If you want to understand the basics of how the Chinese government creates a level playing field in business, in particular in relation with foreign products, study this post.

Developments in this business have been literally dramatic, and it is directly related to the most precious item of the majority of adult Chinese: their, until recently, only child.

Melamine

A synopsis of what had happened from 2008 up to the present day.

In the year of the first Chinese Olympics it was discovered that several brands of domestic infant formulae contained melamine, a compound that make the protein content of milk appear higher in the standard tests as conducted by dairy companies. It caused about 300,000 babies to get seriously ill, with a small number of deaths.

As a result, the market share of the domestic brands dropped even lower that it already was at that time. However, a number of smaller brands deftly used this situation to gain market share, as is clarified in the following video

Hubris

Foreign brands believed that a Golden Age had come, in which they could virtually set the market price of formulae in China. European and American brands increased their prices almost every couple of months, without naming a valid reason.

Chinese consumers were so eager to get their hands on foreign products, that Chinese on foreign trips were asked by the relatives to buy up any formulae they could get their hands on, as products there were much cheaper than in Chinese supermarkets. In countries like the UK or The Netherlands, quotas were issued for the number of packagings single customers could buy at one time.

Then the gods punished the foreign suppliers for their hubris. Fonterra came with the news that its whey powder could have been contaminated. That shocked China.

Leveling the playing field

The Chinese authorities grabbed the momentum of the falling consumer confidence in foreign formulae to start a media campaign trying to restore the reputation of domestic product.

To support this, they launched an investigation into monopolistic activities by foreign suppliers of infant formulae. A good example is the accusation against Danone that it had bribed hospital staff to feed babies first with their Dumex formula, to get them hooked on that brand. Most foreign suppliers were found guilty, and those who have not fully cooperated with the investigation, were heavily penalised.

However, a survey among young parents conducted at that time noted that the latter were still more confident in foreign formulae.

Who the were the guilty parties in all that commotion? I believe all of them.

The domestic suppliers have forfeited their favourite position with relatively low cost to produce good generic infant formulae. Instead, many of them, including the then market leader Sanlu, were attracted by the short-term opportunity of increasing their income by adding ‘protein power’ (read: melamine) to their milk. The larger Chinese producers usually control the entire value chain, from cow to formula. This means that the melamine was added right under their noses and it is hard to believe that they were not aware.

The foreigners have been too greedy. The constant price hikes increased the financial burden for young parents. Without those unreasonable price increases, the authorities would probably have left their high market shares untouched.

The international media have been biased towards the domestic companies. Chinese companies like Sanlu were heavily criticized in the Western press for trying to hide the first reports about health problems, not to spoil the national Olympic party. The same media were a lot milder towards a company like Fonterra, the then partner of Sanlu.

New system of accreditation

The Dairy Association of China (DAC) has begun to promulgate ‘state endorsed milk powder manufacturers’. Here, ‘milk powder’ mainly refers to infant formulae. Severa; have so far been stamped this way. Others are allowed to produce as well, but the state only guarantees the quality of the suppliers on its shortlist. It will surprise no one that China’s top dairy company Yili (see the item on China’s top brands of 2014) heads the list.

Foreign brands need to be registered and are not allowed to be active in China with more than 3 brands or 9 different products.

The best that can come out of this mess is that there now is finally an opportunity that the Chinese market for infant formulae becomes a level playing field in which domestic and foreign brands can compete fairly.

Inbound foreign investment- new style

Statistics seem to confirm that it works. Four of the five most popular infant forumula brands in China were foreign brands. This is happening in spite of recurrent media reports about batches of imported infant formulae being rejected by the Customs inspections.

A number of international players try circumvent those problems at the customs through setting up local production.

FrieslandCampina of the Netherlands entered into a joint venture with Huishan Dairy (Liaoning) to jointly produced infant formulae in October 2014. The joint venture will own Huishan’s facility in Xiushui (Liaoning). During the obligatory ceremony, the Dutch partner’s CEO said that he was ‘proud that FrieslandCampina will be part of the first joint venture between a Chinese and a foreign dairy company that will locally source, manufacture, market and distribute infant milk formula’. That statement called for correction, as a number of international investors have preceded FrieslandCampina, with varying results. A few years later, mid 2017 to be precise, the joint venture got into serious problems, when the Chinese partner Huishan was accused of fraud. FrieslandCampina opted to buy out their local partner early 2018 and now operate a wholly foreign owned company alongside their partner. This situation is far from ideal, as it renders FrieslandCampina’s local production in China extremely vulnerable.

