I. Overview

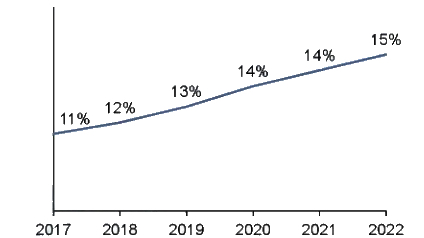

Anti-ageing helps people delay the ageing process of the body and promote overall health, so that people can stay mentally and physically healthy, within the life limit determined by genetic factors, and improve the quality of life. The following table shows the percentage of the part of the Chinese population that is 65 years or older.

Skin ageing refers to the deterioration of the cell structure and function of skin tissue under the continuous action of the internal (accounting for 20%) and external (accounting for 80%) environment, usually manifested as dry skin, pigmented spots, reduced skin elasticity, sagging, rough and wrinkled skin. There are many schools of research on the causes of skin ageing, including genetic ageing, excessive free radicals, photoaging, non-enzymatic glycosylation, etc. Endogenous ageing refers to the ageing of the human body due to irresistible physiological factors such as genetics and endocrine. Exogenous ageing is environmental ageing, that is, ageing caused by light radiation, environmental pollution, bad living habits, etc.

II. Anti-ageing policy

In recent years, China has issued a series of policy documents to promote the development of the anti-ageing industry. In August 2022, the General Office of the Guangzhou Municipal People’s Government issued the ’14th Five-Year Plan’ for the Development of the Marine Economy of Guangzhou, which proposed to focus on the development of marine biologically active substance screening, marine biological genetic engineering and other technologies to support marine biological vaccines and substances such as antibacterial, antiviral and antioxidant derived from marine organisms. The research and development of biologically innovative drugs, as well as the development, production and industrialisation of high-value-added marine biological functional foods such as lowering blood sugar and blood lipids, improving immunity and anti-ageing, have led to the establishment of a number of new enterprises in the fields of marine drugs and functional biological products. In January 2024, the General Office of the State Council issued the Opinions on Developing the silver-haired Economy to improve the welfare of the elderly, which proposed to develop the anti-ageing industry, promote the deep integration of biotechnology and delayed senile diseases, and develop products and services for early screening of geriatric diseases.

III. Anti-ageing value chain

The upstream of the anti-ageing industry chain is mainly plant extracts, traditional Chinese medicine and other anti-ageing raw material industries, and the downstream is mainly in the fields of skin care, beauty and health care.

At present, scientists have found that a variety of plant extracts can be combined with NMN to improve their anti-ageing effect. This development started relatively late, but its growth is rapid. According to statistics, the domestic plant extract market has increased from RMB 5.66 billion in 2015 to RMB 23.78 billion in 2023; an annual growth rate of 20.94%.

IV. Development status of the anti-ageing industry

With the ageing of China’s society, ‘anti-ageing’ has now become a topic of high public attention. People’s lifestyle and habits are changing. They all want to be young forever and minimise the traces of ageing, which has promoted the rapid growth of sales of anti-ageing products. Data shows that the market scale of China’s anti-ageing industry in 2023 was about RMB 152.18 billion, in which skin care products were good for RMB 94.82 billion; nicotinamide mononucleotide (NMN) health care products RMB 12.48 billion; and other anti-ageing health care products and health foods RMB 44.88 billion.

The research and development strategies of domestic anti-ageing brands are shifting to products made from traditional Chinese medicine, and use advanced medical technology to promote the rapid development of traditional Chinese medicine skin care products. The attention of international high-end brands still dominates the field of anti-ageing skin care products in China, but consumers gradually recognise domestic anti-ageing brands, which promotes domestic brands to perform better and better in the mass market and have greater development potential.

Data show that 53.2% of consumers begin to pay attention to anti-ageing at the age of 26-35, and 23.2% of consumers at the age of 18-25. With the in-depth development of the anti-ageing industry and the popularisation and application of anti-ageing knowledge, the people who pay attention to anti-ageing are getting younger and younger, and the market increases proportionally.

