In 2025, the total national output of aquatic products exceeded 76 million mt.

The Fisheries Administration of the Ministry of Agriculture and Rural Affairs recently released the 2025 National Fisheries Economic Statistics Bulletin (hereinafter referred to as the “Communique”). According to the data, the total output of aquatic products in China in 2025 reached 76,521,400 mt, an increase of 4.00% year-on-year.

In 2025, in the face of the complex and severe situation of increasing external pressure and increasing internal difficulties, the national fishery system focused on stabilising production and supply, promoting industrial development, and promoting increasing fishermen’s income.

Value

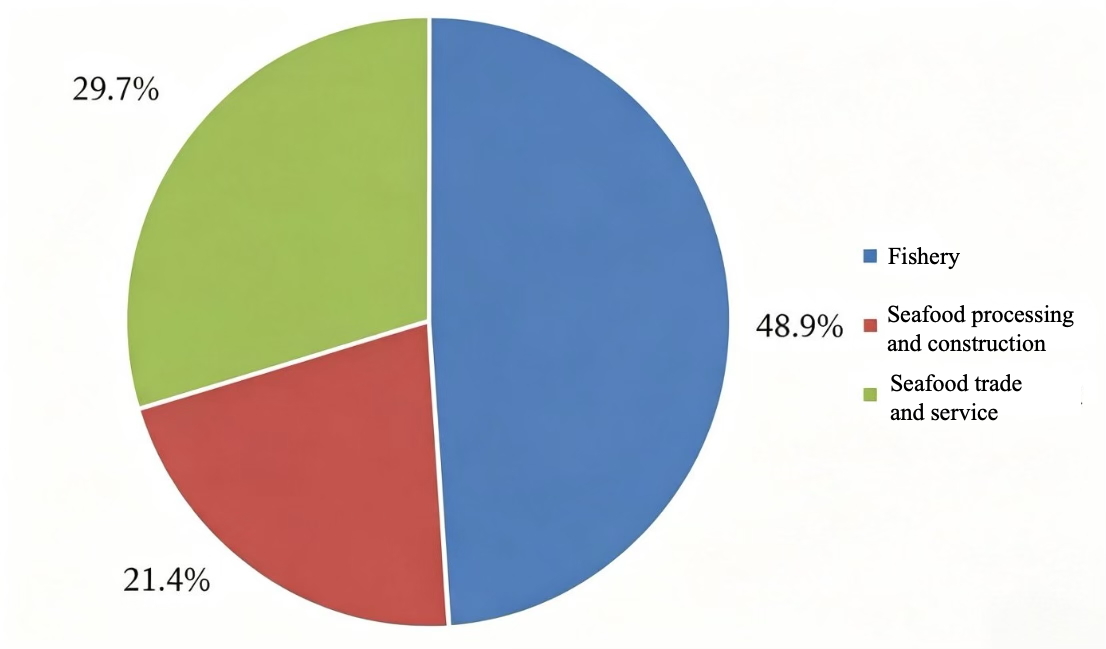

According to the communique, the total output value of the national fishery economy was RMB 3548.830 billion, of which the output value of fisheries was RMB 1735.439 billion, the output value of seafood processing and construction industry was RMB 760.608 billion, and the output value of seafood trade and service industry was RMB 1052.783 billion. Within the output value of fishery trade and service industry, the output value of leisure fisheries was RMB 106.296 billion, an increase of 7.52% year-on-year.

According to the National Bureau of Statistics, the output value of sea aquaculture was RMB 509.142 billion, the output value of marine fishing RMB 274.964 billion yuan, the output value of freshwater aquaculture RMB 919.936 billion, and the output value of freshwater fishing RMB 31.397 billion. Among the fishery output value, that of aquatic seedlings was RMB 92.462 billion.

Volume

According to the communique, in 2025, the total output of aquatic products in the country was 76,521,400 mt, of which the aquaculture output was 63,256,200 mt, an increase of 4.38% year-on-year; the fishing output was 13,265,200 mt, an increase of 2.23% year-on-year. The output of seawater products was 38,599,400 mt, an increase of 4.07% year-on-year; the output of freshwater products was 3,792,200 mt, an increase of 3.93% year-on-year.

Income

In terms of per capita net income of fishermen, in 2025, according to a survey of the income and expenditure of nearly 10,000 fishermen’s families across the country, the per capita net income of fishermen nationwide was RMB 28,676.94, an increase of RMB 1545.94 over the previous year, an increase of 5.70% year-on-year.

Area

In terms of aquaculture area, in 2025, the national aquaculture area was 7,760,600 hectares, an increase of 2.55% year-on-year. Among them, the area of seawater aquaculture was 2,408,520 hectares, an increase of 7.52% year-on-year; the area of freshwater aquaculture is 5,352,080 hectares, an increase of 0.46% year-on-year.

Foreign trade

According to the statistics of the General Administration of Customs, in 2025, China’s total import and export of aquatic products was 11,657,100 mt, an increase of 4.35% year-on-year; the total import and export was USD 45.645 billion, an increase of 4.13% year-on-year. Among them, exports amounted 4,582,400 mt, an increase of 8.11% year-on-year; with a value of USD 20,714 billion, down 0.13% year-on-year; imports were 7,074,700 mt, an increase of 2.05% year-on-year; with a value of USD 24.931 billion, an increase of 7.94% year-on-year. The trade deficit was USD 4.218 billion, an increase of USD 1.860 billion over the same period last year.

ecently, the Shenzhou 23 manned spacecraft was launched, and three astronauts took temporary residency in the Tiangong space station. This time, an astronaut will venture a one-year in-orbit stay. A one-year stay is the ultimate examination of the life support system. The relevant person in charge of the China Manned Space Engineering Office pointed out that ‘the self-sufficiency of the food system determines how far we can go in the future.’ From ‘all relying on delivery’ to ‘making and planting on the spot’, China Aerospace Food is undergoing a fundamental change.

Recipe update: high-quality experience on the tip of the tongue

In 2003, Yang Liwei completed a 21-hour space flight on Shenzhou 5. At that time, the twenty or thirty kinds of food he carried were all ready-to-eat simple meals, and a piece of coconut mooncake was a rare treat. Today, the categories of food on the space station exceed 190, and the astronaut’s meals can be different for 10 days. Mapo tofu (a spicy beancurd dish), tomatoeggs,, stir-fried lotus root, cumin potato… These home-cooked dishes with the characteristics of various regional Chinese cuisines have become the normalised meals on the space table.

‘Not only take care of full belly, but also your mood.’ According to the experts of the China Astronaut Scientific Research and Training Centre, taking Mapo Tofu as an example, the scientific research team has completely retained the original taste of the dishes: spicy, hot, fragrant and tender, after thousands of process optimisations in response to technical problems such as fragile ingredients and splashing soup in the weightless environment. Customised meals that fit the eating habits of the astronauts can effectively comfort their homesickness, when they stay in orbit for a long time.