Later that same month October 2014, Danone announced that it was to subscribe to a private placement by Yashili, one of China’s leading infant milk companies. Upon completion of the subscription, Mengniu, currently Yashili’s majority shareholder, will hold a 51.0% equity interest and Danone will hold 25.0%. Danone and Mengniu want to use this expanded alliance to grow Yashili and develop a wide range of products that meet the very highest standards in this category. Through their alliance, Danone, Mengniu and Yashili intend to expand and strengthen their cooperation in the infant milk formula business in China. The parties will study the possibility of a minority equity investment by Yashili in Danone’s subsidiary Dumex China.

Reaping success

Domestic brands have started recouping market share in 2018, fastening the pace in 2019. A leading player in this developed is newcomer Junlebao (Hebei). Founded in 1995, Junlebao used to make only yogurt. It added infant formula to its product line in 2014 to help revitalise the product’s domestic presence. In the following five years, the company established a whole industrial chain, including a planting pasture, a base for breeding cows and quality-control centre. By 2019, the company had 17 production plants and 10 breeding bases with more than 60,000 cows across China. To improve the quality of its milk sourcing, Junlebao has developed a high-standard cow breeding system, which consists of raising the animals in comfortable barns, feeding them with high-quality fodder and using high-tech machines to milk them. The market share of domestic formulae in China increased to more than 60% in 2018, thanks to Junlebao.

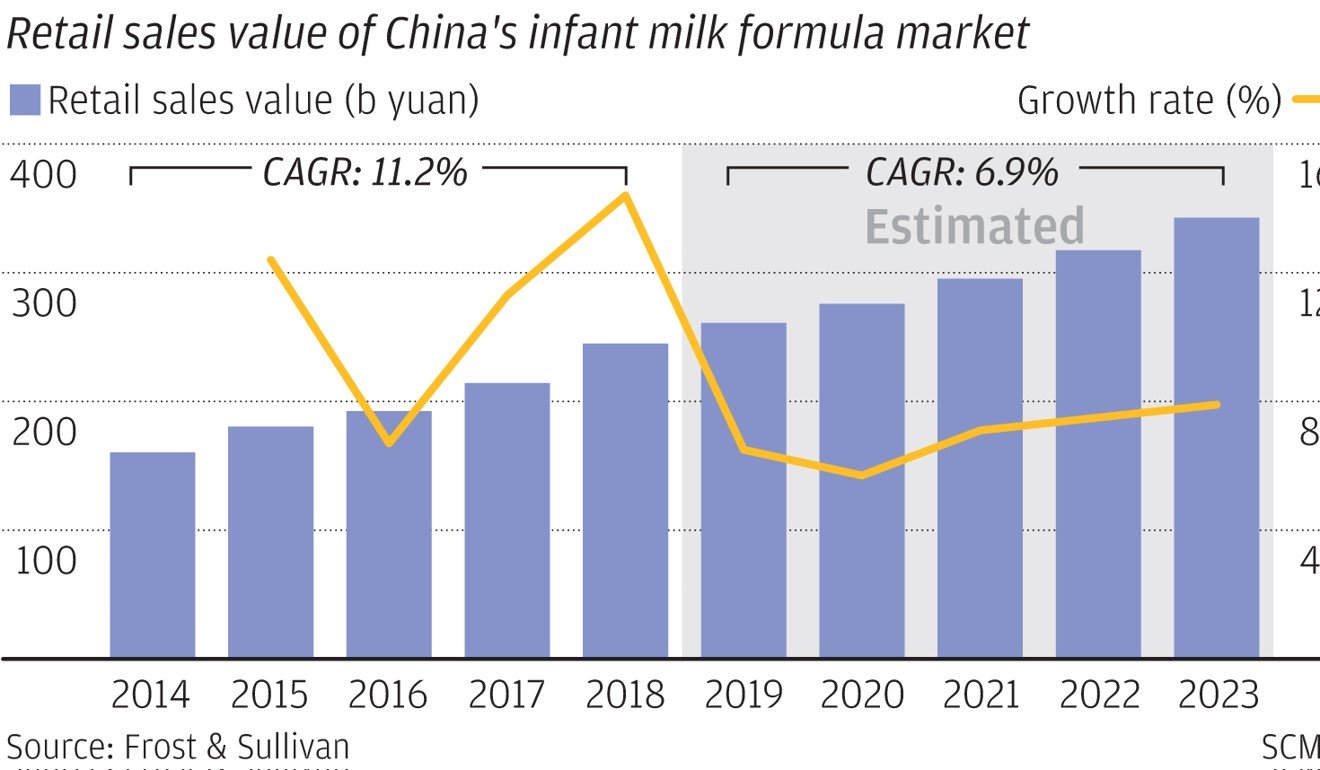

The following tables show the development of the value of the market and estimates for the years up to 2023 by various researchers.