Still according to the research, 68.2% of consumers combine anti-ageing with fitness, 62.4% of consumers use skin care products to prevent ageing, and nearly 50% of consumers pay attention to diet and take supplements for anti-ageing. With the continuing upgrading of anti-ageing skin care products and health care products, more consumers will recognise the effectiveness of anti-ageing ingredients and anti-ageing through the use of skin care products and health foods.

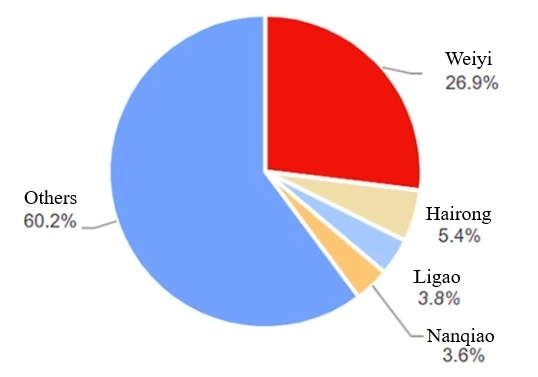

V. Key enterprises in the anti-ageing industry

The market competition in China’s anti-ageing industry is fierce, and the leading enterprises consolidate and expand their market share through product innovation, technology research and development and marketing. At the same time, with the increasing diversification of consumers’ demand for anti-ageing products, enterprises are actively looking for differentiated competitive advantages. At present, the main enterprises in China’s anti-ageing industry include Vecanbio (Zhongyuan Xiehe), Kingdomway (Jindawei), Marubi (Wanmei), BBCA Pharmaceutical (Fengyuan Yaoye), (Challenge & Young) Qianyuan, Zhongsheng Pharma, Yiling Pharmaceutical, Changchun High-tech, By-health (Tangcheng Beijian), etc.

VI. Trends in the anti-ageing industry

- Diversification and personalisation of consumer needs. Consumers’ demand for anti-ageing products is no longer limited to a single effect, but pays more attention to the diversification and personalisation of products. They not only hope that the product can effectively prevent ageing, but also hope that the product can meet their specific needs, such as improving skin quality and enhancing immunity. In addition, with the improvement of consumers’ health awareness, their requirements for the safety and effectiveness of anti-ageing products are also getting higher and higher. Therefore, brands need to pay more attention to ensure that products are both safe and effective.

- Technological innovation and application; With the continuous development of biotechnology, genetic technology, nanotechnology and other high-tech technologies, anti-ageing products will pay more attention to the application and innovation of science and technology. These new technologies will help improve the effect and user experience of the product and meet consumers’ needs for efficiency, safety and convenience. At the same time, anti-ageing products will be more intelligent and personalised in the future. Through intelligent devices and technical means, brands can more accurately understand the skin quality and needs of consumers, so as to provide more personalised skin care solutions and product recommendations.

- Market segmentation and channel expansion; With the continuous development of the anti-ageing market, the trend of market segmentation will be more obvious. Brands need to segment the market according to different age groups, skin type, dietary needs demand and other factors, and launch more targeted products to meet the needs of different consumers. At the same time, the sales channels of anti-ageing products will be more diversified in the future. In addition to traditional offline channels, online channels will occupy an increasingly important position. Brands need to pay attention to the expansion and operation of online channels to improve brand awareness and product sales.

If this post appeals to you, you may also like to read:

Public nutrition in China

Bird’s nest – if you can’t eat them, drink them

China’s silver hairs are challenging the single dogs

The Chinese health food market in 2023

Chinese research of anti-fatigue functional food

Chinese health water – the hottest drink to cool you down this summer

Peter Peverelli is active in and with China since 1975 and regularly travels to the remotest corners of that vast nation. He is a co-author of a major book introducing the cultural drivers behind China’s economic success. Peter has been involved with the Chinese food and beverage industries since 1985.