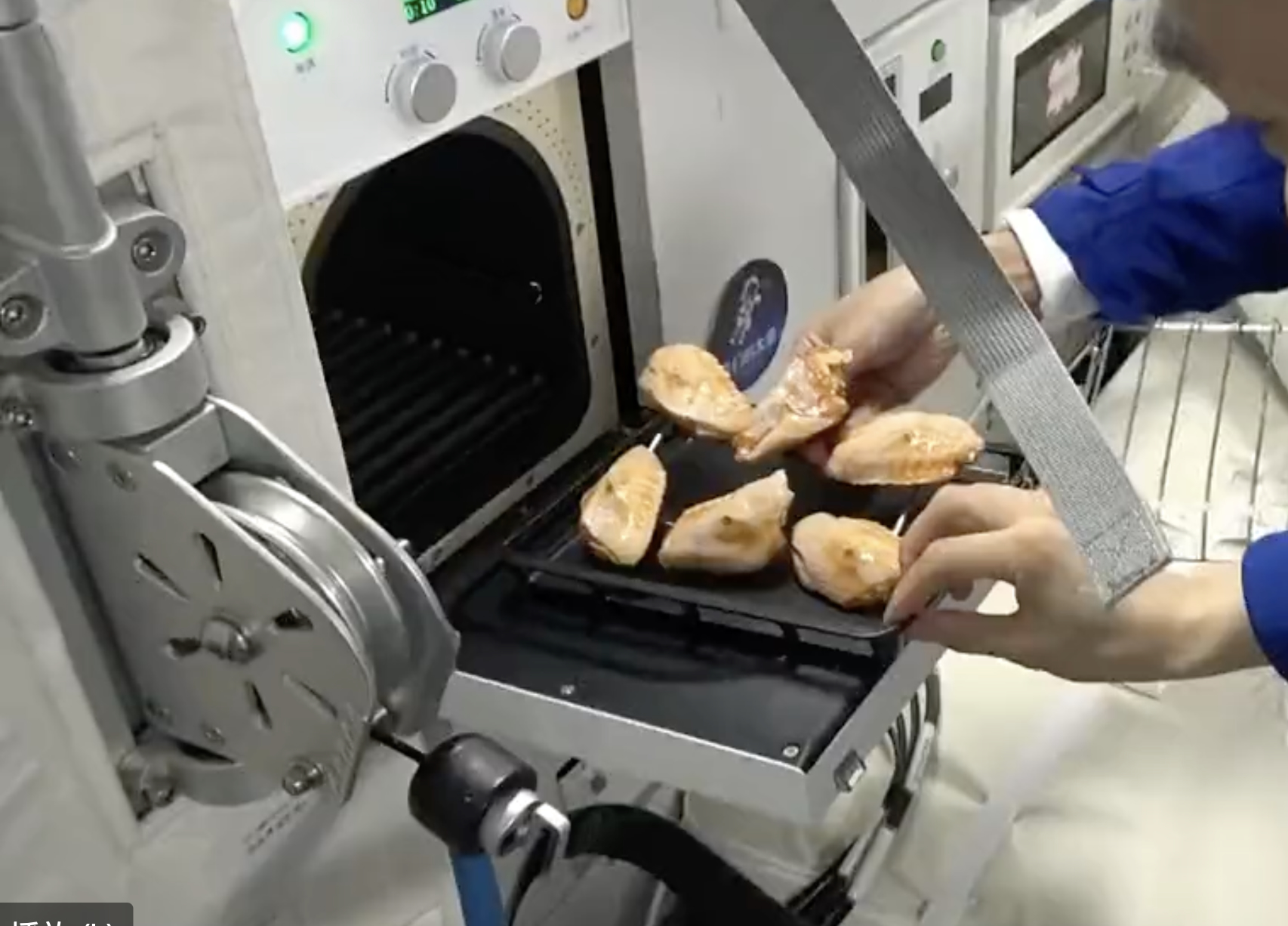

Behind this growing abundance of space catering is the breakthrough of the core equipment of aerospace cooking. In November 2025, the hot air roaster on board the Shenzhou 21 spacecraft was officially put into use on the space station. The equipment has successfully overcome a number of technical bottlenecks such as smoke purification in a closed space, drifting of ingredients in a weightless environment, and difficulty in collecting food residues. It has raised the upper limit of the heating temperature of space food from 100 degrees to 190 degrees Celsius. It can complete the production of hundreds of delicacies within 30 minutes, and work with fresh ingredients such as chicken wings and steak. Space in-situ cooking – from raw to cooked, the whole process is completed in orbit.

‘The process of baking food by hand is a kind of psychological healing in itself.’ Liu Weibo, a researcher at the China Astronaut Scientific Research and Training Centre, says that aerospace medical research has confirmed that diversified hot food supply and immersive dining experience can effectively reduce the level of cortisol in the body of astronauts and alleviate the loneliness and anxiety of long-term orbiting. For one-year long-term stay missions, high-quality experience on the tip of the tongue is not the icing on the cake, but an important support for astronaut mental health intervention.

Preparing raw ingredients in space

Packaging

In addition, space-specific food packaging technology has become a key support to ensure the safety and long-term storage of ultra-long-cycle space food.

The special meal box for astronauts equipped with the Shenzhou 23rd mission adopts multi-layer composite high-blocking special materials to build a closed structure that is almost vacuum. According to the technical information, the use of this meal box can realise the long-term storage of staple food at room temperature for three years without adding any preservatives, and adapt to the supply needs of one-year ultra-long in-orbit. At the same time, the research and development team has optimised the operation problems in the weightless environment, innovatively designed special water inlets and exhaust ports, realised the safe preparation of food inside the closed space, and completely avoided the risks of space water drift and food pollution.

It is reported that this aerospace-specific packaging technology not only serves the orbital mission of space station, but also forms a mature technical reserve, providing an important reference for the upgrading of the ground high barrier and additive-free food packaging industry.

Breeding in orbit

Advanced cooking equipment solves the problem of ‘how to do space ingredients’, and in-orbit breeding technology completely solves the core problem of deep space exploration ‘where does the grain come from’.

The space application system carries 9 scientific experimental projects through Shenzhou No. 23, including the ‘Molecular Mechanism Research on Multi-Generation Genetic Stability and Environmental Adaptive Regulation of Space Rice’ led by Zheng Huiqiong’s Team of the Centre for Excellence and Innovation in Molecular Plant Science of the Chinese Academy of Sciences. This is also the world’s first attempt to complete it in orbit. The complete growth closed-loop test of ‘seed to seed to new generation seed’.

This experiment sets up 4 cultivation units and is divided into 2 groups of control: one group carries out a reproduction experiment of rice to explore the ‘intergenerational memory’ effect of crops in the space environment and verify the adaptability of the offspring of space-selected seeds to the microgravity environment; the other group adopts the regeneration rice cultivation mode to retain the rice pile root system to achieve secondary germination and growth. , compare the growth differences and trait stability of the two breeding modes in the special environment of space.

Zheng Huiqiong said that near-earth orbits can rely on ground freight supply, but in the future, deep space exploration missions such as the moon and Mars are not sustainable to rely entirely on ground supply, and in-site grain production is a must. She acknowledged that there are still unknown challenges in in-orbit breeding at present. The impact of the space environment on crop genetic traits has not been fully clarified. Whether multi-generation breeding seed quality will deteriorate is the core topic of this experiment.

According to public data, by the end of 2025, the China Space Station has completed a total of 10 batches and 7 types of plants in orbit cultivation experiments, producing about 4.5 kilograms of fresh fruits and vegetables. Lettuce, cherry tomatoes and other crops have taken the lead in realising closed-loop cultivation in the whole growth cycle in space. This verifies the feasibility of space in-situ planting technology and accumulates key in-orbit data and technical experience for deep-space large-scale grain production.

While the space food system has achieved a leapfrog upgrade, industry experts pointed out that deep space complete food self-sufficiency still faces multiple technical barriers and needs to maintain rational research and judgement.

Genetic stability is an unknown number to be verified. The multi-generational breeding of rice in orbit is still in the stage of scientific research and experimentation, and the advantages and disadvantages of the ‘cross-generational memory’ effect generated by the special environment in space have not been decided. Once there is seed degradation, it will directly restrict the future deep space large-scale grain production.

An oven in space

Energy

Energy consumption, a multiple-choice question to be solved. High-power cooking equipment such as hot air baking machines consumes high energy, while the power resources of the space station are limited. High-power equipment operation is easy to crowd out the energy consumption of scientific experiments. The engineering team is continuously optimising the energy-saving plan to balance the electricity needs of food security and scientific research tasks.

Nutritional balance, a closed loop that has not yet closed. In the one-year ultra-long residence mode, there are limitations in the supply mode of pre-packaged food and short-term fresh fruits and vegetables, which cannot fully match the intake of trace elements of astronauts in orbit and the needs of scientific diet for a long time. The ground scientific research team needs to rely on real-time health monitoring data, dynamically optimise the nutritional formula, and continuously improve the meal security system.

Civilian use

Technological breakthroughs in the field of aerospace food are continuing to feed back the civilian market and empower the domestic food industry to improve the quality and upgrade.

In April 2025, the group standard of ‘General Technical Requirements for Aerospace Ecological Agricultural Products (Ecological Ingredients)’ was released, transforming the strict aerospace food production, cultivation and quality control standards into general norms for the civil industry for the first time, providing a reference for the high-quality upgrading of domestic agricultural products and food industries. Cui Yajuan, a researcher at the Beijing Institute of Nutritional Sources, commented that the implementation of aerospace-level standards has forced food and agricultural enterprises to upgrade their equipment, optimise management and improve quality control. With the gradual popularisation of standards, the overall quality and technical level of the domestic food industry will be comprehensively promoted.

At present, aerospace breeding agricultural products have been commercialised. Some catering enterprises in Wenzhou, Zhejiang Province took the lead in introducing space-bred eggplants, tomatoes, green peppers and other ingredients to develop specialties. After testing, the core nutritional indicators such as soluble sugar and vitamins of fruits and vegetables cultivated in space are significantly better than those of ordinary varieties.

From the 21-hour short-term flight of Shenzhou No. 5 to the one-year long-term stay of Shenzhou No. 23, behind the leap of time is the fundamental change of aerospace food from a single ‘grain transportation and supply’ to autonomous ‘grain cultivation and grain production’. Every upgrade of the space table is a powerful demonstration of China’s deep space exploration strength. Nowadays, the technology dividend of aerospace food continues to sink, from space laboratories to fields and consumer markets. This ‘table revolution’ across the world is pushing China’s food industry to fly higher and more steadily.