Year

ValueRMB billion

2016

157.10

2017

187.30

2018

222.10

2019

257.86

2020

295.51

Outbound foreign investment – recent but rapid

A number of Chinese companies try to overcome the problems in the industry by acquiring foreign infant formula producers. Formulae imported from those plants then have a hybrid Chinese and foreign identity.

Bright Dairy & Food (Shanghai), China’s third-biggest dairy company by volume, has bought a majority stake in Canterbury milk processor Synlait Milk for $82 million in 2010. Synlait, which abandoned a planned $150 million share sale in 2009 due to a tepid response, is a joint owner of its processing company with Bright Dairy, while keeping and operating its farms through a separate company.

In 2014, Bright bought a majority stake in the Israeli manufacturer of infant formulae Tnuva.

September 2014, Guangdong real estate group Evergrande (which also owns the province’s main football team) acquired the New Zealand company Cowala Dairy.

Internet interaction analysis

An interesting development is that the China Statistical Information Service Centre (CSISC) has started analysing online consumer interaction about brands. CSISC published the following table showing consumer interaction about infant formulae in the 2nd quarter of 2014 today (19/9/2014).

The brand most discussed is Junlebao (also featuring in my blog on old yoghurt), followed by Dumex and Mead Johnson. The brands that the central government has been heavily supporting in the above described campaign, like Yili, ranks 7. Obviously, brands can also turn up high in this graph, because consumers may share negative experience with it. Still, CSISC analysts believe that this outcome shows that newcomer Junlebao’s low price strategy is reaping results. Junlebao received class A certification of EU’s BRC Food Safety Global Standards in September 2014. Junlebao’s milk powder would be qualified to enter CIES’ 200 supermarket groups in the world. I would like to add that it also proves the central authorities right: the Chinese market for infant formulae is a level playing field now. The international brands are still favourites, but local entrepreneurs have ample space to move, as long as the get their strategy right.

Top formulae of 2019

The following table shows the top 5 infant formula suppliers in China of 2019

Company

Market share(%)

Nestlé

14

Feihe

13

Danone

10

Abbott

7

Mead Johnson

6

More babies, bigger market . . or not?

The market for infant formulae has changed in China, when the government decided that couples who both were only children were aloud to have 2 children. Even though fewer eligible couples responded positively than expected during the first few years after the decision, this is now gradually leading to a small baby boom. That and the continuing growth of an affluent middle class, has boosted the sales of most players in this market. However, this does not mean that China will once more become the paradise of multinationals in this field. It is a genuine level playing field now, and a growing one, with opportunities for all companies that are willing to play by the rules.

However, in spite of the new policy, 15.23 mln babies were born in China in 2018, 2 mln fewer than in 2017. Therefore, insiders estimate that the consumption of infant formulae in 2019 will be approximately the same as in 2018, and will decrease with 2% in 2020.

Innovative products – a step up the ladder for the Chinese industry

Beingmate (Hangzhou, Zhejiang) has received official approval for the production of infant formulae for prematurely born babies and over-birthweight babies in August 2019. While these are not new types of formulae, Beingmate was the first in China to launch these specialist products. Fonterra is a major shareholder of Beingmate. After the repositioning of the regular Chinese infant formulae, this development could mark the beginning of the rise of the Chinese industry on the technological ladder.

The organic way

The sales of organic infant formulae increased significantly in the course of 2019. Buoyed by the rising demand, several multinational companies like Germany’s Hibb, Switzerland’s Nestlé and its unit Wyeth are not only witnessing resurgent sales. Hipp is looking to further expand its presence in the e-commerce market. The company witnessed annual growth of about 20% in China in 2019, making the country its second-largest market after Germany. Besides, Wyeth, the baby and infant formula unit of Nestlé, has introduced Illuma 3 organic products for Chinese parents since 2017. Its research released in October shows that the sales of organic infant and maternity products grew by 33% year-on-year in China, creating a generation of “organic mothers”. US infant formula maker Mead-Johnson introduced its grass-fed Enfagrow to Chinese consumers in September 2019.

If this article is of interest to you, you may also like: