A rapidly growing beverage category in China are the milk teas. They are a combination of the bubble teas that originated in Vietnam and based and traditional milk or butter teas drunk by Mongolians and Tibetans.

In the course of 2018, China’s tea aficionados have embraced a new trend, one that is encapsulated in the growing popularity of the milk tea brand, Heytea. Originally sold in a tiny alleyway in Jiangmen, southern China’s Guangdong province, the brand went viral on social media because of its signature “cream cheese” series — a cup of hot sweet tea topped with a spoonful of savoury cream cheese. Since then, Heytea has developed into a franchise with more than 80 outlets in 13 cities across the country. There are also outlets in North America.

Milk tea now has many brands and more are still being added. Some are already established brands: for example, Naixue, Chagee, Mixue Ice Cream & Tea and Chabaidao.

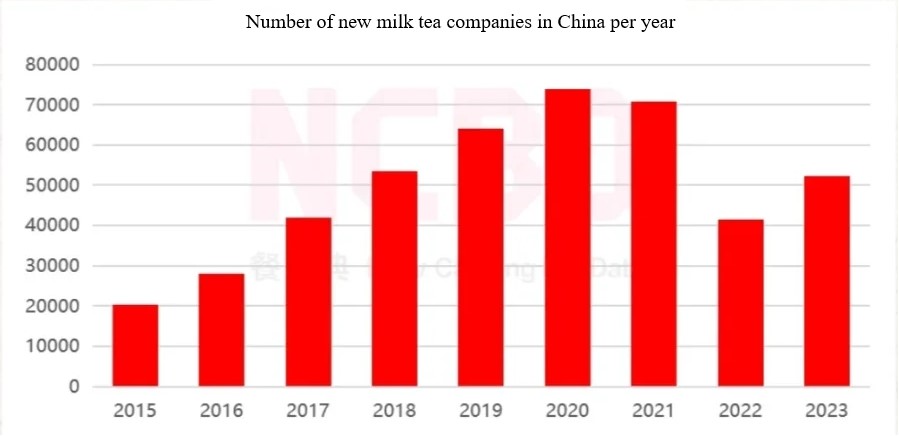

This table shows the number of new outlets opened per year.

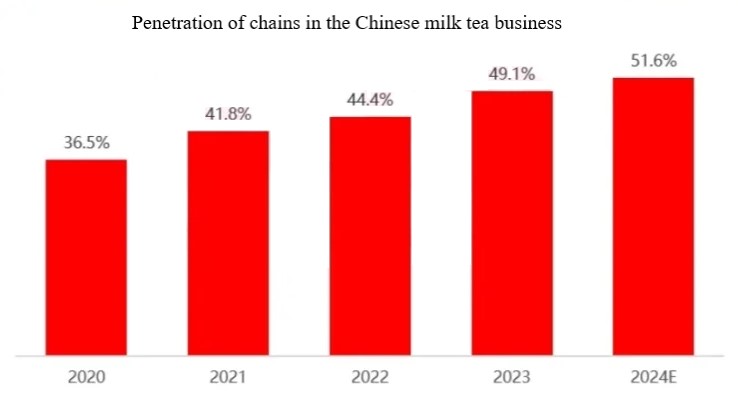

The penetration of chains has been steadily increasing in this business.

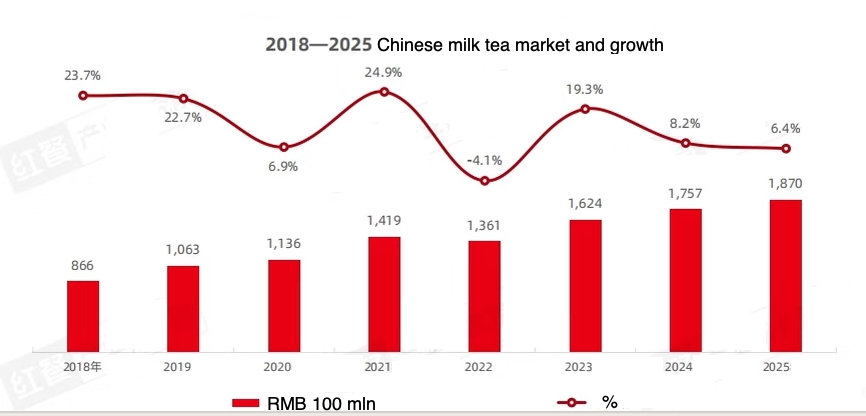

Here is an overview of the market size in RMB 100 mln and annual growth in %.

The following table lists the turnover and profit for a number of major players in this market for 2024.

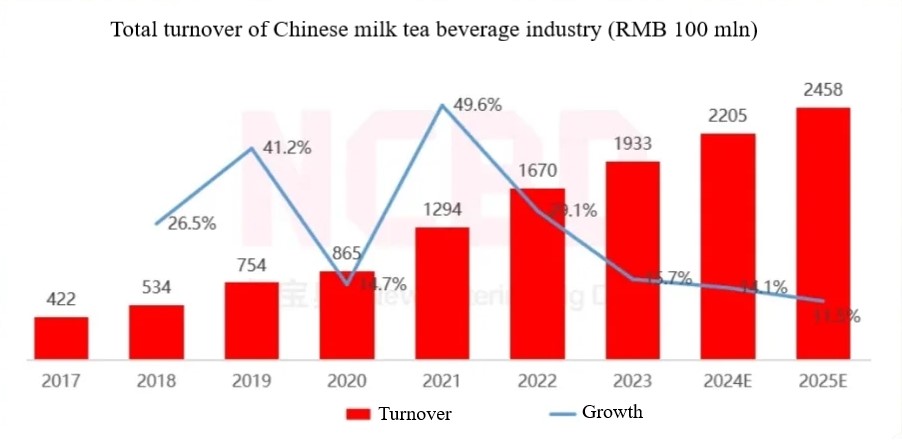

This positive trend can be expected to continue, as the total turnover of this business is expected to grow, at least during the coming few years.

The 2023 New Tea Drink Research Report, released by the China Chain Store and Franchise Association and Meituan New Catering Research Institute, predicts that by the end of 2025, the market size of Chinese-style tea drinks will reach RMB 242.5 billion.

It is not news that milk tea is outrageously popular in China. Young people are at times willing to line up for ours to sample a new flavour of a newly opened shop. However, there is clash of interests in the popularity of the colourful beverages. Chinese consumers are talking all day about more healthy eating and drinking milk tea definitely does not fit into that realm.

The various brands are engaged in a murderous competition and the less than healthy image of the product does not make that battle easier. Recently, the brands have started to work on that image and their competition for the healthiest version has become as fierce as the one for market share.

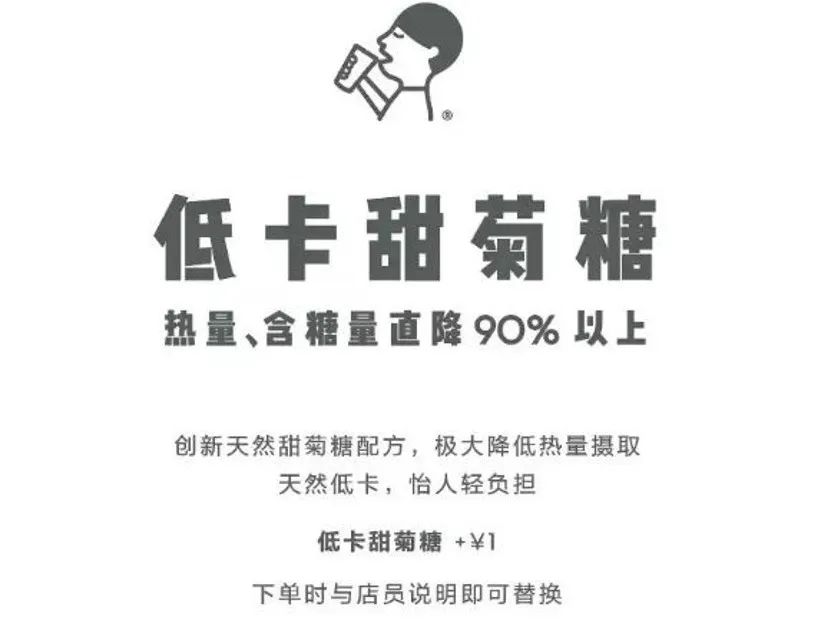

A relatively easy aspect to work on is sweetness. In line with the ongoing no sugar no salt no fat vogue in the food and drinks markets, many top brands have started advertising with their favourite sugar substitute. In this post, I am showing a few of these ads.

Nayuki

Nayuki (Naixue) has chosen the monk fruit (luohanguo or arhat fruit, in Chinese). This gives its sweetening a very Chinese image. The ad claims 0 calorie sweetener and also adds that it is ‘vegetable sweetness’, which sounds very natural.

Hi Tea

Hi tea (Xicha) is is sweetening with stevia. This, according to the ad, decreases the energy content with 90%. The ad also tells us twice that stevia is a natural sweetener. This is supported by the Chinese name for stevia: tianjutang, literally ‘sweet chrysanthemum sugar’.

Baifen Tea

Baifen Tea (Baifencha) has selected a less common sweetener: L-arabinose. The add uses a pun ‘pa tang bu pa tang’ ‘afraid of sugar not afraid of sugar’. This is based on the fact that the final character of the Chinese translation of arabinose (alabotang ‘arabian sugar’) is tang. A minor problem with arabinose is that Baifen Tea cannot claim zero calories, as this sweetener is low caloric.

Anyway, Chinese milk tea companies keep looking for more alternative sweeteners as well as alternative ingredients for the fatty ingredients. I will keep you abreast on this page.

The oldest Chinese carbonated beverages dates from 1874

Soft drinks is undoubtedly a Western concept. However, the history of domestic carbonated beverage in China is longer than many people may believe. The most famous soda beverages launched before 1949 are:

Most of the HQ locations were cities with considerable numbers of foreign expats.

The Chinese typology of foods and beverages is one of the recurrent themes in this blog. The typical way in which such products are divided in categories in a certain region provides an interesting look on the influence of the local culture on eating and drinking.

This post will continue with this topic with the typology of beverages. This typology has even been officially laid down in a State Standard (GB), GB10789 to be precise. It discerns the following types.

Carbonated drinks

These are relatively new in China and still strongly connected to the Western lifestyle. China’s oldest carbonated drink: Beibingyang (Northern Ice Sea) has been revived recently, which I have introduced in a separate post on the reappearance of old brands.

Protein beverages

Although not a Chinese invention, this category is much more popular in China than elsewhere in the world. They have also been introduced separately in a previous post. Protein beverages are relatively viscous liquids made from various nuts or beans, or milk, or a combination. A number of them include probiotic cultures.

Bottled water

Paying a lot of money for something that you can get from your tap for a much lower price has also taken on in China. China’s bottled water market is expected to reach 490 mln hls of total annual consumption by 2020. The retail value of bottled water in China for 2019 is estimated at RMB 346.2 billion. Apart from the large number of branded water, new mineral water brands keep appearing in China. Many are profiling themselves with the location of their source. The trend of 2015, e.g., in this category was mineral water from Tibet.

Some statistics of the past 5 years

Year

Volume(hls)

Increase(%)

2015

841,016,000

7.60

2014

781,614,000

9.37

2013

665,114,000

13.01

2012

556,278,000

19.20

2011

178,900,000

23.67

Top brands

The following table shows the market shares of major brands in 2017

Brand

Share (%)

Nongfu Spring

8.5

C’est Bon

8.0

Evian

5.0

Chef Kong

4.8

Ganten

4.6

Wahaha

4.5

Coca Cola

4.0

Others

60.7

A new variety was added to the category of bottled water by Nongfu Spring in February 2022: bottled boild water (baikaishui). This type is inspired by traditional Chinese medicine. TCM attributes many healing and nutritional functions to water that has been brought to the boil and then cooled to drinking temperature.

China’s once largest mineral water brand, Laoshan, came back in 2025 with a mineral water enriched with snake grass. Snake Grass, also known as Clinacanthus nutans, is a plant ascribed various medicinal benefits, like anti-inflammatory, anti-diabetic, anti-cancer, and antioxidant properties.

Tea beverages

Tea is China’s national drink, but still, tea beverages have been introduced from overseas. When foreign ice teas were launched in China, many beverage makers tried to concoct their own versions. Tea beverages with various fruit flavours appeared one after another.

Milk tea

A rapidly growing subcategory are the milk teas, based on traditional milk or butter teas drunk by Mongolians and Tibetans.

The pictures shows the Sizhou brand milk tea, with the following ingredients:

In the course of 2018, China’s tea aficionados have embraced a new trend, one that is encapsulated in the growing popularity of the milk tea brand, Hey Tea. Originally sold in a tiny alleyway in Jiangmen, southern China’s Guangdong province, the brand went viral on social media because of its signature “cheese” series — a cup of hot tea topped with light cheesecake mix. Since then, Hey Tea has developed into a franchise with more than 80 outlets in 13 cities across the country. In large urban centres such as Shanghai and Beijing, customers routinely wait for hours to get their hands on a cup of cheese tea. Hey Tea’s cheese-inspired beverages are just variations of the same milk-topped teas available at many urban teashops in China. Fresh milk, skimmed milk, and cream cheese are blended and poured on top of iced tea to create a layer of creamy froth about 3cm thick.

Milk tea is becoming such a huge market that ingredients suppliers have started to prioritise it in their R&D. FrieslandCampina Kievit, e.g., is conducting research to develop the optimum dairy ingredients for Chinese milk tea. Aspects considered include: tea type, milkiness, sweetness and mouthfeel.

A new development in the Chinese tea beverage market is mixed tea drinks. Representative brands are: Teaka (tea + coffee), Chef Kong’s tea + milk, Cha pi (tea + fruit juice) and Hongchajun (tea + probiotics).

Multinationals like Coca Cola cannot afford to miss out on the popularity of tea beverages in China. The company has launched a range of tea drinks branded Chunchashe ‘Genuine Tea House’. It is marketed as not containing sugar, but still leaving a sweet aftertaste. It comes in green, black and Wulong flavours.

Herbal tea

Traditional Chinese Medicine (TCM) is making an effort to cash in on the increasing interest in health foods among Chinese consumers, as has been introduced in earlier posts. The market value was estimated at more than RMB 40 billion late 2015 and is expected to grow to close to RMB 20 billion in 2020.. A very prominent application of medicinal herbs as food ingredients are the herbal teas that have become popular during the past few years. The first and most popular, Wanglaoji, is still based on a traditional recipe. Later herbal teas are marketed as modern health or functional beverages, comparing and competing with Western drinks like Red Bull. A very recently launched product in this category is Good Night (Wan An), produced by Wan’an Technology Co., Ltd. (Beijing). Ingredients are said to include:

natural GABA, theanine, chamomile and spina date seed

Wanglaoji launched its own cola drink, Wanglaoji Cola, in January 2018. The company promoted it during the Davos Summit.

The value of the Chinese tea beverage market in 2020 exceeded RMB 100 billion.

Coffee beverages

Coffee being such a recent arrival in China, so closely linked to a Western lifestyle, it seems odd to find it as an officially sanctioned subcategory of beverages. However, they have become quite popular. Perhaps they are easier on the Chinese palate than the basic black brew. The have been introduced in this blog before, in a separate post.

Plant beverages

This category includes drinks made from the juice of vegetables and fruits, in various degrees of concentration. Cereal based drinks are also included. A subtype that is especially popular in China is called ‘fruit tea’ (guocha) in Chinese. The best English translation would be ‘nectar’. The are relatively viscous drinks with carrot or hawthorn pulp as the main ingredient.

In 2016, China’s fruit juice retail volume was 134.47 mln hls and retail sales reached RMB 100.914 billion, up 1.88%. Main brands in the Chinese fruit juice market include Uni-President, Chef Kong, Nongfu Spring, and Huiyuan. China’s top producer in this category is Huiyuan Fruit Juice (Beijing). The company was once an acquisition target of Coca Cola, but the deal was vetoed by the Chinese cartel watchdog. Huiyuan recently launched a range of juices in Malaysia under the Yami brand.

The latest addition to the fruit nectars is Zaoshanzha, a drink made from dates and hawthorn by Haoxiangni.

In terms of taste, orange juice is still the largest category of the fruit juice market in China, There are some differences in taste between the north and the south in China. Apple, peach and pear consumption is relatively high in the north market. Pure juice (‘not from concentrate’) is the growth point in this industry. Chinese women have greater demand for juice, which is related to the pursuit of a healthy figure.

Another popular new subtype is formed by the fruit vinegars. These beverages have become in vogue in the years 2015 – 2016 as health products that help burn fat. In the early stage, it looked as if they would become a success, cashing in on the general trend towards more healthy food in China. However, the tide seemed to turn mid 2018, when a prominent brand, Tiandi Nr. 1 (Tiandi Yihao)’s semi-annual report showed a turnover almost half that of the same period of the previous year.

Flavoured beverages

The literal translation of the Chinese definition of this category is: drinks made by combining food flavours, sugar or sweeteners, or acidifiers. We probably could also refer to these as: designer beverages. It is not always easy to distinguish these from other categories. If you boil tea leaves and the add other flavouring ingredients to the filtered liquid, you would have a tea beverage. However, a drink whose ingredients list includes tea extract, would count as a flavoured beverage.

Nutritious beverages

These include sports drinks and other functional beverages. This category started to boom in the course of 2016. As a result, Red Bull is confronted with an ever growing number of domestic competitors in China. One of the frist challengers (August 2016) was a vitamin drink by Want Want, presented in a gold-coloured can.

This product category is getting so popular, that a dairy company like Yili launched an energy drink of its own in April 2018: Huanxingyuan.

Solid beverages

These are sold in powdered from and infused before consumption. There is at least one traditional Chinese drink typically sold as such: suanmeitang or sour plum drink (literally: soup). A more recent, but still traditional, product is instant soy milk. Many members of the other categories are now also available in powdered form.

The picture shows Yiben brand suanmeitang, which contains the following ingredients:

Senke Beverages has launched an innovative type of suanmeitang adding traditional Chinese medicinal herbs, marketed as ‘Lotus Leaf Suanmeitang‘, in the summer of 2018. Apart from quenching thirst, it is said to lower cholesterol and have a certain slimming effect.

Daring launches – low survival

Chinese beverage makers are quite daring in launching newly developed products on the market, where Western multinationals would organise more pilots to test the products’ reception by consumers. However, a recent survey by the China Food Industry Association reveals that only 5% of newly launched Chinese beverages survive. I guess that is test marketing the Chinese way.

How do Westerners appreciate this?

Are you getting bored with my academic stories? No problem, you can now relax watching this home brew video in which a Western lady living in China introduces here own favourite Chinese beverages.

Here is another Top 5, but then of the most bizarre Chinese drinks.

Latest trend: odd flavours

The structure of the Chinese soft drinks market is undergoing rapid changes. Consumers are developing an awareness of personality, paying more attention to individual needs and preferences. This has created a market for what Chinese have started to call ‘odd flavour water (guaiweishui)’. Laoshan, China’s first and for a long time only producer of mineral water, has launched Baishecaoshui (literally: white snake grass water). It is based on Baishecao (oldenlandia). Hey Song Sarsaparilla from Taiwan is also gaining popularity. The current top producer of mineral water, Nongfu Spring (see above), has also launched odd flavour drinks: Oriental Leaves (Dongfang Shuye), which does not contain herbal extracts, but a mix of flavourings and nutrients, and Red Pointed Leaves (Hongse Jianye), which contains extracts from American Ginseng, green tea and bamboo. This market is extremely volatile. The survival rate of new drinks is generally about 10%, and is now dropping to 5%, according to recent market studies. These products are catering to the young and young Chinese consumers have a low brand loyalty where food and drinks are concerned.