The dairy industry is an important industry related to the national economy and people’s livelihood, and it is also an important fulcrum for a healthy China, rural revitalisation, scientific and technological self-reliance and economic security. The Party and the state attach great importance to the development of the dairy industry. With the joint efforts of all walks of life in the industry, China has made remarkable achievements in the in-depth processing of dairy products, nutritional research and intelligent production. However, it still faces new challenges between the development mode, industrial structure and market demand. Despite facing many challenges, China’s dairy industry has been actively seeking breakthroughs and transformation. Under the overall guidance and support of the government, enterprises attach great importance to and continue to invest in technological innovation to become the core engine driving the high-quality development of China’s dairy industry. In nutrition and health, deep processing, intelligent manufacturing, biological manufacturing, green low-carbon technology Important breakthroughs have been made in art and other fields. In order to create a model of dairy product innovation and industrial upgrading, and help the high-quality development of China’s dairy industry, the China Dairy Industry Association organised industry experts to systematically sort out the top ten achievements of scientific and technological innovation in China’s dairy industry in 2025 through result collection, literature analysis, industrial research and other ways. The following is hereby released.

The exclusive strain of domestic infant matching

The early 1000 days of life is the golden window period for intestinal flora colonisation and immune system development. As the core functional substrate for the intestinal micro-ecology construction of infants and young children, probiotics have gained international consensus on their health efficacy. However, China’s infant probiotics have long faced bottlenecks such as dependence on imports of core strains and unclear targets, which has become a core shortcoming that restricts the high-quality development of China’s infant nutrition and health industry.

The National Dairy Technology Innovation Centre, together with Yili Group, carried out an independent attack and successfully isolated the infant subspecies YLGB-1496 of Bifidobacterium Chang from the breast milk of healthy mothers in China. It has been confirmed by authoritative institutions such as China Agricultural University that this strain can make efficient use of breast milk oligosaccharides (HMO), significantly reduce the incidence of eczema and respiratory infection symptoms in infants and young children, improve intestinal comfort, reduce the incidence of diarrhoea and the severity of symptoms, and effectively help the establishment and development of the immune system in early life. With solid safety and efficacy evidence such as whole genome sequencing and multi-centre clinical trials, YLGB-1496 has been officially included in the National Health Commission’s List of Bacteria Available for Infant Food.

YLGB-1496 is the first Bifidobacterium strain independently developed and approved by China. It has broken the long-term monopoly of probiotic strains for infants and young children by foreign countries, and realises the autonomy and control of the whole chain from strain screening, efficacy verification to large-scale production. The successful approval of this strain marks that China has made a key leap from “technology following” to “independent leading” in the field of infant probiotics, providing solid scientific and technological support for improving the core competitiveness of domestic infant formula milk powder and ensuring the safety of the national dairy supply chain.

Innovative application of sn-2 DHA functional lipid

Functional lipids are an important part of early nutrition of infants and young children. DHA is an indispensable key nutritional factor for the cognitive and visual development of infants and young children. However, compared with breast milk, traditional DHA mostly adopts non-sn-2 esterification form or random distribution structure, and the absorption efficiency and metabolic utilisation rate are low, which restricts the upgrading of infant brain nutrition from “component supplementation” to “structural precision nutrition”.

Junlebao and other dairy enterprises and scientific research institutes jointly tackled the situation. Based on the proprietary microbial fermentation, low-temperature extraction and physical refining technology system, they took the lead in launching high-sn-2 DHA algae oil. Sn-2 DHA accounts for as high as 50% of the total DHA ratio, which is very close to the natural distribution of DHA in breast milk. While accurately simulating the nutritional composition and proportion of DHA of breast milk, the upgrade of DHA from “content enhancement” to “structural delivery” has been realised. Compared with conventional DHA, sn-2 DHA places more emphasis on the accuracy of fatty acid location, which helps to improve the stable release and absorption and utilisation efficiency of DHA in the process of digestion. It has the comprehensive advantages of more bionic structure, more efficient absorption, more scientific formula, and more prominent industrial barriers.

The development and application of sn-2 DHA marks the important transformation of China’s functional lipid research from single nutrition enhancement to breast milk affinity structure innovation, and provides a new technical path for the high-quality development of infant formula. At present, sn-2 DHA has been applied in products such as Junlebao, Mengniu, Feihe, etc., which has improved the scientific and technological content and core competitiveness of domestic infant formula milk powder, and provided representative scientific and technological support for China’s dairy industry to move from “following the formula” to “structural innovation”.

New probiotics targeting intestinal orphan receptors

As the core functional base of nutritional and health products, the health efficacy of probiotics has become an international consensus. However, China’s core strains rely heavily on imports, and there are biosafety hazards and international trade risks. At the same time, traditional probiotics generally have bottlenecks such as unclear targets and insufficient efficacy, resulting in insufficient precise regulation of strains, which has become a difficult problem that restricts the high-quality development of the industry.

Mengniu, Yili, Junlebao, Bright, Sanyuan, Weigang and other enterprises, together with colleges and universities, have tackled the precise selection of strains and in-depth cracking of functional mechanisms. Among them, Mengniu and China Agricultural University successfully selected and obtained independent intellectual property rights from the intestines of the long-lived people in Bama, Guangxi. (CGMCC No.17827), through cooperation with top teams such as Peking University, its unique glucose-lowering mechanism was revealed for the first time: Lc19 metabolism produces a new bioactive substance – tryptophan-cholic acid (Trp-CA), which specifically activates the intestinal orphan receptor MRGPRE, and then Stimulate L cells to secrete glucagon-like peptide-1 (GLP-1) to realise the precise regulation of blood sugar homeosis. This breakthrough original achievement was published in the top international journal Cell, marking that China’s basic research in the field of food science has reached the world’s leading level.

The strain Lc19 won the “Annual Excellent Blood Sugar Health Raw Material Award” at the 9th Asian International Dairy Innovation Summit, and was successfully applied to the “Antang Shield” series of probiotic powder and milk powder and other products, which not only broke the long-term monopoly of foreign strains, but also marked the successful entry of Chinese dairy enterprises into the global “precise nutrition” innovation chain. High-value links have opened up a new development path for the industry based on local scientific research and serving the world.

The first GOSS system to realise the flexible production of milk ingredients

Deep processing is the key engine that drives the value of raw milk to jump. Its core lies in the efficient separation and high-value utilisation of milk source materials. However, the traditional milk source ingredient production line mostly focusses on the extraction and separation of a single group, and there are common pain points such as low raw milk utilisation rate, high production line switching cost, lack of flexible production capacity and difficulty in adapting to diversified market demand.

The first GOSS system (non-destructive orderly analysis system) in the Mongolian milk industry realises the orderly separation of core milk-based raw materials such as milk fats, milk proteins and whey, so that the value of raw milk is increased by more than 3 times. While improving the extraction efficiency, the nutritional value of active substances is preserved to the greatest extent. Relying on this core technology, Mengniu has independently designed and built 7 industry-leading “milk cube” flexible co-line production lines, which can process 600 tons of raw milk per day and can flexibly switch between a variety of products such as lactoferrin, desalted whey and miceller casein, completely breaking the long-term limitation of deep processing in the domestic dairy industry to a single product model. The barrier has realised the leap from “single-line single product” to “multi-category flexible common line”. The key performance and quality of the prepared products meet the national standards: the purity of lactoferrin is more than 95%, and the desalination rate of D90 desalination whey powder exceeds 90%. At present, the achievement is not only applied to the fields of healthy food such as early nutrition, sports nutrition and clinical nutrition, but also extended to new track products such as milk tea base milk. This breakthrough not only provides key core technical support for the transformation and upgrading of dairy deep processing to flexibility, high efficiency and diversification, but also provides an independent and controllable localisation solution for the quality and efficiency improvement of dairy deep processing.

High-efficiency active extraction technology of milk protein

Milk protein is a key substrate for infant formula milk powder, sports nutrition, special medical food and functional nutrition products for middle-aged and elderly people. However, China’s milk protein raw materials have long had the problem of high external dependence and insufficient independent supply capacity. Restricted by the core technology systems such as high activity maintenance, natural structural integrity protection and high-efficiency extraction, it has not been completely broken through, and industrial development is facing a serious “stuck neck” dilemma.

Based on independent innovation, Feihe took the lead in overcoming the problem of milk protein extraction and separation. It has independently developed three international leading technologies of milk protein chromatography ultrafiltration extraction, fresh active low-temperature separation and directional enzymatic lysis, and achieved a technological breakthrough in the direct extraction of highly active protein from raw cow’s milk. Among them, the extraction rate of lactoferrin extracted by chromatography ultrafiltration technology reaches 95%, and the whole process of low-temperature technology effectively protects the natural active structure of protein. Based on these three core technologies, the enterprise has built five large-scale production lines, covering the preparation of ten core raw materials such as lactoferrin, desalted whey and hydrolysed milk protein, and promoted the autonomy rate of infant formula milk powder raw materials from 50% to more than 90%.

In terms of product quality, the purity of lactoferrin has reached more than 97%, and the desalination rate of whey has reached more than 90%. All indicators have reached EU standards, which has strongly promoted the reduction of domestic dependence on desalted whey imports from 70% to less than 40%, which has significantly alleviated the pressure of import dependence. At present, Feihe has laid out milk protein raw material factories in the three golden milk source belts of Inner Mongolia, Heilongjiang and Ningsia, with a total of 3,000 tons of fresh milk per day. It is committed to building a global supply base, realising the independent production and localisation substitution of milk protein core raw materials, and making China’s dairy industry safer and supply chain stable. And the autonomous controllable of high-end functional raw materials provides a solid guarantee.

Platform operation and quality safety through AI

Under the background of the deep integration of digital technology and the real economy, AI technology is profoundly reshaping the production mode of the dairy industry. The dairy industry chain is long and has many links. The traditional carbon management model faces efficiency bottlenecks such as long accounting cycle, many data islands, and difficult to reduce carbon together. In the field of quality and safety, the traditional microbial detection cycle is as long as 2-3 days, and the traceability response is slow, and it is difficult to achieve prior prevention and real-time control.

Yili Group launched the first digital carbon management and operation platform for the whole industry chain in China’s dairy industry. With the whole life cycle carbon accounting, dynamic monitoring, intelligent decision-making and collaborative carbon reduction as the core, it builds a closed-loop system covering agriculture and animal husbandry, processing, logistics packaging, consumption and waste treatment, integrating “carbon footprint + water footprint” collaborative management, and also It takes into account the needs of large, medium and small dairy enterprises, and has the value of cross-industry and cross-regional promotion. Feihe has successfully built an automated rapid detection platform for pathogenic microorganisms, a “raw material-grade dairy industry chain traceability system” and a “near-infrared AI intelligent pupil full-link millisecond quality inspection equipment system”, which has pushed quality control to a new height of “second-level response, raw material traceability, millisecond detection”, and the traditional 2-3-day microbial screening Shortened to 30 seconds; relying on deep learning and million-level spectrum library, more than 10 indicators of the whole process of milk powder are monitored online at the millisecond level, and process parameters can be regulated in real time.

Relying on the digital carbon management and operation platform, the carbon accounting cycle is compressed from 2-3 months to 15-20 days, the efficiency is tripled, and the annual cost is about 5 million yuan, which truly realises the synergy of environmental, economic and social benefits. The product quality and safety control mode has changed from “post-disposal” to “pre-prevention”, which greatly reduces the risk of food safety. AI technology promotes the dairy industry from single-point optimisation to the whole industrial chain, helping enterprises achieve a balance between business value and social responsibility, and providing a standard paradigm for the sustainable development of the industry.

Autonomous and controllable dairy filling

Sterile carton filling is the core link of dairy manufacturing, but China’s high-end equipment has long relied on imports. There are problems such as high price, production line curing, long change cycle, high energy consumption, hydrogen peroxide residual risk and low degree of intelligence, and it is difficult to achieve global optimisation.

Hangzhou Zhongya Machinery Co., Ltd. has conquered the high-efficiency sterilisation technology of tunnel-type multi-warehouse online blanks. Through the sequential transmission of tunnel-type preheating gasisation warehouse, sterilisation warehouse, waste discharge warehouse and bottle blank moulding heating process, the online bottle blank low-energy and high-efficiency sterilisation process is realised, and it is equipped with PDMS cloud intelligent operation. The maintenance system realises remote diagnosis and digital management, and the energy efficiency of equipment is improved by 35%. Old modules can be recycled across industries to realise full-cycle green manufacturing. In response to the problems of production line curing, long change cycle, and difficult to meet the needs of small batches and multi-variety, Hangzhou Central Asia Machinery Co., Ltd. has broken through the flexible filling synchronous switching technology to realise 200-1250 ml full-capacity one-click switching production; Shandong Bihai Packaging Material Co., Ltd. has broken through flexible manufacturing and intelligent control. Manufacturing technology, research and development of multi-module compatible moulding system, to realise the seamless switching of brick bags, diamond bags and other packaging types within 30 seconds, and a single equipment can complete the multi-category production of the past 3 special lines.

The BFCA fully automatic high-speed flexible multi-functional sterile bottle blowing filling and capping integrated production line of Hangzhou Central Asia Machinery Co., Ltd. has been identified by the expert group organised by the Zhejiang Packaging Federation. The overall technical level is at the international advanced level. The relevant equipment has been applied to dairy enterprises such as Yili; Shandong Bihai Packaging Material Co., Ltd. The price of the product is only 1/2 to 2/3 of the same kind abroad. It has been applied to enterprises such as Mengniu and exported to more than 40 countries and regions such as India. China’s high-end dairy equipment has truly realised the coordinated improvement of production line efficiency, green manufacturing and economic benefits, providing a replicable scientific and technological paradigm for the independent controllability of dairy packaging equipment and the sustainable development of the industry.

Sterile packaging

In the field of sterile packaging, the 250-ml peak drill bag type and supporting filling equipment and capping equipment have long relied on imports, resulting in high equipment investment, high maintenance cost and poor flexibility when domestic dairy enterprises launch high-end normal temperature yoghurt, vegetable protein drinks and other products. Traditional bottle caps also have problems such as large opening torque, insufficient sealing, and high plastic usage, which makes it difficult to take into account consumer experience and environmental protection requirements.

Fanmei Packaging (Shandong) Co., Ltd. has leaped from a packaging material supplier to a “equipment + packaging material + service” integrated solution provider. It independently developed a 250ml peak drilling filling machine, breaking the international monopoly of dream cover and 250 peak drilling bag type. In response to the pain points of traditional bottle caps, the innovative cover body “Fanxiang Cap” is launched, which adopts a one-step low-torque large spiral design to reduce the opening force by 50%; it adopts a double-step small-calibre bottle mouth to solve the sealing problem and take into account the release of flavour; the “small barrel edge” base design is adopted to save plastic usage and improve the fitting stability. , the cover body works seamlessly with the filling machine and the capping machine to realise the autonomous control of the full link of “cover-material-machine”.

The high-end sterile packaging and filling solution independently developed by Fanmei Packaging (Shandong) Co., Ltd. provides dairy enterprises with a lower cost, faster response and more flexible technical path. Its plastic reduction design and green technology run through the whole life cycle of the product, practising the concept of environmental protection. This series of products has been widely used in domestic dairy leaders such as Yili and Mengniu, with a market share of more than 13% in liquid milk, and has been successfully sold to France, Germany and other countries. China’s high-end dairy equipment has truly realised the coordinated improvement of cost control, flexible response and green manufacturing, providing a replicable successful paradigm for the industry’s independent, efficient and green high-end packaging overall solution.

Functional sugar manufacturing

In order to realise the scientific sugar reduction of processed food, Action for Healthy China (2019-2030) advocates that food enterprises use functional sugar to replace sucrose. The new generation of functional sugar represented by tag sugar plays an important role in the food industry and health management with its pure taste close to sucrose, extremely low calories, regulating intestinal health, low glycetic index and other physiological functions. However, although the sugar was approved as a new food raw material in 2014, it has been monopolised by a few countries for a long time because of its high-efficiency biotransformation and separation and purification technology and key enzyme preparations, and the cost is high, which seriously restricts its wide application.

China’s scientific research units and enterprises have worked together to overcome the problems of enzyme preparation, biotransformation and high-purity crystalisation, and achieved a breakthrough of lactose and starch dual routes: the lactose route has built China’s first fully automated production line through enzyme-oriented evolution and double enzyme co-expression; starch route uses multi-enzyme molecular machine technology, and the conversion rate exceeds 6 0%, the pilot has been completed, the product purity has reached more than 99%, and an independent intellectual property production system has been built, and the cost has been reduced by about 60%. Tag sugar can significantly improve the sweetness quality and texture stability of yoghurt, give milk drinks a refreshing and smooth taste, and provide a healthy low-sugar label for formula milk powder. More importantly, its functional attributes such as regulating blood sugar and helping intestinal health have greatly broadened the development boundaries of functional dairy products.

This breakthrough marks that China has broken down international technical barriers in the field of new functional sugars, realised the localisation of the whole chain from core enzyme preparations to industrial mass production, and provided a new low-sugar option for yoghurt, milk drinks and high-end formula milk powder. From a cup of yoghurt to a can of high-end milk powder, the domestic application of Tag sugar is a strong witness that China’s dairy industry relies on independent innovation, masters core technologies, and leads the healthy upgrading of global dairy products.

Green low-carbon technology

From the “dual carbon” goal to the “15th Five-Year Plan” planning proposal, the construction of an agricultural industry system with green and low-carbon circular development is emphasised. However, the long industrial chain of the dairy industry, the dispersion of carbon emissions, the low coverage rate of the three-scope accounting, the poor connection of the breeding cycle, and the lack of carbon management standards, etc., restrict the green transformation of the industry.

In response to accounting and standard issues, Yili has launched a carbon management and operation platform, which has built a closed-loop system covering upstream agriculture and animal husbandry, production and processing, logistics and packaging, consumption and waste treatment, integrating the collaborative management of “carbon footprint + water footprint”, to achieve 100% full coverage of factories across the country, and strongly support the accurate amount of carbon emissions in the supply chain. Chemical. In response to the problem of poor connection of the breeding cycle, Mengniu has built a whole-chain green low-carbon technology system, forming a cycle model of “fort planting – dairy farming – cow dung biogas power generation – swamp fertiliser return to the field”, and cooperated with the resource utilisation of 100% manure of pasture; built 41 national green factories, 4 zero-carbon factories, and launched Tren Su Desert organic pure milk and other green products; practising the 4R1D green packaging strategy, PHA marine degradable straws are applied for the first time in China.

There are 154 members of the Yili Zero Carbon Alliance, and the carbon emission intensity per ton of products in 2025 will be 65% lower than that of the 2012 benchmark year. Mengniu has been selected as the Enterprise Carbon Neutrality Path Map of the United Nations Global Compact for its desert organic pasture practice. It has won the highest AA rating in the MSCI ESG (Environment, Social and Governance) industry for three consecutive years, and has been selected as the S&P Global Sustainable Development Yearbook for two consecutive years. The whole-chain green low-carbon technology system provides a system solution that can be popularised for the green and low-carbon transformation of the dairy industry.

Look ahead

Looking forward to 2026 and beyond, in order to accelerate the development of new quality productivity in the dairy industry and promote industrial upgrading, it still needs government guidance, enterprise-led, scientific and technological support, market-driven and other multi-party cooperation to strengthen top-level design, increase R&D investment and collaborative innovation, build an integrated innovation ecology, and promote scientific and technological innovation and industrial development. Show in-depth integration, improve national health, and realise the transformation from a “dairy powerhouse” to a “dairty powerhouse”. It is expected that dairy industry colleagues will continue to adhere to the concept of scientific and technological innovation to lead the industry development, increase scientific and technological investment, focus on the direction of “efficient production, precise nutrition, green low-carbon, intelligent manufacturing”, and form a technological breakthrough of the whole industrial chain: tackle active protection and flavour regulation at the raw material end, and improve the nutritional quality of products; push the processing end Dynamic and precise sterilisation and nutrition customisation, and develop functional products for different groups of people; the deep processing end breaks through the high-value extraction technology, realises the full-component utilisation of raw milk, and reduces import dependence; the manufacturing end improves the localisation rate of intelligence and equipment, and integrates AI and digital twins; at the same time, it tackles low-carbon breeding and environmental protection packaging, and helps the “dual carbon “The goal. Synthetic biology is accelerating its industrialisation, which is expected to bring about subversive changes in breast milk oligosaccharides, lactoferrin and other fields. Driven by policy and science and technology, China’s dairy industry is moving towards a higher quality, safer and more sustainable future.

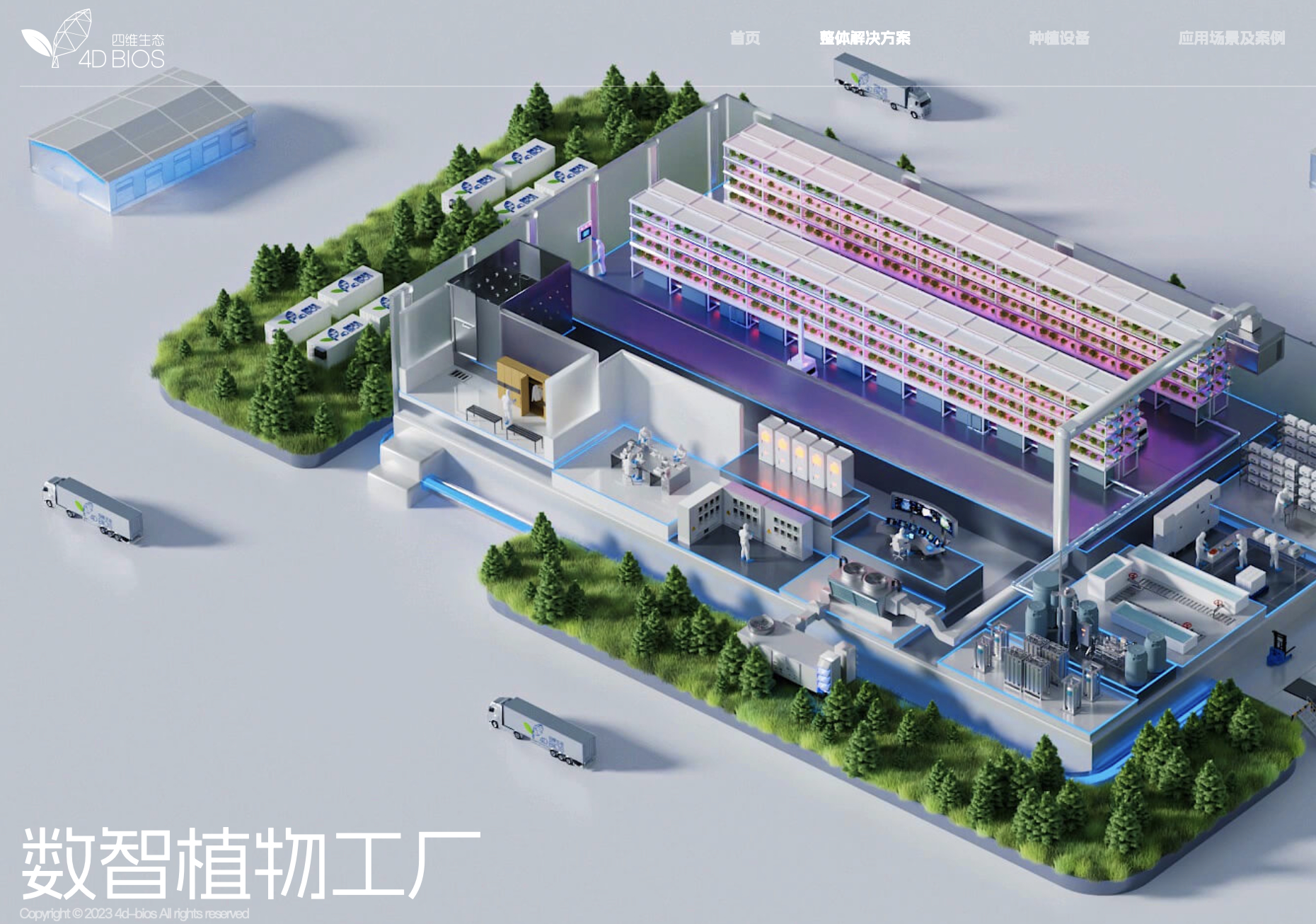

Plant factory is an advanced stage of the development in agricultural production on an industrial scale. It is a high-input, high-tech and well-equipped production system. It integrates biotechnology, engineering and system management, so that agricultural production can be freed from the shackles of the whims of nature. A factory-based agricultural system enables a government to plan fruit and vegetable production with a precision close to that of other industries.

In recent years, the overall market size of China’s plant factory industry has shown an upward trend. In 2025, the market value of China’s plant factory business was RMB 2.248 billion, an increase of 13.8% year-on-year.

Foto’s of Pulante in Hebei province

In addition to being affected by national policies, this development is also inseparable from technological innovation. The deep integration of the Internet of Things, artificial intelligence and automation has realised a high-precision coordinated regulation of the planting environment and the unmanned operation of the whole process, which has greatly improved the consistency of production efficiency and product quality, and strongly promoted the continuous growth of the industry.

In terms of demand, the improvement of health awareness has promoted consumers’ preference for agricultural residue-free, zero-pollution and high-fresh agricultural products, and the closed production and traceable product attributes of plant factories accurately match this consumption trend.

Hengtong Ecological Agriculture Technology Development Co. (Jilin) has produced 300 mt of cherry tomatoes in 2025.

Overview of the plant factory industry

The plant factory is an efficient agricultural system that realises the annual continuous production of crops through high-precision environmental control in the facility. It uses computers and electronic sensing systems to automatically control the temperature, humidity, light, CO2 concentration and nutrient solution and other environmental conditions of plant growth.

According to different divisions, plant factories can be divided into the following categories: according to the construction scale, they can be divided into large (more than 5000m), medium-sized (1000~5000m), small (100~1000m), and micro (less than 100m).

According to the production function, they can be divided into plant seedling factories, leafy vegetables, melons and fruits, flower plant factories, as well as some field crops, medicinal plants, edible fungi, etc..

In terms of the organisational scale of production and research objects, plant factories can be divided into plant production plant factories, group culture plant factories, cell production plant factories (photobioreactors).

According to light energy The utilisation method can be divided into three types, namely solar light utilisation plant factories, all-artificial light utilisation plant factories, and comprehensive plant factories that combine sunlight and artificial light.

A design by 4D-Bios in Hangzhou, specialised in vertical farming

China

In recent years, the Chinese government has introduced a number of policies to actively promote the development of plant factories.

For example, in June 2023, the ‘Guidance on the Development of Modern Facility Agriculture’ issued by the Ministry of Agriculture and Rural Affairs proposed to support the development of connected greenhouses, plant factories and other advanced production facilities around large and medium-sized cities according to local conditions, strengthen demonstration and guidance, and improve the stable production and supply of fresh agricultural products such as vegetables.

In September 2024, in the ‘Opinions on Practising the Concept of Big Food and Building a Diversified Food Supply System‘ issued by the General Office of the State Council, it is proposed to actively develop daylight greenhouses and plastic greenhouses, promote the transformation and upgrading of old facilities, accelerate the development of intensive seedling breeding, and develop soilless cultivation such as matrix and hydroponics. Plant factories are built around the city.

In April 2025, in the ‘Plan to Accelerate the Construction of a Strong Agricultural Country (2024-2035)’ issued by the Central Committee of the Communist Party of China and the State Council, it is proposed to implement the modernisation of facilities and agriculture, build modern cultivation facilities with standards, advanced equipment and high output, and develop new forms such as agricultural factories.

Sure, regular readers of these pages are completely aware that the natural flavour of milk does not agree with the average Chinese palate. And this continues to clash with the position of dairy products in the top layer of the Chinese nutrition pyramid.

I have introduced yoghurt and ice cream with peculiar flavours that are more in line with traditional flavour patterns of the Chinese, to mask the ‘creamy’ flavour of milk. In this post, I will introduce dairy products flavoured according to entire classic Chinese dishes, as available in China at the date of this post. Most of these are not produced by the large national dairy giants like Yili or Mengniu, but by regional or local companies.

White sliced chicken

Screenshot

White sliced chicken, baiqieji, is a classic starter in Cantonese cuisine. It is chicken cooked in a broth with ginger and scallions, served cold to be dipped in soy sauce. Yuexiu Dairy is producing a ‘ginger scallion white sliced chicken milk’. A cool looking chicken is showing a glass of the milk alongside the original dish.

Halal milk

Screenshot

Xiajin Dairy is the largest dairy processor of Ningxia province. It is a region with a large Muslim population, so Xiajin is offering a range of beef and mutton flavoured milks. An salient detail: the middle product is a mutton flavoured cow milk.

Tomato

Screenshot

Chinese like to eat sliced tomatoes with a little sugar as a snack or starter. Jiabao from Guangdong is offering sugared tomato milk.

Dim sum

Screenshot

Dim sum, a table full of small plates with savoury delicacies is a favourite lunch in Guangdong province. Chenguang Dairy from Shenzhen has developed a series of milks mimicking some favourite dim sum.

Whenever I run across new exciting flavours, I will add them here. However, tasting all the above products will keep you busy for a while.

Black sesame has always been a frequently used ingredient in Chinese desserts. The top product probably is the tangyuan, a glutinous rice ball with a sweet filling. There are several types of fillings, but black sesame is the first choice. I am showing a sugar-free version from Jietang Mudashu, which literally means: ‘weaning from sugar Uncle Mu’. This long brand name stresses how hard Chinese are struggling with their sugar addiction.

Since Guangdong Zhuang’s Sesame Milk became popular, black sesame, a traditional ingredient, has also ushered in a new life in the Chinese baking industry. By 2025, the scale of China’s baking market has reached RMB 100 billion, and the combination with the concept of the same origin of medicinal food is opening up new growth space for it.

Black Sesame Milk

Nowadays, black sesame has changed from a limited flavour to a ‘star ingredient’ in the baking, dairy and confectionery industries. From the continuous popularity of black sesame cakes and bread, to the ‘Chinese medicine pharmacy style’ baking on social networks, it is no longer just a food from past memories, but has gained a popular role in baking innovation with both health and flavour.

How black sesame turned hot

It is no coincidence that black sesame is popular in the baking industry. Under the joint embrace of all circles of society, black sesame has gradually risen from the corner of the supermarket shelves to the C position of the bakery shops. In 2025, the scale of China’s ‘food as medicine’ market has exceeded RMB 370 billion, and the valuation of the whole industry chain will exceed RMB 2 trillion.

This trend has directly promoted the upgrading of the entire black sesame industry. In recent years, the National Health Commission has accelerated the expansion of the ‘food as medicine’ catalogue, which now covers 106 kinds of food substances. In 2025, the government proposed to simplify the identification process and shorten the cycle to inject new momentum into the development of the industry.

Black Sesame Pastry

The transformation of consumer demand is equally crucial. The data of Internet platforms like Meituan and Xiaohongshu confirm this trend: 72% of the post-90s generation have replaced traditional health care products with functional snacks, and the number of readings on the topic of ‘health snacks’ on Xiaohongshu has exceeded 800 million.

Young consumers have shown a strong interest in the modern expression of traditional health wisdom, transforming black sesame from a simple ‘food for the elderly’ to a synonym for fashion and health.

The transformation of black sesame, which traditionally exists in the form of paste, has experienced a texture leap from liquid to solid in modern baking.

Innovative applications such as black sesame thousand-layer cake, black sesame rock sauce, black sesame sweet potato, black sesame raw filling, etc. have emerged one after another.

The leap of aesthetic style also adds bricks to the popularity of black sesame. The natural dark gray colour of black sesame perfectly fits the ‘new Chinese aesthetics’ and ‘minimal industrial style’. In boutique bakeries in New York and London, black sesame is often combined with miso and sea salt to form a visual style called ‘Charcoal Aesthetic’.

Charcoal Aesthetic is an emerging design and marketing concept in contemporary consumer culture, especially in the fields of baking and beverages. It does not refer to the artistic creation using charcoal pens, but refers to a visual style and product aesthetics with deep, high-grade black or charcoal gray as the core, emphasising natural, rustic, textured and mysterious.

For example, Onion, a Korean Internet celebrity bakery, specialises in looking for old houses with a sense of age. The cement decoration style is popular with young consumers.

The research of the Institute of Oil Crops of the Chinese Academy of Agricultural Sciences reveals the scientific basis of black sesame flavour: sesame food contains 187 flavour compounds with aroma contributions, and its rich aroma and unique taste are addictive.

At present, a variety of black sesame hot products have emerged on the market:

Holiland Black Sesame Five Black Crisps triggered a rush to buy as soon as it was launched.

Master Nanyang’s black sesame chicken cake has become a popular new product, and some stores have sold more than 100 copies in a week.

Five black mulberry buns developed by Fu’e Baking (Chongqing), black sesame + black beans + black rice stir-fried and ground flour, add dough with whole wheat flour, fragrant!

In the tea industry, this ‘black whirlwind’ is equally strong. Luckin Coffee launched the winter solstice limited ‘five black’ latte, Chabaidao upgraded the classic version of soy milk to the black sesame soy milk, and M Stand (a coffee chain) simultaneously launched Black Sesame Milk and black Sesame Cheesecake.

Heaven Chosen Material

The reason why black sesame could become a ‘chosen material’ lies in the perfect superposition of its triple attributes, which together constitute its irreplaceable competitive advantage in the current market environment.

Nanyang’s Black Sesame Chicken Cake

The obsession of ‘anti-hair loss’ engraved in the DNA of Chinese people: In the oriental context, black sesame has a strong association with ‘black hair, kidney tonic’. According to research data, the subconscious driving force of 85% of Generation Z consumers buying black sesame products is anxiety over hair loss. It is this profound cultural psychology that significantly reduces the brand’s market education cost.

And compared with white sesame, the nutritional performance of black sesame is more convincing. Its calcium content is about 7 – 8 times that of milk. At the same time, it is rich in melanin and lignin, which has strong antioxidant properties.

Black sesame also has the characteristics of ‘scent without grabbing space’. It can be perfectly compatible with the bitterness of matcha, the mellowness of chocolate, and the sweetness of sweet potato, and its high oil content can naturally improve the moisture and aroma thickness of baked goods. A study by the Chinese Academy of Agricultural Sciences shows that natural polyphenols in sesame seeds can enhance the stability of food flavour, which is very important for processing and storage.

Black sesame is more than black

The next step of black sesame baking will be internationalisation, which has begun to emerge in China and global markets.

The trend towards globalisation is obvious. Black sesame is becoming the ‘new matcha’ in the coffee chain business. In 2025, the overall demand for ‘black sesame’ in the United States increased by nearly 30% year-on-year, the highest in history. In Seoul and Tokyo, black sesame latte has become a resident variety of cafes, while in the United States, there are many coffee shops serving ‘black sesame latte’, which has the momentum to catch up with ‘matcha latte’.

