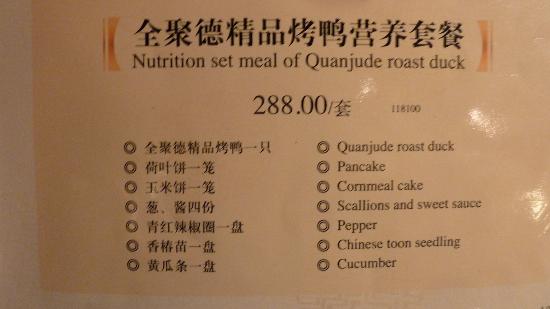

The restaurant best known for applying this method was Quanjude, founded in 1864 by Yang Quanren. Today, Quanjude has almost become a synonym of Beijing Roast Duck to many Chinese. It is a state owned enterprise listed on the Shenzhen Stock Exchange. Quanjude’s Hepingmen branch not only offers gourmets a chance to dig into the traditional food but also the whole roast-duck culture, thanks to a 1000 square meter museum on the seventh floor.

From 1949, Zhou Enlai, the first premier of the People’s Republic of China would often treat foreign guests with Peking Duck. It became part of China’s foreign diplomacy, along with table-tennis.

More local cuisinese are known for their duck dishes, in particular that of Nanjing, where people prefer to eat pieces of duck, rather than the whole thing. However, Peking Duck is still the national leader.

The Chinese duck raising industry exceeded RMB 100 billion for the first time in 2018.

The British connection

Present day ‘Peking’ ducks actually have an English background. Cherry Valley, based in the northern English county of Lincolnshire, started importing interbred Peking ducks to China in the 1980s. Some insiders estimate that by 2016, at least 75% of all ducks sold in China were Cherry Valley breeds. Others give a lower estimate of about 60%. Beijing-based cooks prefer the local ducks, which have a higher fat percentage in weight.

New presentations

Quanjude had updated its menu earlier in July 2015 to showcase its long-standing culinary heritage. The latest menu features “peony duck”, which is a roast duck presented like a peony flower in full blossom — the delicately sliced breast meat is layered to give the impression of petals, while boiled towel gourd parts make up the green stalk and leaves. The dish was first served at a State banquet during the Asia-Pacific Economic Cooperation summit November 2014 in Beijing, where leaders of more than 20 member economies were present. The Quanjude-made dish has since been served to customers at all branches of the restaurant in Beijing, according to Sun Zhongmin, director for the group’s innovation center. The restaurant has also launched an individual summer special menu of 11 new dishes consisting of both cold and hot items, soups, dumplings and desserts.

Another restaurant experimenting with modernised version of the traditional Peking Duck is the Shang Palace Restaurant in Beijing. However, the novelty is mainly expressed in the presentation of the various ingredients (pancakes, condiments, etc.) as shown by the picture.

Patent

A recent innovation was introduced by Sun Lixin of the Bianyifang Duck Restaurant (founded in 1416) in 2003. Sun added a step before roasting – soaking the 3-kg duck in pure juice extracted from onions, carrots, celery, bay leaves, rosemary, tarragon, celery seeds, and aniseed, adding mushroom powder and mirin. A patent was granted for this process (patent nr.: CN1543863). The vegetable juice, being alkaline, eliminates the pungency of the duck but also reduces the duck fat beneath the skin.

A complete meal

Peking Duck is eaten with shredded spring onions and cucumber dipped in a sweet fermented sauce (jiang), and wrapped in thing wheat pancakes. The liver, stomach and heart are usually prepared separately and served as side dishes. The meal ends with duck soup made from the carcass and whatever else is still left of the duck.

Peking Duck is by no means light food. Even though the new roasting method removes a major part of the fat, the total Peking Duck experience it is still high in protein and carbohydrates. It is so tasty, that you keep eating, and by the time the signal from your stomach telling you that it has more than enough reaches your brain, it is too late.

Peking Duck is therefore not a dish that is eaten frequently. It is nice to reserve it for a special occasion like a holiday or a birthday, enjoying it with the entire family or a group of friends.

Innovation

The typical route to innovate Peking Duck and adapt it to the life of the modern urban Chinese is to chop the bird in small one-bite pieces. It so happens that Chinese love to nibble on bones, or chew on tougher bits of meat, much different from the Western preference for tender meat.