Honeymoon Dessert (Manji tianpin) launched a black sesame milk early 2026

Black sesame candy

Yilümai Food (Xiamen) has developed a Black Sesame Gorgon Nut Walnut Candy. It is a chewy type of candy with a slightly sweet earthy sesame taste. The chunks of walnuts accentuate the earthy flavour. The gorgon nut is the seed of a type of water lily. Ingredients:

The continuous increase in recognition of domestic baking ingredients among Chinese consumers has also created favourable conditions for local black sesame products. According to the survey, 56.2% of consumers believe that domestic raw materials ‘can replace’ or ‘completely replace’ imported raw materials in most cases.

The global sesame market was expected to reach USD 12.511 billion in 2025 and grow to USD 15.832 billion in 2032. Black sesame is expected to become a new generation of popular flavours in 2026, becoming a regular in desserts, drinks and health topics.

China is not only the world’s largest ice cream market, but I have also reported on innovative ice cream from China in several posts. One post concentrated on savoury flavours, like chili ice cream. Another introduced funky ice cream, like one shaped as the tail of a fish (or perhaps a mermaid?).

Here are some of the latest inventions launched recently by the Lawson’s chain of convenience stores in China.

French fries ice cream, complete with tomato sauce (actually strawberry).

The same company has also launched an ice cream version of the hamburger.

Less funky, but surely the most ingenious is the peach shaped ice cream. It is almost a shame putting your teeth in it. An interesting detail: the Chinese name of this product is taoqi, literally: ‘peach spirit’. However, it is homophonous to taoqi with different characters, which means ‘naughty’.

It’s well known that China is the biggest coffee market in the world. And if you’ve been following this blog, you might recall my stories about new coffee experiences in China, like coffee cocktails, ready-to-drink coffee and dirty coffee.

During my recent trips, I met even more coffee innovators, so I thought I’d share some of the latest trends in a new blog post.

Coffee and tea: a perfect pair

Even though coffee is becoming super popular in China, it’s not really replacing tea as the national drink. Tea is still the top choice. But to be more accurate, coffee is just becoming a new kind of tea in Chinese tea culture. The Pu’er region in Yunnan province was the first place I saw coffee and tea blending together.

In October 2025, we took a tour around Jingdezhen, China’s ceramics capital in Jiangxi province. This area is also famous for its tea. But we had a really interesting coffee experience in a small village called Hanxi, where an entrepreneur had opened a fancy coffee shop right in the middle of the tea fields.

Besides the usual coffee drinks like espresso and americano, they also made coffee mixes with tea and other ingredients. We tried two special drinks: Apple by the Window and Pine Grove in Tea Field. They weren’t quite to our taste. They tasted mostly like coffee, but the tea flavour was hard to spot. The apple in the first one didn’t really go well with the coffee. The pastries were good, and the view of the endless tea fields was amazing. We chatted with the manager, who told us they’re planning to make even more variations and might even add Chinese wines. She had just come back from a trip to the wine region of Ningxia.

Coffee and wine: a bold combination

I came across this on Chinese social media about a visit to the Torch Coffee Farm in Pu’er, Yunnan. Torch Farm is experimenting with different coffee bean varieties, like roasting methods, to create unique flavours. The illustration shows some of their coffees during a tasting session, which is part of the tour. To me, the Merlot variety stands out the most. Torch Farm people compare coffee flavour variations to wine grapes. Interestingly, Pu’er has a sister city relationship with Libourne in the Bordeaux region of France. This was because tea experts in Pu’er noticed similar differences between tea and wine grapes.

These are fascinating developments that blend food science, business and culture. I’m sure I’ll be back soon with another post on this topic.

Picles and coffee: a peculiar couple

A company in Shantou (Guangdong) has launched an extremely funky drink, combining coffee (milk) tea and several other ingredients including pickled vegetables, in 2024. This concoction redefines the expression ‘an acquired taste’. However, a sales point was reported in Beijing in February 2026. So, apparently has developed a certain clientele.

The 22nd Annual Meeting of the Chinese Society of Food Science and Technology was held in Guangzhou October 2025. Through conference reports, special seminars, display of achievements, theses, other forms, this annual conference promoted the cross-integration of food science, accelerated the transformation and application of scientific and technological innovation achievements, built a high-quality food science and technology talent echelon, strengthened the integration and innovation of science and technology and industry for the food industry.

The remainder of this item provides summaries of the various forums and seminars of the Conference.

Hot Issues Forum:

The 2025 Food Science Frontier Hot Issues Forum focussed on the most forward-looking research direction in the field of food science. From new resource mining, nanobiology, precise nutrition, immune regulation, digital intelligence to intelligent materials, it presents a high-density and high-quality ideological collision, clearly outlining the cross-integration of food science. The way to break through with innovation.

Professor Mao Xiangchao, dean of the School of Food Science and Engineering of Ocean University of China, introduced the great development potential of marine carbohydrates, as well as the team’s discovery, functional analysis and high-value utilisation of new marine polysaccharide structures such as duckweed starch and microalgae starch in the report of new carbohydrate resources. Breakthrough research progress has been made in terms of use, pointing out that the need for resources from the ocean is one of the key paths to meet the challenges of sustainable food supply in the future.

Professor Fang Yapeng, dean of the School of Health Science and Engineering of Shanghai University of Technology, brought a report entitled “Intracellular Biological Effects of Food-based Nanoparticles”. Through the close intersection of food science with nanobiology and cell biology, we explore the interaction mechanism between natural food-genic nanoparticles such as lipids, starch and proteins and cells. He emphasised that paying attention to the biological effects of food nanoscale is of milestone significance for a comprehensive understanding of the deep mechanism and safety assessment of the health effects of food components.

Professor Chen Hongbing of the Sino-German Joint Research Institute of Nanchang University focusses on the increasingly serious global food allergy problem and shares the latest research results of “the immune regulation role of active polysaccharides in the prevention and treatment of food allergies”. Chen Hongbing’s team discovered and verified the specific structure of polysaccharides, such as sea cucumber polysaccharide, aloe vera polysaccharide, etc., by regulating the intestinal flora-immune axis, reshaping the Th1/Th2 balance and inducing Treg cells, thus effectively alleviating food allergy reactions. This study provides a new theoretical basis and practical strategy for the development of natural immunomodulators based on dietary polysaccharides and the realisation of nutritional intervention for food allergies.

Professor Xu Yong, director of the Oil and Plant Protein Research Centre of the School of Food of Jiangnan University, looked forward to the “development and challenges of digital intelligence of oils and fats in the future”. Driven by big data, artificial intelligence and advanced sensor technology, grease from molecular design, precision processing, customised nutrition to intelligent control of the whole industry chain is the key to solving the core challenges of efficiency, sustainability and personalised needs faced by the oil industry.

The report of Professor Guo Zhiming of the School of Food and Biological Engineering of Jiangsu University, “Research Progress on Intelligent Packaging Indication of Fruit and Vegetable Multifunctional Response Nanomaterials”, introduced the intelligent nanomaterials developed by the team that can produce sensitive colour or signal response to specific gases, temperature or microbial changes released during the corruption of fruits and vegetables. These “intelligent packaging” can monitor the freshness of food in real time and without damage, greatly improving the safety of food quality and security and the intelligence level of the supply chain.

Professor Tian Jinhu, vice dean of the Central Plains Research Institute of Zhejiang University, shared the “structural design and application research of pH-responsive EGCG-metal self-assembly ‘phenol cage’ as a long-term delivery carrier of insulin”. The study uses the self-assembly behaviour of EGCG and metal ions to construct a nanocarrier with a “cage-like” structure, which can effectively envelop insulin and intelligently release it in a specific pH environment, providing potential new materials for oral long-acting drug administration in patients with chronic diseases such as diabetes.

Professor Sun Na’s report of the School of Food of Dalian University of Technology “Research on the Risk Assessment and Blocking of Cell Cultured Fish Sensitisation” confronts the potential risks and safety problems in this emerging field and explores effective strategies for cultivating fish sensitisation through processing technology or formulas to adjust the sensitisation of blocking cells.

Jia Longgang, a young teacher of the School of Food Science and Engineering of Tianjin University of Science and Technology, reported “From the atmosphere to the intestine: a two-way pathway for PM2.5 aggravation and probiotics to relieve neurodegenerative diseases”, revealing PM2.5 by building a complete pathway from environmental exposure to intestinal flora disorder and then to central nerve inflammation. How to “enter the brain” to aggravate neurodegenerative lesions, and it has been verified that specific probiotics can effectively inhibit this negative pathway by repairing the intestinal barrier and regulating flora metabolites. This research combines environmental science, neuroscience and food microbiology to open up a new perspective for nutrition intervention in environmental-related diseases.

New Quality Protein Innovation and Development Forum:

The New Protein Innovation and Development Forum, hosted by the Professional Committee of New Proteins of the Chinese Society of Food Science and Technology, gathered experts and scholars from universities, scientific research institutions and business circles across the country to carry out in-depth discussions on the technical path, health effects, risk assessment and industrial application of new proteins. At the meeting, Professor Chen Jian, an academician of the Chinese Academy of Engineering, vice president of the Society, and director of the Professional Committee of New Mass Protein, released the “Top Ten Technical Problems of New Mass Protein in 2025”, specifically including: green and efficient extraction technology of low-denatured plant protein; improvement of the multi-dimensional structure of neoplasm protein mimic meat and juice sensitivity simulation; cell culture The creation of long-term transmission of muscle cells in meat cultivation; the construction of a large-scale serum-free culture system for cell cultivation meat; the construction of microbial fermentation bacteria protein high-efficiency cell factory; the design of protein biological manufacturing reactor and the intelligentisation of high-density fermentation process control; the precise design of yeast chassis cells for high-efficiency expression of functional proteins; edible Integrated technology of low-carbon processing and automated solid-state fermentation equipment of bacterial protein; optimisation of yeast protein processing adaptability and multi-scenario application development; enrichment and quality-enhancing and efficiency utilisation of Venetian sickle protein.

Professor Li Zhaofeng, vice president of Jiangnan University, gave a systematic introduction to the above problems. He pointed out that these topics are not only the bottlenecks of current scientific research, but also the key to whether new proteins can be industrialised and go to the mass table in the future.

The forum set up a number of special reports on the top ten technical problems, from intelligent manufacturing, health assessment to resource development, and introduced the progress in the field of new protein research in many aspects.

In terms of intelligent manufacturing and equipment technology, Professor Liu Donghong of Zhejiang University discussed the intelligent manufacturing path of new mass proteins and shared the three-dimensional culture and moulding technology and equipment of cell culture meat. Li Yingying, a senior engineer at the China Meat and Food Research Centre, focussed on cell cultivation of meat and shared the key breakthroughs in the construction of its large-scale production process.

In terms of health and safety assessment, Professor Yang Xiaoquan of South China University of Technology systematically explained the health effect mechanism of plant protein diet and emphasised the importance of scientific evaluation system to product development. Professor Fu Linglin of Zhejiang University of Industry and Technology proposed a systematic assessment and control strategy for the risk of sensitisation for emerging protein resources such as insect proteins. Jin Fen, a researcher at the Institute of Agricultural Quality Standards and Testing Technology of the Chinese Academy of Agricultural Sciences, further explored the risk of chemicals in the cell culture medium and discussed the scientific construction of the safety system of cultured meat.

In terms of green manufacturing and resource development, Li Huiyue, a senior engineer of Jiangxi Fuxiang Pharmaceutical Co., Ltd., proposed a green process path for the industrialisation of new protein. Associate Professor Li Jian of Beijing University of Industry and Commerce deeply analysed the flavour characteristics of yeast protein and its multi-scenario application potential. In addition, Jiang Xianzhi, the founder of Momi (Guangzhou) Biotechnology Co., Ltd., and Liu Xiao, an associate researcher of Jiangnan University, respectively introduced the creation and multi-scenario application expansion of the Venetian sickle fungus.

Xue Changhu, an academician of the Chinese Academy of Engineering, Professor of Ocean University of China, and Wang Qinhong, a researcher at the Tianjin Institute of Industrial Biotechnology of the Chinese Academy of Sciences, concluded: “New protein is not only the breakthrough direction of food science and technology, but also a strategic choice to ensure national food security and achieve sustainable development. Only through collaborative innovation and cross-border integration can we jointly meet the global challenges of protein supply.

Artificial Intelligence and Food Seminar:

At a time when artificial intelligence technology is accelerating to penetrate into various fields, how to promote its deep integration with food science, health research and other fields has become the key proposition of industrial upgrading and scientific and technological innovation. At the artificial intelligence and food seminar co-hosted by Professor Sun Xiulan, dean of the School of Food of Jiangnan University, and Jiang Shuqiang, a researcher at the Institute of Computing Technology of the Chinese Academy of Sciences, experts and scholars from universities, scientific research institutes and enterprises focussed on the innovative achievements of artificial intelligence in food science, brain health, industrial application and other fields. In-depth communication.

At the beginning of the seminar, Jiang Shuqiang systematically sorted out the application progress of AI technology in the field of food with the title of “Artificial Intelligence-Driven Food Science Research”. He pointed out that artificial intelligence has gradually penetrated from basic research to the whole chain of food research and development, production, safety, etc., providing a new methodology for food science research, promoting the transformation of the industry from traditional experience-driven to data intelligence-driven, and attracting the attention of the whole audience.

Hu Bin, a professor at South China University of Technology, focussed on the “Multimodal AI Large Model-Driven Depression Brain Health Research” and shared three core research results. The dynamic map pulse neural network model developed by its team has solved the problem of time dynamic feature extraction and bioexplicability missing through innovative designs such as BIP modules; the multi-task mixed pulse network model realises the efficient processing of joint classification and segmentation of CT images, which is greatly efficient than the traditional single-task mode. Improvement; The multimodal language risk assessment model builds a depression risk assessment system covering EEG, voice, text scale and other multimodal data based on the collaborative attention mechanism, and finally formed a “multimodal + brain-like + knowledge-driven” brain health management framework, with low power consumption and high response characteristics, for real-time health Dynamic evaluation provides technical support.

Cheng Wei, a dual professor of Huashan Hospital Affiliated to Fudan University, referred to the global attention to brain health issues with the title of “Big Data-Driven Brain Health Research”. He introduced that the number of brain disease patients in China ranks first in the world, and Alzheimer’s disease (AD) and other diseases seriously affect the quality of life of the elderly. Relying on artificial intelligence algorithms, his team has built a series of results such as the brain biological age assessment model and the blood protein AD risk early warning model based on multimodal images. It has also been confirmed through research that a healthy lifestyle can reduce the risk of AD by 41% and the risk of depression by 72%, and machine learning has helped Build the best diet model for AD, which provides a scientific basis for early accurate intervention.

Ma Peihua, a researcher at the Institute of Agricultural Products Processing of the Chinese Academy of Agricultural Sciences, focusses on the “cross-basic research of artificial intelligence and food science”, showing the hardcore breakthrough of AI in the field of food. He introduced that the team realised millimetre-level heating control in food extreme processing through Q-Learning, and completed the screening of high-throughplet materials with the help of the Gaussian process. The “AI food techologist” developed by it became the first food AI intelligent body included in OpenAI. At the same time, he expects that in the future, AI4-food will achieve greater breakthroughs in the research of natural product function, intestinal microbial mechanism analysis, and extreme process control.

Li Li, dean of Xunfei Higher Education Research Institute of the University of Science and Technology, Cheng Li, vice dean of the School of Food of Jiangnan University, and Qin Hui, deputy general manager of Luzhou Laojiao Brewing Co., Ltd., shared their experiences from the perspective of educational application, discipline-specific large model construction and industrial practice respectively. Li Li introduced the application cases of large models in college teaching evaluation, intelligent office and other fields; Cheng Li explained the construction background of FoodSeek special large models for food disciplines and the cooperation path between schools and enterprises; Qin Hui shared the results of the exploration and application of digital intelligence technology in the liquor industry.

This seminar has built a cross-border communication platform in the fields of artificial intelligence, food and health, and comprehensively presented the achievements and application prospects of cutting-edge technology. Experts said that the seminar will accelerate the transformation and application of AI technology in the fields of food and health, promote the upgrading of the industry to precision and intelligence, and inject new momentum into the implementation of the Healthy China Strategy.

Seminar on Technology Innovation and Industrial Development of Dairy Deep Processing:

With the slowdown in global dairy consumption and the increase in consumers’ demand for nutrition and health, deep-processed raw materials for dairy products are becoming a key component in achieving precise nutrition. At the seminar on dairy deep processing technology innovation and industrial development chaired by Professor Jiang Yujun, vice president of Northeast Agricultural University, and He Jian, director of the National Dairy Technology Innovation Centre, the experts clearly outlined the future picture of China’s dairy deep processing.

With the deep processing of dairy products as the traction, it drives the value of the industrial chain to leap.

Jiang Yujun pointed out that the dairy industry has changed from the “era of nutrition preservation” and the “era of nutrition optimization” to the “era of precise nutrition”. Deeply exploring the natural nutrition in dairy products and realizing precise nutrition transmission is inseparable from the innovation and breakthrough of deep processing technology. Professor Ai Lianzhong, dean of the School of Agriculture and Biological Engineering of Shanghai Jiaotong University, said that the dairy industry will enter a new cycle of “total stability and structure rebalance” in the next 3-5 years, with cheese products as the core, extending high value-added products such as whey powder and functional milk-based ingredients. Professor Zhou Peng of the School of Food of Jiangnan University said that compared with traditional whey ingredients obtained through enzyme coagulation or acid sedimentation, natural whey obtained through membrane filtration has unique nutritional and health characteristics. In addition, through the isolation and enrichment of key subcomponents in casein, its nutritional characteristics and health efficacy in special foods such as infant products can be better improved.

Innovation and breakthrough from “component simulation” to “structure-function”