A number of companies have therefore developed duck wings, duck tongues, duck necks, duck hearts or duck gizzards as one-bite snacks. They are usually individually wrapped, with around 20 snacks in a larger pack.

These products are much easier to take pack in your hand luggage on a trip, or eat while watching TV or reading a book. Sharing a few duck wings is also less of a burden to the body than eating an entire duck.

Juewei duck necks – the ultimate taste

One manufacturer of duck products has gained national fame with its duck necks that are not only sold as packed foods in supermarkets, but also fresh and hot from its 5000 special outlets.The company was established in 2006 as Jueweixuan Business Management Corporation in Changsha (Hunan). A consortium including Kunwu Jiuding Capital Co., Ltd. and Fosun Group has invested RMB 260 million in Juewei in 2011. Juewei generated a turnover of RMB 4.386 billion in 2018; up 13.46%.

The company’s brand name Juewei literally means ‘ultimate taste’. This may strike us as rather presumptuous, but the popularity of the products (as well as the large number of copy cats) seems to indicate that the company has lived up to the promise contained in its name. Juewei Duck Necks are as well known in China as KFC’s hot wings. It is an interesting fight between the Chinese duck and the American chicken, and in view of the recent quality problems that have affected KFC in China, the duck seems to be on the winning hand. However, the battle is still going one.

By the way; the standard recipe for duck necks includes . . . chicken bones, great and cheap flavour enhancers.

Zhouheiya – a model in brand building

Zhouheiya (Hubei) is another Chinese fast food chain known for their signature spicy duck necks. It gained its name from its founder, self made billionaire Zhou Fuyu. Zhouheiya has 400 stores in communities, airports, train stations and other major locations across China. An alliance between a food chain famous for duck necks and a robot might not seem like the most likely combination. But Zhouheiya made it possible by advertising in the film Transformers 4, benefiting immensely from the cooperation. Zhouheiya has ambitious plans to enlarge its production in America and Europe.

Zhouheiya got listed on the Hong Kong Stock Exchange in 2016. Credit Suisse Group AG and Morgan Stanley are sponsors, or banks responsible for the IPO.

Zhouheiya’s factory

Zhouheiya generated a turnover of RMB 3.249 bln in 2017; up 15.4%. The company has mainly lifted by surging online sales and increased number of retail stores across the country. The group has established a strong presence in 11 major domestic online market places, including one newly operated storefront on Jumei.com, in the first half of 2017. “By leveraging its own social media channels, the company enhanced customer loyalty by active interaction with the customers.” The company has been reshaping its brand into a trendy snack in an attempt to lure young customers, especially millennials, into buying what used to be seen as an old fashioned snack food. Zhouheiya made headlines in 2014 when its logo briefly appeared on screen in the Hollywood blockbuster Transformers: Age of Extinction, creating valuable media buzz for the brand.

Zhouheiya expanded its business to agrifood research by taking a 16.67% stake in Hubei Mingchuang Agritechnology Development Co. early 2022.

Another competitor from Hubei is Jingwu (Kingwuu). Jingwu has derived its name from the well-known Jingwu Road in Wuhan. The company is a supplier of cooked and marinated duck and goose meat products. Jingwu aims to develop a series of products with special characteristics including preserved Jingwu duck necks, and duck feet with a unique taste.

One of the earlier players in the lucrative duck neck market is Huangshanghuang from Jiangxi province. This company was founded in 1993 as a collective enterprise in Nanchang, the capital of Jiangxi and gradually developed into the Huangshanghuang Food Group. It was listed on the Shenzhen Stock Exchange in 2012. Although it is a predecessor of Zhouheiya and Juewei, Huangshanghuang’s turnover of 2017 was RMB 1.478 bln, so considerably less than the two leaders. However, as Huangshanghuang has a much broader product range, we should be careful in comparing it with the two duck specialists.

Duck necks have become such a fad these days, that a duck neck eating competition was organised in Wuhan in July 2015. According to the rules, participants were asked to finish a 350 gr box of duck necks and leave no more than 150 gr of bones in as short a time as possible. However, the success of the two Wuhan-based companies Juewei and Zhouheiya is so huge, that one competitor, Shanghai-based Jiujiuya, has adopted a strategy to attack them in their own home region. Jiujiuya is advertising its products as ‘Wuhan-style duck necks’, ‘Wuhan-style duck wings’, etc. The company also appointed a former CEO of a major mineral water brand from Guangzhou as its regional manager for Central China, indicating that it is focusing its marketing efforts on the heartland of duck necks. The following picture shows a typical Jiujiuya outlet.

In 2020, Jiujiuya changed its positioning strategy to the then current trend of imitating Chinese advertising of the 1920s and 30s.

Goose chasing the duck

Zhouheiya entered 2018 with a new strategy to battle its main competitor: the company added a range of goose products to its portofolio. So far, there has been no reaction to this move from Juewei.

From duck necks to ducklings

The Chinese affection for nibbling on duck necks has stimulated the creation of several innovative dishes. Here is lovely one that I found on a Chinese recipe site. The name of the dish is ‘miniature babao calabash ducks’. The term babao ‘eight treasures’ has been introduced in an earlier post on babao porridge. As the picture shows, the ‘ducklings’ in this dish indeed look like miniature calabashes. They are in fact sections of duck necks, stuffed with glutinous rice. On the plate they strike you as small calabashes. Apparently, the Chinese cook does not want to run the risk that discriminating customers will criticise that they ‘don’t look like ducklings at all’. So he has carved a ducks out of vegetables; to make the dish more ‘ducky’. This is one of those Chinese paradoxes: the veggie ducks look more like ducks that the duck neck ducklings do.

Bloody profits

Even duck blood can be transformed into earnings. Huaying Cherry Valley (Xinyang, Henan) is investing in improving duck blood processing. The company has a special subsidiary to develop a range of products from duck blood, including blood powder and blood beancurd. The company processed more than 10 000 t of duck blood in 2014.

Hearty snack

Piaoling Dashu has developed duck hearts into snack food. This food ranks under the traditional Chinese category luwei, meat cooked with a mix of spices in which star aniseed is the most prominent. Ingredients:

Dong Zhenxiang, Beijing’s legendary Peking Duck maestro, once joked that would serve up his specialty on a hamburger bun with a side of fries. Da Dong’s birds are so enshrined for special occasions that a downmarket sandwich, paper-wrapped for easy takeaway, seemed just plain odd. But no-he really pulled it off and we must admit that Dong is really on to something. His succulent signature duck comes with a tart bit of pickle in the salad layer that makes the plum sauce sing on the fresh bun.

Dadong – Duck with a Western touch

A newcomer in the world of Peking Duck is Dadong. The name of this restaurant chain is derived from the surname of the chef/owner Dong Zhenxiang. He uses customised Justa ovens whose design is top-secret. They have indentations on the walls that bring the oven up to the right temperature. Dadong’s specialty is subuni (literally: ‘crispy, not greasy’) roast duck. However, the customers of Dadong are not only paying to enjoy the food, they also will experience Dadong’s yijing (‘artistic conception’) cuisine.

Yijing cuisine features an exquisite Chinese cultural interpretation to culinary creations – each dish is incorporated with the elements of artworks such as Chinese poetry, literature, painting and bonsai grooming. It makes many of Dadong’s dishes resemble those of European Michelin-starred dishes. The first US subsidiary of Dadong has opened its doors in New York on Dec. 11, 2017. Dadong has had a tough time impressing the New York critics. According to Mr. Dong in an interview of January 2019, the subsidiary in New York is more of an artisan bistro, a new concept, but it is hardly making any profit.

Dadong expanded its overseas presence further by teaming up with Dubai-based JA Resorts and Hotels in 2018, as the latter is eager to attract more Chinese tourists. The group’s Manafaru resort hosted over 5000 holiday goers from China in the past year, accounting for about 50% of total guests.

Duck as ingredient

Staying true to the core notion of this blog, ingredients, I need to point out how duck can also be even further processed to a food ingredient: duck powder. According to a major producer, Weixiangyuan (Guangdong), duck powder can be used to flavour a wide range of foods like soup, leisure food, snack food, biscuits, etc.

Yoghurt is the most widely acceptable dairy product among Chinese consumers. The size of China’s yogurt market is expected to exceed RMB 210 billion in 2023.

Yoghurt has always been one of the more popular dairy products in China. The value of the Chinese yoghurt market for 2020 is estimated at exceeding USD 37 mln, with a per capita consumption at 6.8 kg. An important reason is that it is easier to digest by people with lactose intolerance. Yoghurt is also less ‘creamy’ in taste that liquid milk, and lacks the alien smell of most Western cheeses. It is therefore no surprise that so many new yoghurt products are launched in China.

The Chinese yoghurt market is dominated by the two Inner Mongolian giants Yili and Mengniu and their Beijing cousin Sanyuan and Shanghai-based Bright as the Benjamin. The following table shows the yoghurt market shares of the major companies in January 2018.

Low- and room-temperature yogurts: different growth prospects

Within the Chinese yogurt market, there are two distinct varieties to consider, according to their storage temperatures. Low-temperature yogurt, favoured for its superior taste and nutrition, comes with a shorter shelf life and demands specialized logistics, including cold chain technology for transportation to the retail destination. Room-temperature yogurt largely dominates the market, boasting nearly double the transaction volume of its low-temperature counterpart in 2021. Nevertheless, while the former experienced a growth rate of 6.1% from 2016 to 2021, this growth is anticipated to slow down to 3.6% between 2021 and 2026. Conversely, low-temperature yogurt has exhibited a remarkable growth rate of 14.3% and is projected to maintain a steady growth of 11.4% in the forecasted period from 2021 to 2026, thus narrowing the gap between the two varieties.

Old yoghurt newly formulated

However, even though a large variety of yoghurts is available in the local supermarkets, Chinese consumers have started to grow bored with the relatively sweet and rather liquid products.

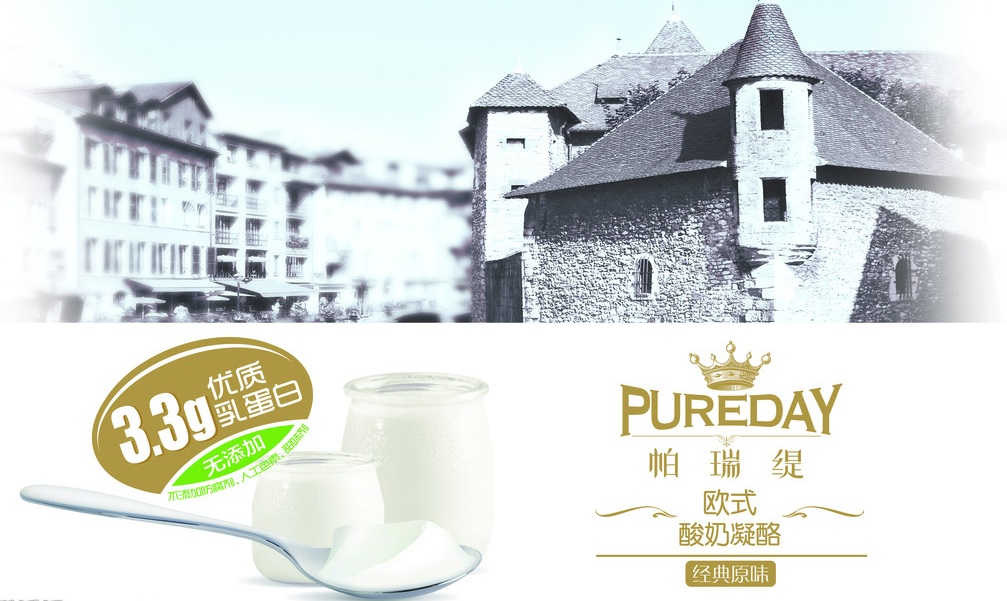

To counter the demand for a new type of yoghurt, a number of Chinese dairy companies started launching more viscous products a year and a half ago, resembling products like Greek yoghurt or quark. In fact, Yili (Inner Mongolia) has launched a Greek yoghurt early 2016 (see photo). They are market as ‘old yoghurt’, trying to create a ‘traditional’ image; yoghurt as it originally used to be.

Huishan Dairy (Liaoning) has launched a type of Russian yoghurt early 2017, branded Wolingka.

After so many food safety incidents, an investigative journalist of the Beijing Evening News purchased old and regular yoghurt of three leading brands, to compare the ingredients used in each product, as listed on the packaging. He has furthermore interviewed a number of experts in this field.

The results allow us to have a look into the kitchen of the present day top producers in this industry in China, and one with a rare degree of detailedness. We will start with offering a translation of the information of the 8 products (4 brands of Old Yoghurt and 4 types of normal yoghurt of the same brands). For each product, the following information will be provided: brand and product name, ingredients, and price. I will then summarise the judgments of the journalist and the experts and end with some comments from my side.

Junlebao

Traditional Old yoghurt

Raw milk, sugar, whey protein powder, streptococcus thermophilus, lactobacillus bulgaricus additives (HPDSP, gelatin, pectin, monoglyceride, aspartame, acesulfame-k)

Raw milk, sugar, streptococcus thermophilus, lactobacillus bulgaricus, additives (gelatin, diacetyl tartaric acid ester of mono(di)glycerides, pectin, xanthan)

RMB 3.80/180 gr = RMB 0.021/gr

Plain yoghurt

Raw milk, sugar, streptococcus thermophilus, lactobacillus bulgaricus, additives (gelatin)

RMB 9.50/800 gr = RMB 0.012/gr

The journalist’s findings

Retailers generally like the Old Yoghurt, which they describe as ‘selling itself without any marketing effort’. Most consumers interviewed while buying it state that Old Yoghurt has an ‘original’ taste and ‘reminds one of the past’.

The price difference is significant. It is smallest for Junlebao, but for the other brands, the Old Yoghurt is on the average twice as expensive per gram as the regular variety.

However, these differences in price are not reflected in the lists of ingredients. Actually, these are remarkably similar for the Old and regular varieties. Moreover, the differences between the various brands are also very small. Even more peculiar is that an ingredient that is typical for Old Yoghurt in one brand is typical for the regular variety for competitive brand.

Apparently the only real difference between these two types of yoghurt is that dosage rates of thickeners, giving Old Yoghurt the thick mouth feel that traditional yoghurt used to have.

The experts’ opinion

The journalist has interviewed a number of dairy scientists on this topic. All agree that Old Yoghurt is a ‘concept’ rather than a real product. Real traditional yoghurt was a solidified milk, produced by fermenting raw milk with certain bacterial cultures in stone jars. There is nothing mysterious about it.

All brands of Old Yoghurt described by the journalist contain gelatin; and so do even some of the regular yoghurts. The thicker mouth feel is thus emulated by means of additives. The current Old Yoghurts are certainly not healthier than the average yoghurts.

My comments

This is a fascinating discussion. Actually, in European regular media we rarely find such detailed reporting on the use of food ingredients to ‘construct’ images of food products. Evidently, the food safety incidents that have taken place in China during the past couple of years have sensitised the awareness of Chinese consumers to an extent that consumer associations in Western countries can only dream of.

The issue revealed here by a Chinese journalist is by no means a typically Chinese phenomenon. One can buy semi-finished muffins and other types of cake in Europe, than can be baked at home to enable consumers to serve hot freshly baked muffins to their guests. TV commercials advertise these products showing people in the street smelling that (grand-)mother is baking cake. We are not aware of protests by consumers or consumer associations about such commercials. What European consumers seem to miss is how it is possible to smell a cake being baked from such a large distance.

Our ‘(grand-)mother’s apple pie’ is also emulated with premixes containing artificial flavours. These are further combined with emulsifiers and other additives, to ensure that even the most inexperienced person can bake such a pie or muffin. These additives are all approved for use in food, but so are the ingredients of Old Yoghurt in China. The Chinese journalist is not exposing excessive use of ingredients or the use of illegal additives. He is simply pointing out that consumers need to be aware of the fact that current Old Yoghurt is not related to the traditional thick yoghurt that Europeans use to eat when they were young. In this respect, Chinese consumers and media seem to be a step ahead of their European counterparts.

A few days after this publication on Old Yoghurt, another article appeared interviewing two more dairy experts. Their judgment was significantly milder. Old Yoghurt was first launched by a relatively small company in Qinghai, a region where people are traditional consumers of dairy products. Once that product became a success, it was imitated by dairy companies all over China. However, these companies lacked the skills to produce a thick type of yoghurt in the traditional way. The move to thickeners is then easily made.

The experts further point out that gelatin, starch and most other thickeners are natural products that are used in a large number of foods, and even in the kitchens of many consumers. Their use as food ingredients has been approved and there even is no maximum dosage rate for this kind of ingredients. The dairy experts do point out that there are better ways of producing a thicker kind of yoghurt, like lowering the water content of the milk. This requires more technical skills than adding thickeners. The current problems of Old Yoghurt in China are therefore directly related to the large number of relatively small companies, lacking skilled staff.

Recent developments

The most recent development is that the more and more producers are replacing the term ‘old yoghurt’ with other fancy names. Yili has launched a ‘Pureday Clotted Yoghurt’ and Junlebao a ‘Laojuezhuang European Sour Cheese’ (laojuezhuan literally means ‘cheese estate’. The names and design of the packaging shows that the basic proposition, that these are traditional European products, is now emphasised even more than before.

Organic yogurts are proving popular for health-conscious office workers and young parents. Discerning shoppers seem willing to pay that little bit more for the right products as supermarkets start stocking an array of upmarket brands. Classy Kiss, a yogurt rolled out from Green’s Bioengineering (Shenzhen) Co Ltd, posted significant sales growth in third and fourth-tier markets. It recently launched an organic brand, which sells at around RMB 14, one of the most expensive products from its dairy range. Earlier, it also launched a yogurt designed to help improve the digestive system after a meal. The company hopes it will be able to cash in on the growing demand for healthy products. Sales of functional and fortified yogurts in China are expected to rise 23% to RMB 43 bln in 2017 compared to 2016. By 2022, sales are expected to surge 56% to RMB 75 bln.

Drinkable yoghurt for the young

Younger Chinese consumers have taken a fancy to creamy, sweet, flavored yogurt and yogurt-based drinks. Category sales have surged about 20% annually since 2014 to reach RMB 122 bln in 2017. Chinese consumers perceive yoghurt as “nutritious”, “helps to boost immunity”, “easy to digest” and “suitable for children and the old”. Yogurt has become a leading product in the domestic dairy market. But compared to other countries, yogurt consumption in China is relatively low at 3.43 kg per person per year (Japan leads with 9.66 kg and the figure for the United States is 4.92 kg). The recent uptrend in yogurt sales in China has positive implications for the larger dairy market. Overall dairy sales in China are expected to exceed RMB 480 bln by 2022 on a compound annual growth rate or CAGR of 6.6%.

Le Pur yoghurt

A noteworthy new arrival on in China’s domestic yoghurt industry is Le Pur. The name embodies the company’s simple and down-to-earth ambition of providing pure and delicious, quality yoghurt. With its dairy imported from countries such as the UK and New Zealand, and other ingredients, such as freshly-picked blueberries sourced from Shandong Province, hazelnut jam from Germany and vanilla from Madagascar, Le Pur aims to provide only “genuine ingredients.” Le Pur’s founder and CEO Denny Liu, a graduate of the Wharton School and a former employee of the Blackstone Group. Liu was also a special adviser to world leading industrial companies like PepsiCo. In late 2014, Liu gave up his career and started to make dairy from scratch. Within a year, he started Le Pur and gained over 40,000 fans on Le Pur’s official Sina Weibo and WeChat public accounts. So far, the number of fans has grown to around 320,000. Just a few months after launching Le Pur, Liu branched out into online to offline operations, and the company’s daily sales volume grew to around 1,000 bottles, according to cyzone.cn, a news platform for start-up businesses in China, on May 10, 2015. One of Le Pur’s marketing strategies is its down-to-earth interaction with consumers. In their concept store in Sanlitun, they showcase the yoghurt’s production line in a 30-square-meter room. The store has never lacked visitors. Le Pur also involves its customers in the choice of flavour and package design.

Salty yoghurt

Terun Dairy (Xinjiang) surprised the market by launching a new type of salty yoghurt late 2018. This flavour fits in with the worldwide vogue for salty sweets, like salty caramel or salty chocolate.

Greek yoghurt

Yili Dairy and the Greek Academy of Agricultural Science founded Ambrosial yoghurt. The sales of this company increased with 106.7% in 2016 compared to 2015. The reason for this sustainable amount is due to the fact that Ambrosial yoghurt is a sponsor of the Chinese popular tv-program Running Man. The viewers of Running Man are the Chinese youth who are also the ones who are responsible of the increase in yoghurt sales. In total Yili Dairy Group spent over RMB 2.5 bln on tv-ads, print media and radio in 2016. In addition to that Ambrosial yoghurt has also launched new varieties of yoghurt and improved old recipes. For example, for a new variety is, the new peach oat flavour. And by launching more diverse flavours, Ambrosial is responding to the sophisticated taste of the Chinese consumers.

The two companies in the top 100 are both state owned enterprises that have succcessfully adapted to the new economic reality in China. Still, the second two are private enterprises.

Spirits remains the best represented type of business with four companies on this list. If we broaden the scope to alcoholic beverage in general, we can add Qingdao and COFCO (Great Wall Wine) as well, to make 6 out of 17 companies.

However, as Mengniu Dairy is now a subsidiary of COFCO, the current list also de facto comprises 4 dairy companies, 2 of which are in the top 100.

You may want to compare this list, which is based on the 2013 turnover, with the list of the Top Food Companies of 2014, which ranks the enterprises according to their estimated brand value.

Food & Beverage in China’s 2017 top brands

The 2017 China Top 100 brands have been published late May. I have extracted a sublist of the food and beverage companies in that list and simply add it to this blog, so we can compare the results with the situation of 2014. First the list.

Spirits stand out as the leading industry with 6 out of 18 brands in the national Top 100. Dairy is the runner up with 4. Quanjude is a restaurant chain rather than a manufacturing company, but it also markets vacuum packed ducks ready for consumption. Regular readers of the blog will recognize most of the names. Don’t hesitate to use the Search function to look for more information of each company in other posts.

Almost all companies have rising dramatically, in particular Moutai. Three years ago, only 3 F&B companies were included in China’s top 100, now 18. This corroborates what has been said about the Chinese food industry in numerous recent publications: it is rapidly becoming a pillar of the national economy.

The development of traditional Chinese foods and beverages to modern industrial products is one of the recurrent themes of this blog. Today I am thrilled to introduce the an innovation process that has already reached a third stage.

Traditional

Huamei, dried and preserved plums, has been a favourite snack of Chinese, in particular ladies, for ages. It refreshes the mouth and the mind. It can be taken after a meal to help digestion and to get rid of bad breath, after indulging on garlic. And after a sumptuous lunch it also gives the mind a boost that can keep your engine running, when it starts dozing off.

The traditional huamei were basically dried and salted plums, scented with licorice and sometimes other ingredients like: lemon juice, aniseed, cloves or cinnamon. This was done for obvious reasons: preservation of the fruits in a relatively hot and humid climate. They were sold in dispensaries and shops specialising in dried and preserved fruits,

Huamei as ingredient

Huamei can also be used as an ingredient. It is e.g. the main ingredient in the traditional plum sauce, combined with garlic, chili, ginger, dried tangerine peel (chenpi), soy sauce, salt, rock sugar, and starch.

In cooking, the sweet & sour zest of huamei can complement the flavour of fatty meat, in particular duck or spareribs (see illustration). Here as well, it is often combined with dried tangerine peel.

Industrial

In the course of the 20th century, huamei were packed in glass jars and later in plastic bags, each plum wrapped in a special paper to retain the moisture.

People started eating them more like a snack, so huamei became part of that very Chinese food group called ‘leisure food‘.

These products were adapted to large scale industrial production. Several additives were used to stabalised the texture and the flavour for a longer period. Here is a standard recipe

Ingredient

weight

Dried plums

100 kg

Licorice

2.5-3.0 kg

Salt

3-5 kg

Sodium cyclamate

2-3 kg

Citric acid

1-2 kg

Potassium sorbate

100 gr

Cinnamon/cloves/aniseed

50 gr each

Chinese plum processors have formed an association to jointly defend their interests in March 2019.

Innovative

Jinguan Food Co., Ltd. (Pujiang, Fujian) has developed a candy based on huamei, called Heitang Huamei, literally: ‘Black Sugar Huamei’. That English translation may not sound particularly appetising, but is probably derived from the dark colour of the product.

This candy gives a unique flavour sensation. The first impression is sweet and creamy, but as soon as the miniscule pieces of huamei are reached, the refreshingly sour taste of huamei emerges to counter the sweetness. It is still highly appreciated after a meal, or when you are starting to feel sleepy behind the wheel of your car.

The product’s label lists the following ingredients:

While the first innovative step mainly addressed the adaptation of the traditional product to economic scale production, the second step was more innovative, using modern food technology to create a combination of flavours more complex that the traditional huamei.

Another innovative product is produced by Liuliu Orchard (Anhui): Coffee Plums. This product links a traditional Chinese snack to the currently emerging coffee culture.

This product might as well succeed in many overseas markets!